INFRA

INFRA

INFRA

INFRA

INFRA

Flash storage provider Pure Storage Inc. beat back doubts about its growth today, reporting better-than-expected first fiscal-quarter profit and revenue thanks to stealing a march on traditional storage rivals and winning new business in cloud computing and analytics.

The company reported a net loss of $62.4 million, or 30 cents a share, but adjusted for stock option expenses, the loss was 14 cents a share. That easily beat Wall Street expectations of a 23-cent loss.

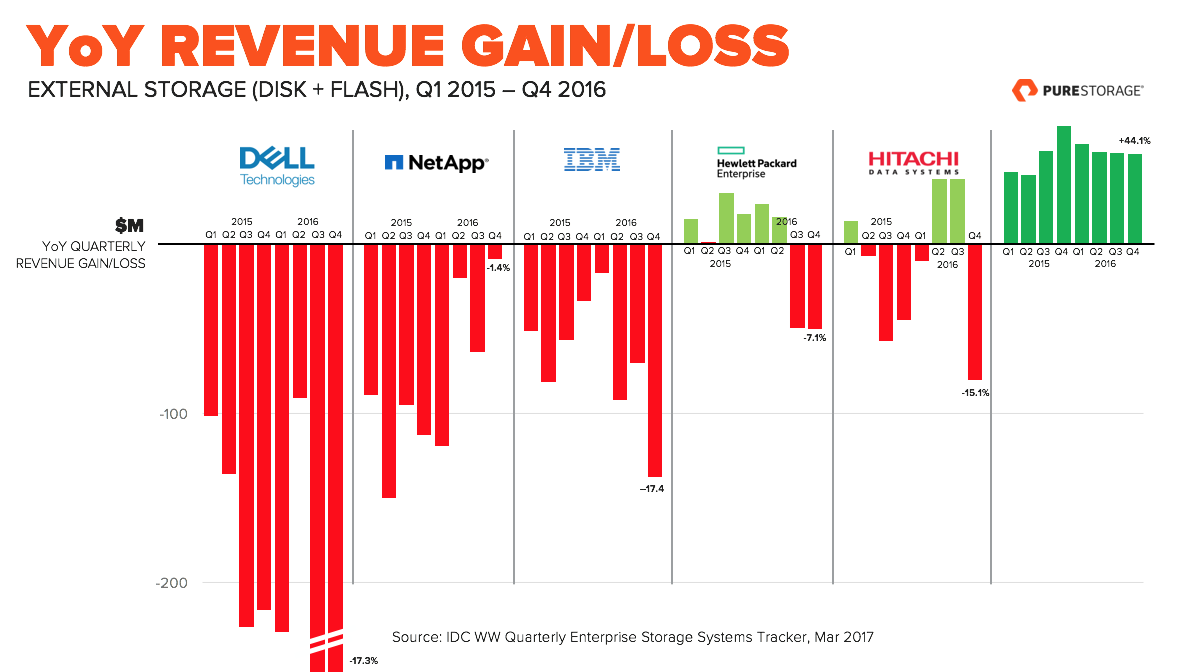

Revenue of $182.6 million, up 31 percent from a year ago, also beat forecasts of $176.4 million, as well as the range of $171 million to $179 million Pure itself had provided. In the current quarter, which ends in August, the company said it expects revenue between $214 million and $222 million, up 34 percent from a year ago at the midpoint. Not least, the company said it expects full fiscal-year revenue of $975 million to $1.02 billion, roughly the billion-dollar level it has predicted for several quarters now.

Pure’s shares surged 11 percent in after-hours trading, following a 0.28 percent decline, to $10.81 a share, in regular trading today. The stock had been down 5 percent from the start of the year and down 26 percent in the past year. Update: On Thursday, investors were a little more circumspect, as shares were rising about 7 percent. But on Friday, they rose 8 percent more.

Chief Executive Scott Dietzen (pictured) told SiliconANGLE in an interview that the company mainly is continuing to take business from traditional storage rivals such as Dell EMC, Hewlett Packard Enterprise Co. and NetApp Inc. He also said Pure gained 300 new customers in the quarter partly from a couple of broad newer markets.

One is public and private cloud providers outside the big three that build their own storage arrays — Amazon Web Services Inc., Microsoft Azure and Google Cloud Platform. The other is large enterprises that need faster storage for data-intensive workloads such as artificial intelligence and deep learning neural networks used for the likes of facial recognition, autonomous driving, advertising automation and security analysis.

“The place where we have relative greenfield is selling to the Nos. 4 to 1,000 cloud providers, for data-intensive applications and versus legacy providers,” he said.

Pure, which makes flash memory chip-based storage products for large enterprises and cloud computing providers, has had an uphill battle to meet investors’ high expectations. After its fourth-quarter earnings report March 1, shares plunged 11 percent despite a 52 percent sales jump when the company’s revenue guidance came in short of forecasts.

And on May 18, shares fell about 10 percent after Morgan Stanley cut its rating essentially to a hold and its target price from $17 to $12. Analyst Katy Huberty cited higher competition in the low-price to midrange especially from Nimble Storage Inc. and NetApp Inc., as well as slow traction for new products. She also sees uncertainty that the cloud-scale FlashBlade and other new products can expand its potential market sufficiently.

Those concerns appear to have been put to rest with the latest results, at least for now. Dietzen said Pure will become cash-flow positive in the second half of the year. But Chief Financial Officer Tim Riitters warned during the earnings conference call that the current quarter wouldn’t show as much of an improvement in operating margins.

“The company continues to overcome competitive pressures, and gross margin is holding strong despite component tightness,” Barclays analyst Mark Moskowitz wrote in a note to clients. “Pure’s sharpened focus on cloud and artificial intelligence could renew investor interest in the company.” But with a hold rating on the shares, he also said that “we need to see a firm crossover to profitability before becoming more constructive on the stock.”

In an interview, Dietzen conceded that the big public cloud providers present some competition, which he said was in the single digits in terms of market overlap. But he said it’s “very minimal” next to what he says is a $35 billion addressable market for its faster solid-state storage arrays. Still, longer-term the public clouds are likely to present more headwinds.

The market may be big enough to support Pure and a number of other upstarts, said Dave Vellante, chief analyst of Wikibon, owned by the same company as SiliconANGLE. “But it will be a knife fight and there will be more consolidation in the array business,” he said. “To emerge a leader Pure must get cash-flow positive and keep expanding its total addressable market by delivering on its aggressive roadmap. If it can stay ahead of what I call the ‘storage cartel,’ it will emerge a winner.”

Dietzen said Pure is managing what he termed favorable win rates against its three key competitors. Indeed, NetApp, which reported fiscal fourth-quarter results today, issued lower-than-expected first-quarter guidance, knocking its shares down about 3 percent, to $38.30. Update: In trading Thursday, investors thought better of the report, or at least two stock upgrades issued after it, and shares were rising 3 percent.

Pure President David Hatfield said during the call that competitors’ recent price hikes on their products may have helped the company. “It’s a nice tailwind that’s influencing our win rates,” he said.

Support our mission to keep content open and free by engaging with theCUBE community. Join theCUBE’s Alumni Trust Network, where technology leaders connect, share intelligence and create opportunities.

Founded by tech visionaries John Furrier and Dave Vellante, SiliconANGLE Media has built a dynamic ecosystem of industry-leading digital media brands that reach 15+ million elite tech professionals. Our new proprietary theCUBE AI Video Cloud is breaking ground in audience interaction, leveraging theCUBEai.com neural network to help technology companies make data-driven decisions and stay at the forefront of industry conversations.