BLOCKCHAIN

BLOCKCHAIN

BLOCKCHAIN

BLOCKCHAIN

BLOCKCHAIN

In the ongoing soap opera that is the cryptocurrency revolution, entrepreneurs have been trying to jump multiple hurdles, like Olympic sprinters heading down a long track. Getting the blockchain to scale up and figuring out how to turn real assets into tokens without winding up in jail are just a couple of the many obstacles confronting crypto players today.

But there are signs of progress on these and other issues, brought to light in Las Vegas this week at the CoinAgenda financial technology conference that attracted entrepreneurs from around the world.

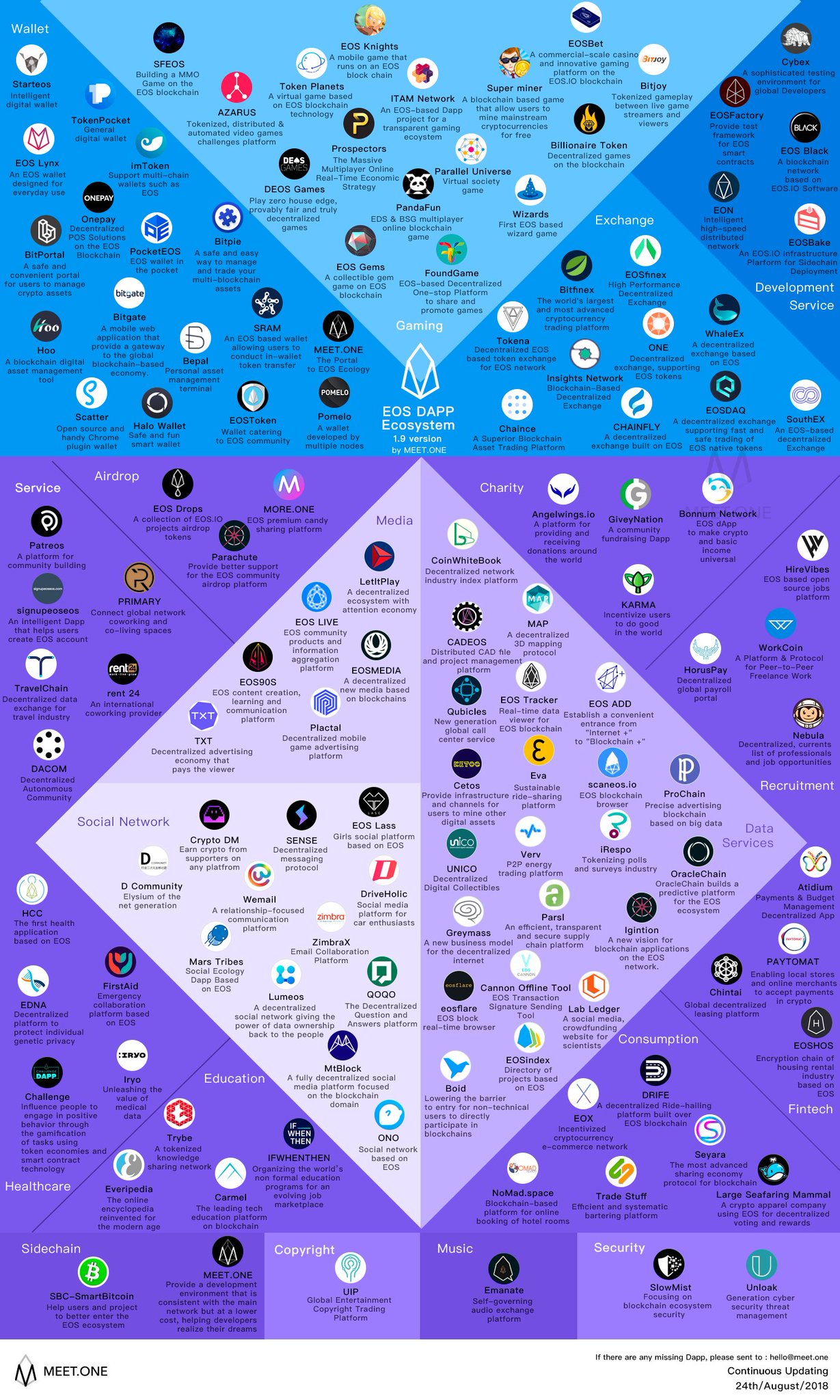

For one, a well-known crypto company founder flat-out declared that after nearly two years and a $4 billion initial coin offering investment, the EOS platform may finally be ready to deliver true scale on the blockchain.

“EOS is something that people should be paying very close attention to right now,” Brock Pierce, co-founder of Block.one, the company behind development of the new platform, said during an appearance at the conference Tuesday. “We have the first actual blockchain that can scale and do consumer applications. It’s live and it works.”

The promise of EOS has been partly clouded by chaos surrounding Block.one. According to one report, a number of the company’s earliest employees left the firm in recent weeks and Pierce himself departed earlier this year. Block.one also encountered problems with its network of block producers in June.

Despite those issues, the company issued a series of optimistic tweets recently about the rollout of EOS, including one showing its growing blockchain ecosystem. “We now can start to do consumer applications,” said the ebullient Pierce. “You can build Facebook on this thing and it runs.”

When he’s not singing the praises of EOS and blockchain scalability, Pierce is bullish on the future of security tokens, despite cryptocurrency’s rocky road. The token economy is an area of the cryptocurrency world that has been plagued in 2018 by plunging values, government crackdowns and negative press.

However, some entrepreneurs believe that security tokens offer a more promising model because they are tied to real assets, such as equity markets or real estate. An evolving ecosystem of companies is beginning to form around the security token, with firms such as Polymath Inc. providing a launchpad for companies to issue the financial instrument and Lexit, which is building a blockchain-powered marketplace for mergers and acquisitions.

“It’s ultimately the securitization of all of the world’s assets,” Pierce said. “The growth, which I think we’re going to see next year, is going to dwarf everything we’ve done to date. This is going to be a quadrillion-dollar market.”

For the security token market to reach “quadrillion-dollar” status, however, it will still require some form of approval by government regulators. So far, that appears to be a long way off. Punitive enforcement by the Securities and Exchange Commission, combined with a lack of action by Congress, have forced U.S. entrepreneurs to flee to friendlier locales, such as Malta or the Bahamas which plans to issue its own state-backed cryptocurrency.

“It seems like my second job is talking with lawyers,” cryptocurrency entrepreneur and investor Michael Terpin said during a panel discussion.

In the absence of encouraging federal signals, players in the cryptocurrency space can take solace in a welcoming embrace from one U.S. state: Wyoming. The state, whose motto is “Equal Rights,” passed legislation earlier this year which made utility tokens an asset class and exempted cryptocurrency from property taxation. Bloomberg has reported that after the legislation passed, at least two to three cryptocurrency companies have registered for business in the state per day.

Michael Terpin and Caitlin Long (Photo: Mark Albertson/SiliconANGLE)

“Hundreds of companies have registered in Wyoming in lieu of Delaware,” Caitlin Long, former president and chairman of Symbiont.io, said during a CoinAgenda appearance on Wednesday. “There are more to come for sure over time.”

After gaining passage of legislation receptive to cryptocurrency firms, Long is now involved in a new battle to open a bank that can be used by the state’s fledgling fintech companies. Although state legislators have indicated interest, there will likely be a struggle with federal regulators. Representatives from the Federal Deposit Insurance Corp. and the Federal Reserve recently pulled out of a meeting with crypto representatives to discuss the proposal, according to Long.

“It’s going to be an industry utility, owned by its members,” Long said. “We know that we’re taking on a fight with the Fed.”

Treacherous regulatory waters notwithstanding, one company has pushed forward with its mission to build identity-based tokens. Civic Technologies Inc. has developed a secure, decentralized identity service powered by the blockchain, after selling $33 million of its own tokens to investors.

The concept behind Civic is to store personally identifying information native to a device and then the blockchain provides a company receiving that data with certification that the consumer is whom they say they are. The application could be used to provide regulated products that require age or identity verification, such as alcohol, tobacco, sinus medication or perhaps even cannabis.

Civic offered a demonstration of its technology in practice earlier this year with a vending machine that dispensed beer. Walk up, scan a QR code embedded with Civic’s identity-based protocol, have the blockchain process the attestation and watch a cold one roll right out.

“If you have a digital ID, you should be able to have digital vending,” Vinny Lingham, Civic’s co-founder and chief executive, said during an appearance at CoinAgenda. “We’re calling it crypto-beer.”

The net takeaway from the dialogue in Las Vegas is that the cryptocurrency world is going to get a lot wilder before anything close to maturity sets in. Proclamations of a quadrillion-dollar industry and newly scalable blockchains offer hints of the volatile journey ahead.

In the end, those knee-deep in the cryptocurrency world remain firmly focused on making digital technology work for them as they build new companies. “I care about the developers, I care about the builders,” said crypto investor Pierce. “I don’t care about the speculators.”

A number of attendees in the room would probably drink a crypto-beer to that.

Support our mission to keep content open and free by engaging with theCUBE community. Join theCUBE’s Alumni Trust Network, where technology leaders connect, share intelligence and create opportunities.

Founded by tech visionaries John Furrier and Dave Vellante, SiliconANGLE Media has built a dynamic ecosystem of industry-leading digital media brands that reach 15+ million elite tech professionals. Our new proprietary theCUBE AI Video Cloud is breaking ground in audience interaction, leveraging theCUBEai.com neural network to help technology companies make data-driven decisions and stay at the forefront of industry conversations.

{kind=link}