CLOUD

CLOUD

CLOUD

CLOUD

CLOUD

ServiceNow Inc. is a company that investors love to love. But there’s caution in the investor community right now as confusion about transitory inflation and higher interest rates looms.

ServiceNow also suffers from perfection syndrome and elevated expectations. The company — which offers a workflow automation platform for tasks such as information technology service management, IT business management and IT operations management — has seen that the slightest misstep, or not beating earnings by a wide enough margin, can cause mini-freakouts from the investor community.

So it has architected a financial and communications model that allows it to beat expectations marginally and raise its outlook on a continuing basis. Regardless, ServiceNow appears to be on a track to vie for what Chief Executive Bill McDermott refers to as the next great enterprise software company. Wait, we thought Marc Benioff had taken that crown already….

In this Breaking Analysis we’ll dig into ServiceNow, one of the companies we began following almost 10 years ago, and provide some thoughts on ServiceNow’s planned march to $15 billion by 2026.

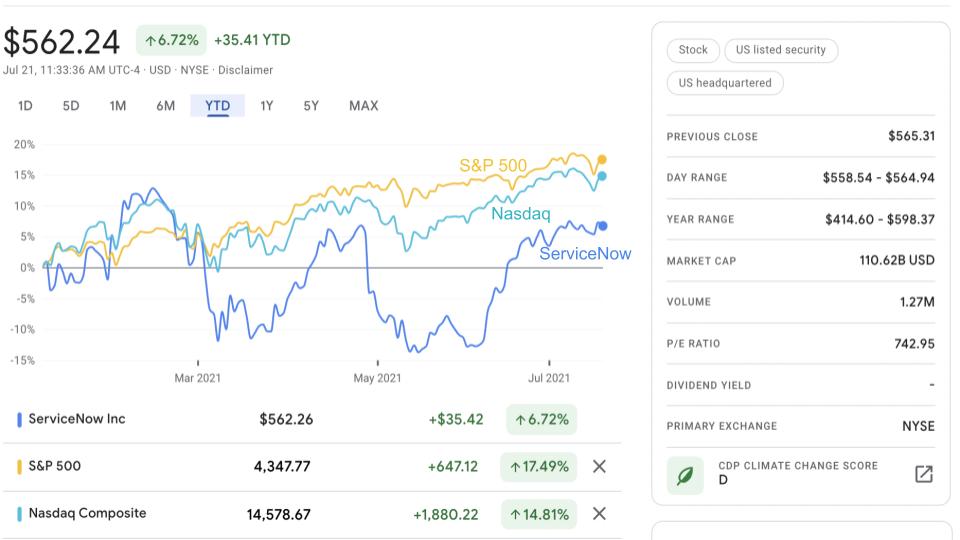

In 2020, despite the contraction in IT spending, ServiceNow outperformed both the S&P 500 and the Nasdaq. But below is a view of 2021 and you can see that although the stock has done well since it saw softness in May and again in early June, and bounced off that double bottom, its performance is below those other benchmarks.

This is not a big surprise given the fact that this is a high-growth stock and we all know that those names with high multiples get hurt in an inflationary environment, but still the gaps are notable. Investors we speak with are still very bullish on the stock but are fearful of getting caught in the downdraft of exogenous factors. But the vast majority continue to look for cheaper entry points as we saw this spring.

It’s not often that you see a company with $4 billion to $5 billion in revenue growing at a 30% clip, throwing off billions of dollars in free cash flow and increasing operating margins at 100 basis points a year. In fact, we don’t think we’ve ever seen that before.

Years ago, trade press and many analysts were criticizing ServiceNow for its lofty valuation and the fact that it was losing money. Then-CEO Frank Slootman said to this author that ServiceNow could be highly profitable tomorrow if it wanted to change its growth strategy. But he said this is a marathon and the company was planning to go big. Essentially Slootman was saying this company was going to be an ATM that prints money. His conviction has turned into reality.

Some of theCUBE team was at ServiceNow HQ in 2017, literally the first day on the job for John Donahoe, the CEO who replaced Slootman. After meeting him, Slootman and other leaders, we remember saying to ourselves, while Donahoe seemed more than capable, why the heck would the board let Frank Slootman get away?

Well, it turned out great for Slootman at Snowflake. Donahoe, we always felt, was a consumer guy anyway and not long for ServiceNow. And look how it turned out for ServiceNow.

McDermott ended up at the helm and there’s not a more qualified CEO for the company, in our view.

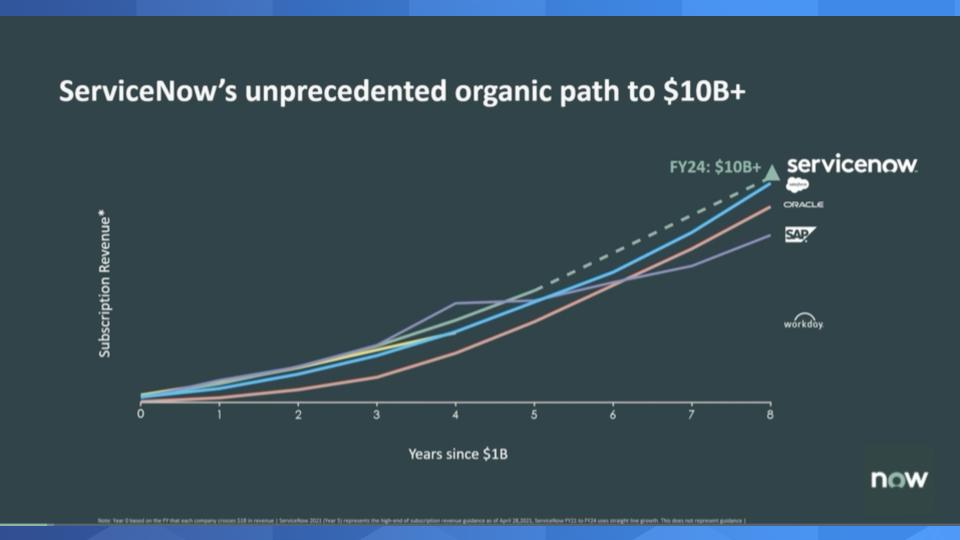

About two month ago McDermott led a virtual investor day event. We’ve had McDermott on theCUBE a couple of times back when he was CEO of SAP and this individual is very compelling. He has JFK looks and charisma, but more than that he’s passionate and convincing. He obviously knows enterprise software. And with conviction, he laid the groundwork for how ServiceNow will get to $10 billion in revenue by 2024 on its way to $15 billion two years thereafter.

Providing details of a path to forward revenue and profitability goals is a thankless task for CEOs and chief financial officers. Snowflake, for example, just had a similar investor day where CFO Mike Scarpelli laid out the company’s path to $10 billion. It typically goes unrewarded because the Street wants more and they want it faster. Although these execs lay out their plans with quite a bit of detail, they must be prudent and put forth targets that are achievable. Our bet is their internal targets are significantly more aggressive.

One of the important factors McDermott stressed was that ServiceNow will hit its goals without any massive M&A moves. That’s important because previously the door was left open for that possibility by his predecessors– that is, we’ll get to $10 billion and if we can’t do it organically, we may acquire to claim “Mission accomplished.” But now the company is assuring investors that it can achieve its targets organically, even with slower growth.

The chart above implies no big M&A – you can see Slootman handed over the reins at year one on the horizontal axis. This was not a turnaround story – it was a rocket ship at the time.

And look at the logos on this chart. This is a revenue view and ServiceNow is aiming to be the fastest to get to $10 billion in software industry history. ServiceNow’s valuation blew by Workday Inc.’s years ago. Its sights are set on SAP SE, which is currently valued at $170 billion, and then there’s Oracle Corp. and Salesforce.com Inc., with valuations at around $250 billion and $225 billion, respectively. These lines show the trajectory these companies took to get to $10 billion, and you can see how ServiceNow plans to get there with the dotted lines.

And this is in part why we called a collision course with Salesforce, because CEO Marc Benioff might say we already are the next great enterprise software company and we have no plans to give up that post anytime soon.

Here’s a clip from four years ago, talking about the pending clash of one titan (Salesforce) with an up-and-comer (ServiceNow). And ServiceNow, to its credit, blew through the projected $4 billion mark, which was set two regimes ago.

Now you may be thinking: Isn’t Salesforce’s revenue like five times that of ServiceNow, so how are they comparable? And the point is yes, but McDermott aspires to bring ServiceNow to that level and unseat Salesforce as the large, growing cloud-based SaaS company.

In addition, Salesforce has gotten to where it is with a lot of M&A – more than 60 acquisitions and some high-profile ones such as Slack Technologies Inc. and Tableau Software Inc. as well as MuleSoft LLC and Heroku back in the day – and many others. So we’ll see how far McDermott can get before he reverts to his acquisitive self from his SAP days.

But the second thing we’ll point out is that ServiceNow positions itself as the platform of platforms. ServiceNow runs its own cloud, and when it does acquisitions, it re-platforms the acquiree into the Now platform so that it can drive integrations more seamlessly.

And that means it’s somewhat limited on the acquisitions it can make without a heavy lift. It’s the power of the model, especially if customers can get to a single CMDB – configuration database management system — which by the way many customers never get to. Remember, ServiceNow is like the enterprise resource planning for IT, so the more you can get to a single data model, the more effective you can be.

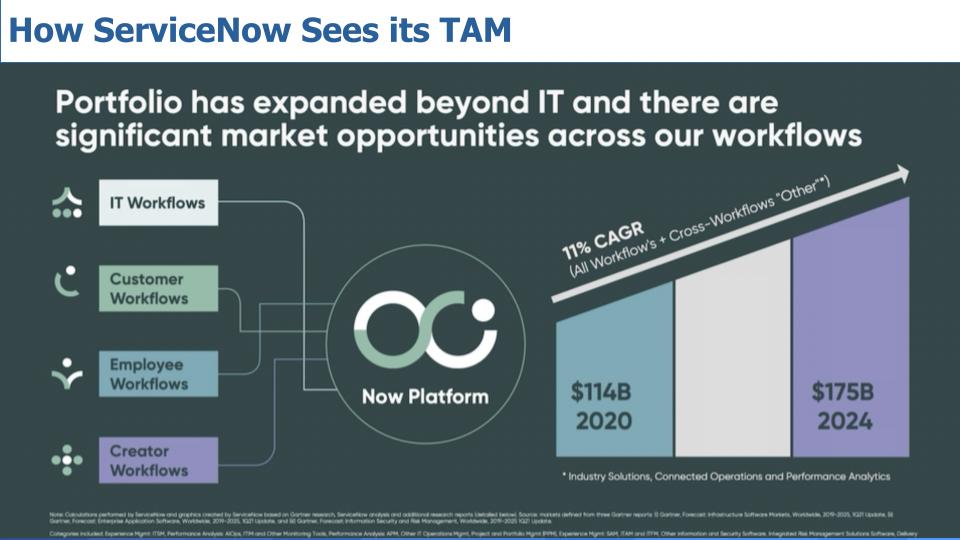

The other thing worth pointing out is ServiceNow wants to use this platform to attack organically what it sees as a very large TAM as shown below.

Now, a couple of points related to the market size: First, when ServiceNow sent public in 2012, many analysts said that it was way overvalued because help desk and writing tickets was a $2 billion business in decline and BMC Remedy wasn’t really that big of a base to attack. In 2013, the Wikibon team took a stab at sizing the total available market and we had it well over $30 billion as we expected the company to move deeper into IT and then beyond into lines of business management. We felt we were being conservative but thought putting a number like $100 billion number out there was too aggressive.

But what we see now is all these software opportunities coming together, systems of workflow, automation, machine intelligence and other functionality. ServiceNow in a way can double-dip both in and beyond. For example, it can partner with HCM vendors and also offer employee workflows as part of its software. It can partner or even purchase robotic process automation tools from specialists such as UiPath Inc. and Automation Anywhere Inc. and it can acquire a company such as Intellibot and integrate lighter-weight RPA function into its platform. So it can manage workflows for best-of-breed software products, do so across clouds and pick off functionality to add into its own software stack.

Now what’s interesting in the TAM chart above is first the size of the TAM ServiceNow sees – $175 billion — but also how it’s now reorganizing its business around workflows shown on the left. This was done, of course, to simplify the many functions you can buy from ServiceNow.

But there’s also speculation that ServiceNow is leveraging its orchestration and service catalog capabilities, which are meaningful, and using them to power these workflows because the way it was organized previously was confusing for customers and sellers. As such, it created friction in the customer base and was not as effective as it could be.

It’s well known that ServiceNow’s ITSM business comprises the biggest piece of its revenue pie and it’s adding to that with ITSM Pro and ITSM Enterprise. And its ITOM business is doing well against the likes of DataDog, Elastic NV, Splunk Inc. and the like — and its acquisition of LightStep Inc. pushes it further into this market, which is both crowded and morphing into observability. as we’ve reported.

What is unclear is how well ServiceNow’s human resources and customer service management businesses are doing, and so this is potentially a way not only to simplify, but to shuffle deck chairs a bit and prop up the non-IT workflows.

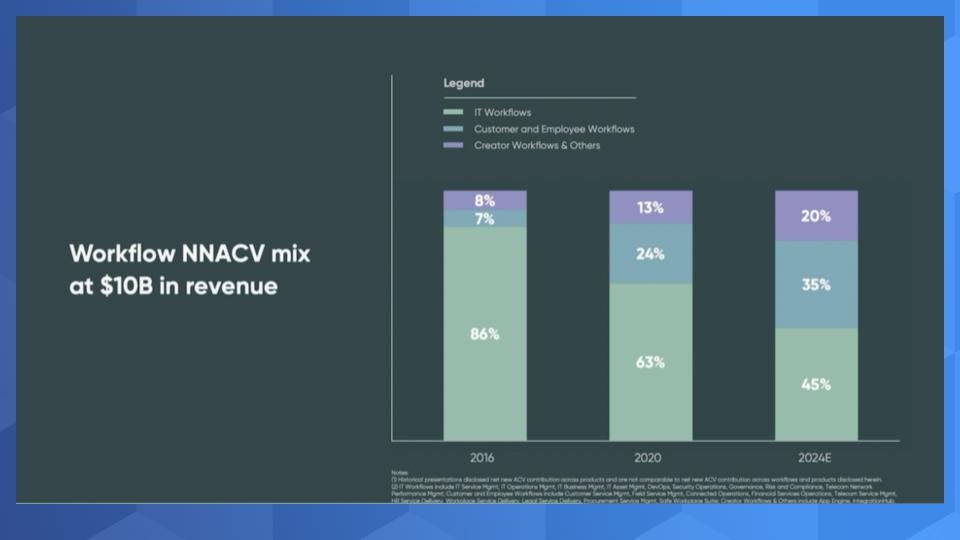

The move, we suspect, allows ServiceNow to show the chart below to investors:

The implication to the Street is: “See we have this huge TAM and our TAM expansion strategy is working as the overall business is growing nicely, including the IT workflows, and the mix is shifting toward customer, employee and creator workflows – see how awesome our business is and how much room we have to grow.”

This new view is possibly a way to hide some of the warts and accentuate the growth. Look, there’s not a lot to criticize this company about, but it has been good at featuring what some perceive as weaknesses — like the way it marketed multi-instance as a better model, even though the cloud world was all multitenant. And with ServiceNow you have to really plan new releases, which it drops every six months.

But to the company’s credit, CJ Desai, ServiceNow’s head of products, did say at the investor meeting that it does certain releases bimonthly and even some biweekly. So it’s maybe a bit of nitpicking here, but we always question the motives when such changes are made to reporting structures.

And if workflows are the new logical construct, one has to wonder, will ServiceNow start pricing by workflows versus what really has been a legacy “what’s your ticket volume and how many agents need access model”? We’re not ServiceNow pricing experts, but the company doesn’t make it easy to figure out fees, so let’s keep an eye on how this evolves.

The other thing to watch is deals over $1 million. It looks like that metric was softer last quarter and though large deals tend to be lumpy, we should keep an eye on this.

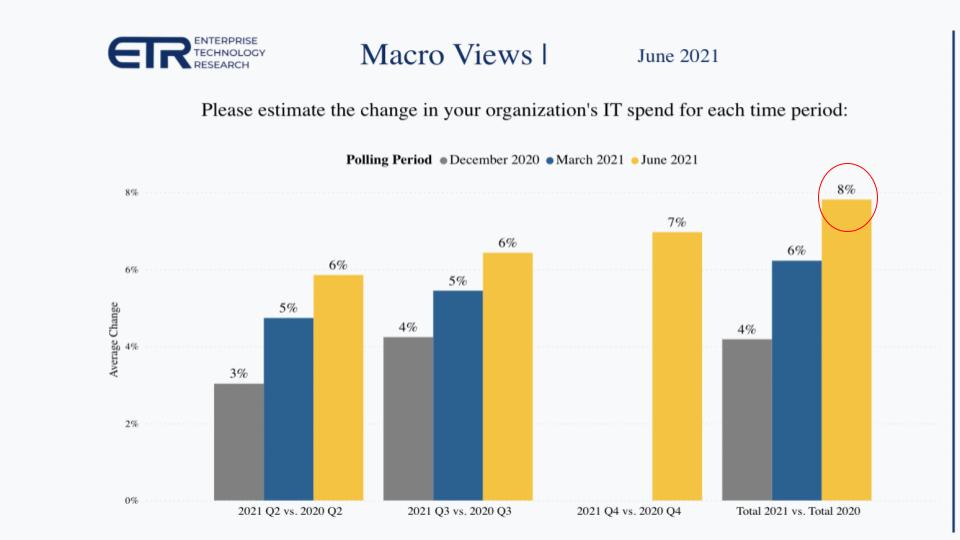

First, let’s take a look at the latest update on IT spend from Enterprise Technology Research. This is especially relevant for ServiceNow as the chief information officer/IT budget is still the company’s mainspring of revenue. We’ve been consistently saying expect a 7% to 8% growth in 2021 spending off last year’s contraction and the latest ETR survey data puts it right at 8% as shown below, so we like that number. It could even be higher and push 10% this year.

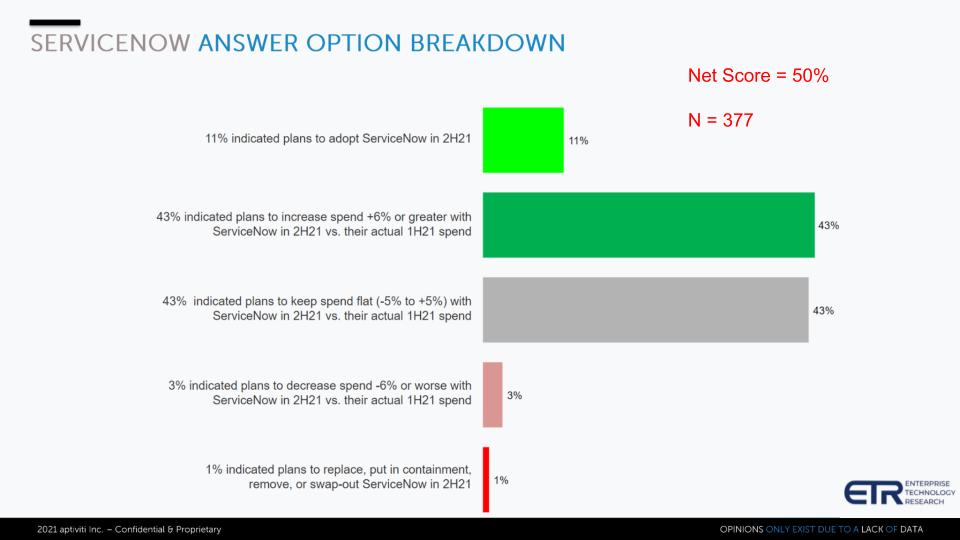

Below we show the spending profile for ServiceNow customers within the ETR data set. Of the 1,100-plus respondents this quarter, there were 377 ServiceNow customers responding.

The data show the breakdown of Net Score among those respondents. Remember Net Score is a measure of spending velocity. It is calculated by taking the lime green bar, which is adopting new – 11% of the respondents. It adds the forest green bar – growth in spending of 6% or more, which is 43% of the ServiceNow customer respondents, and then subtracts the reds, comprised of the pink – spending less – that’s 3%. And the bright red is leaving the platform – that’s a miniscule 1% of respondents. Spending more minus spending less equals Net Score.

ServiceNow’s Net Score of 50% is well above the 40% elevated mark that we like to see. It’s rare for a company of this size, except for the hyperscalers; and oh, there’s this other great enterprise software company at 45% – that’s Salesforce.com. But it’s rare to be that large and have that much spending momentum in the ETR surveys.

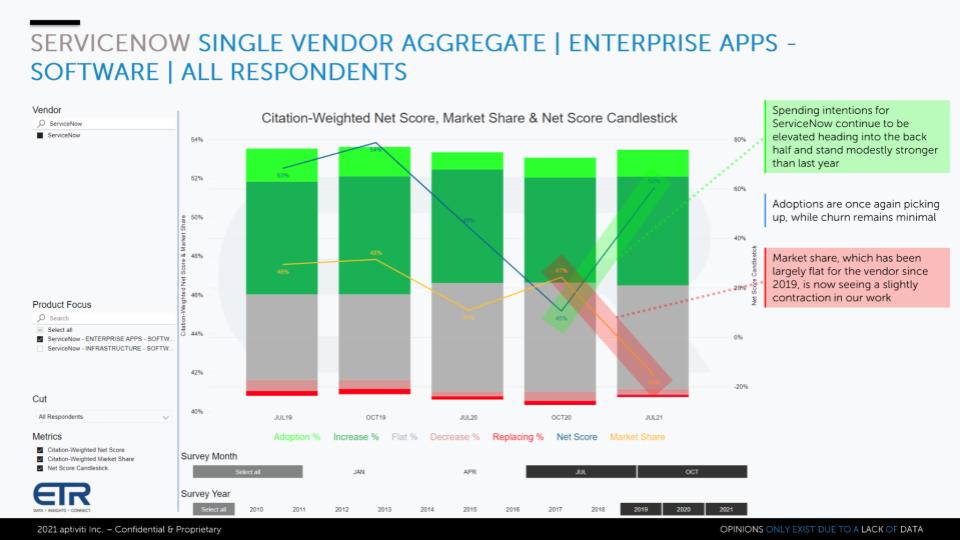

Let’s take a look at the time series data for ServiceNow:

The chart above shows the Net Score granularity going back two years to the July 2019 survey. The blue line is Net Score, and you can see it was dragged down during last year’s lockdown. It’s now spiking back toward pre-COVID levels, which is a very positive sign for the company. The red call-out, which shows Market Share – that’s an indicator of pervasiveness in the data set – is decelerating, but we’re not overly concerned about that. We don’t think that’s a meaningful indicator of ServiceNow broadly in the marketplace because its revenue is skewed toward some big spender accounts. The ETR view is an account “unit” indicator, not a spending-level metric.

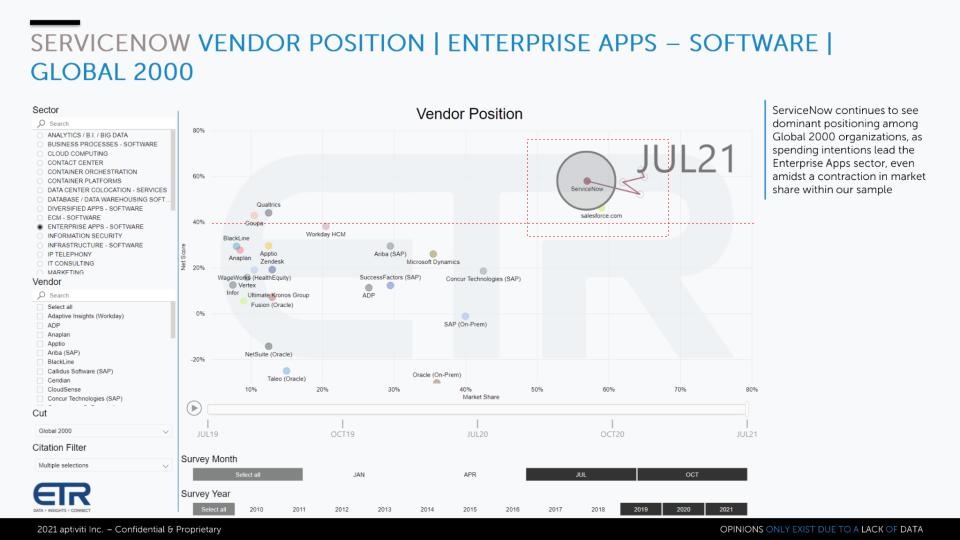

The chart below is another reason we’re not overly concerned about ServiceNow’s Market Share as ETR defines it:

This is an X/Y view with Net Score on the vertical axis and Market Share on the horizontal plane for enterprise software. Remember that 40% red line is the elevated level – anything over that is indicative of strong spending momentum. Look at the two leaders: Salesforce and ServiceNow.

Again we see these two companies as not direct competitors today, but as ServiceNow expands its TAM, they will increasingly collide in our view.

CEO McDermott would say, as would his predecessors, that ServiceNow is a platform of platforms. We partner with other software companies and meet at the customer. Sure, we’ll integrate functions where we think it can add value to customers, but we also understand we have to work with the vendors our customers are using, so it’s all good.

But anyone who has ever been around the enterprise software industry knows that software execs and salespeople believe that virtually every dollar spent on software should or at least could go to them. And if it’s a good market, they can organically write software to deliver customer value or they can acquire to fill gaps. So although what McDermott would say is true – Oracle, Microsoft, SAP, Salesforce, Infor and the like all want as big a budget pie as they can grab.

That’s just the way it is.

We’ll close with some anecdotal comments from ETR Insights (formerly called VENN), which is a roundtable discussion with CxOs.

You can read these in detail, but we’ll make some comments on the first and third call-outs.

This first comment comes from an assistant vice president in retail who says ServiceNow is a key part of their digital transformation. It moved off BMC Remedy two years ago for the global ticketing system. And this person is saying that although the platform is extremely powerful, you have to buy into specific modules to get a feature and you may not need much of the capability – so it gets expensive.

The other thing this individual is saying is that initially it’s a services-heavy project. And we would advise that when you look at the ServiceNow ecosystem, the big system integrators have big appetites and they want big clients with big budgets. If you’re not one of the top 500 or 700 customers, the big-name SIs may not be for you.

So what we would suggest is you get in touch with someone like Jason Wojahn of Thirdera or a more specialized ServiceNow consultancy like them. This is because you’re going to get better value for the money, get to short-term return on investment faster and make long-term, sustainable ROI a measurable objective with a partner that understands ServiceNow and doesn’t require a massive budget.

The third comment sums it up nicely. The ServiceNow platform is integrated. It’s not a bunch of stovepipes and cul-de-sacs. Yes, it’s expensive, but people love it and, like the iPhone, it just works. And the feature pace is accelerating.

That’s a pretty strong testimonial. So let’s keep an eye on price transparency and any possible backlash there and how the ecosystem evolves. It’s something we called out early on as an indicator and ServiceNow needs to continue to invest in that partner network, especially as it builds out its vertical industry practices and expands internationally.

And let’s see how the lumpiness of the larger deals, that is those of over $1 million annual contract value, play out in the next several quarters.

Remember we publish each week on Wikibon and SiliconANGLE. These episodes are all available as podcasts wherever you listen.

Email david.vellante@siliconangle.com, DM @dvellante on Twitter and comment on our LinkedIn posts.

Also, check out this ETR Tutorial we created, which explains the spending methodology in more detail. Note: ETR is a separate company from Wikibon and SiliconANGLE. If you would like to cite or republish any of the company’s data, or inquire about its services, please contact ETR at legal@etr.ai.

Here’s the full video analysis:

THANK YOU