CLOUD

CLOUD

CLOUD

CLOUD

CLOUD

Broadcom Inc.’s acquisition of VMware Inc. is proceeding almost exactly as we expected when the deal was announced in May 2022.

Although much of the media and competitor narrative is focused on the increased license fees Broadcom is imposing and the urgency of migrating off VMware, customer conversations and recent surveys show that though migrations are happening, the real story is that VMware’s more narrow focus and cost discipline are allowing Broadcom to integrate VMware into its highly successful business model.

Specifically, we see two seemingly countervailing trends that are both possible to be true: 1) Customers are actively moving many low-value workloads off VMware; and 2) Most mission-critical work is staying put, allowing Broadcom to dramatically increase the contribution from its software business and deliver a roadmap for customers that will often be more cost-effective than migrating.

In this Breaking Analysis, we share results from a recent survey from Enterprise Technology Research and provide our latest thinking on the often discussed and frequently maligned VMware acquisition — and why it’s a win for customers, competitors and Broadcom specifically.

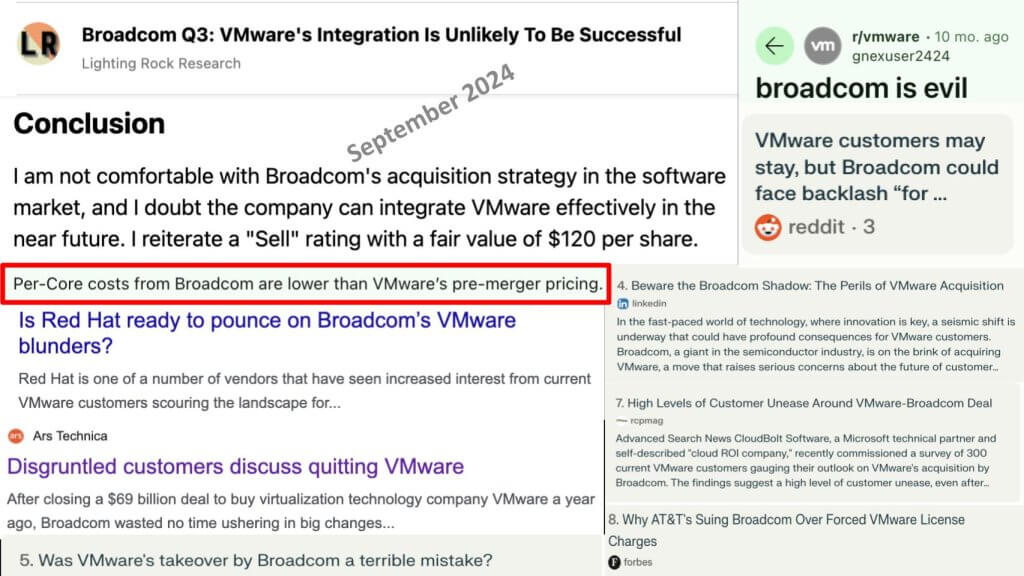

It’s easy to find negative sentiment in the press, social media and Reddit threads about the changes Broadcom has imposed with respect to ending perpetual licenses and limiting the bespoke options across the VMware portfolio.

Many headlines underscore the negative sentiment toward Broadcom’s moves. But the company has been unapologetic and, quite the opposite, optimistic with customers, strongly marketing the economic benefits of going all in on the VMware Cloud Foundation bundle.

One notable comment in a reddit thread highlighted above in red is that by some measures, costs are actually lower than acquisition. At first blush, this is hard to swallow given the price increases that customers have seen when it’s time to renew their maintenance agreements.

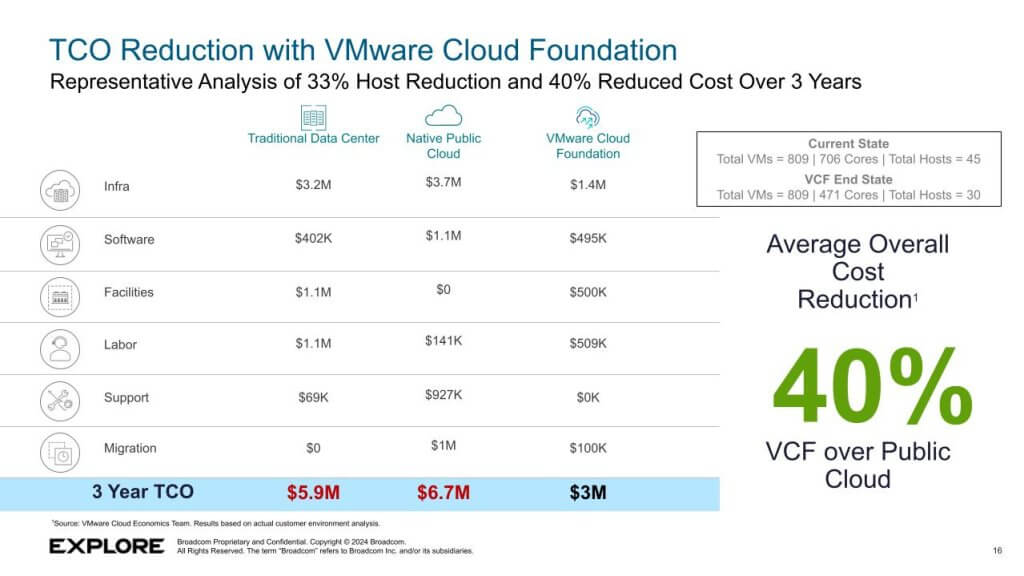

To its credit, Broadcom has done extensive total cost of ownership and economic analysis that appears quite defensible. The caveat is a key assumption in the calculations is customers go all-in on VMware Cloud Foundation or VCF. As shown in the chart below, relative to traditional data center costs and public cloud, VCF is “less expensive.”

[VMware note: This is a representative analysis only. There is no discounting applied to any of these numbers in this representative model. Native Public Cloud Numbers come from list pricing available on public websites.]

The chart above shows a head-to-head comparison with traditional data centers comprising bespoke software, public cloud and VCF. What it doesn’t show is an “As-is” and a “To-be” relative to existing customer installations. Nonetheless, in an interview on theCUBE in August of this year we dug into this issue with Drew Nielsen, who leads cloud economics analysis at Broadcom. We pressed on the assumptions and methodology VMware analysts used in this chart.

[Watch the full discussion on VMware economics]

Our bottom line is that despite near-term license cost increases, we found the long-term economic analysis to be compelling in the sense that it will capture the attention of senior executives. It’s a classic Broadcom playbook as applied to VMware:

Whether you buy the pitch or not, before trying to do a wholesale migration of VMware, you’d be wise to do your own economic impact analysis.

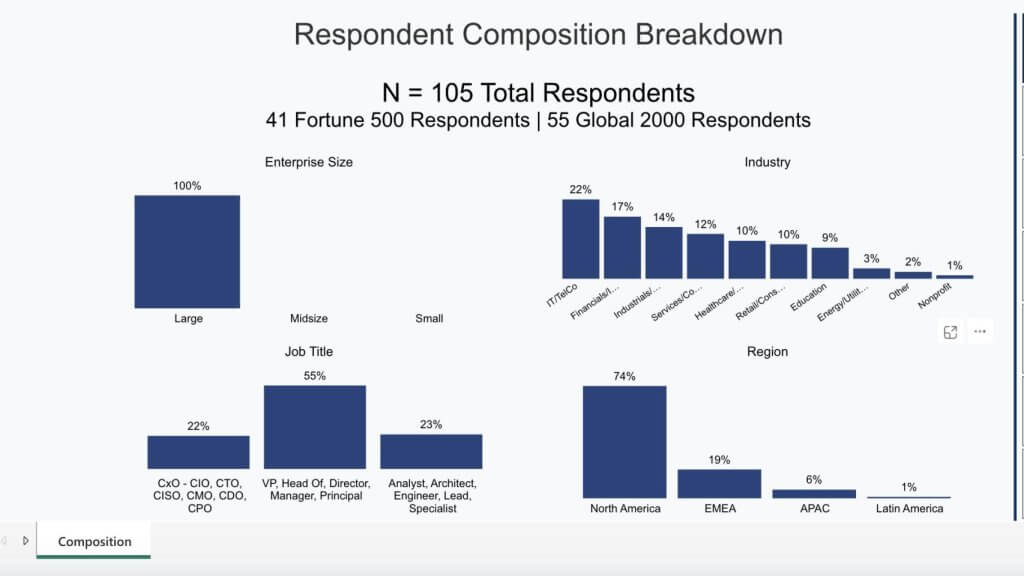

In October of this year, ETR conducted a small survey of information technology decision makers or ITDMs. The demographics are shown below.

The survey explicitly focused on large customers across a variety of industries with a bias toward North American respondents. As shown above, ETR captured a nice mix of C-level titles, mid-level managers and practitioners in the survey.

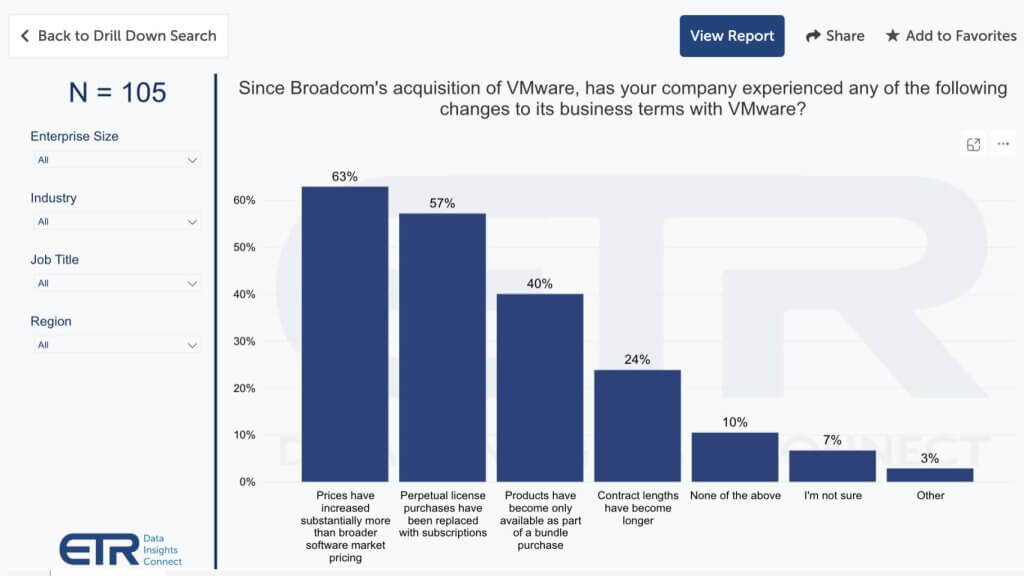

The chart below highlights the impact respondents have seen from the changes Broadcom has implemented to VMware packaging and pricing. The hallmarks of the new pricing and packaging strategy are shown in the first three bars starting with the third bar and working left:

Though the N in the sample is small, it represents the anecdotal feedback we’ve had from customers in the big three areas of impact. Note we cited at least 80% of respondents as affected, accounting for the 7% citing “I’m not sure.”

The previous TCO analysis we described above assumes customers go all-in on VCF. As shown below, that is not the predominant procurement model today and underscores why we feel Broadcom has significant upside to its VMware business.

This strategy was highlighted on the last earnings call by Broadcom Chief Executive Hock Tan, who stated:

The transformation of the business model of VMware continues to progress very well. In fact, last week, we held a well-attended VMware Explore Conference in Las Vegas, our first as a combined company. This event was all about promoting VMware Cloud Foundation, or VCF, which is the full software stack that virtualizes an entire data center and creates a private cloud environment on-prem for enterprises. The success of this strategy is reflected in our performance in fiscal Q3.

Many narratives from the media and competitors suggest that customers are angry, they’re migrating and calls for help are numerous. All of these are true based on our assessment. At the same time, research shows that customers are not migrating their entire estates. This is the win-win we cited in our opening premise.

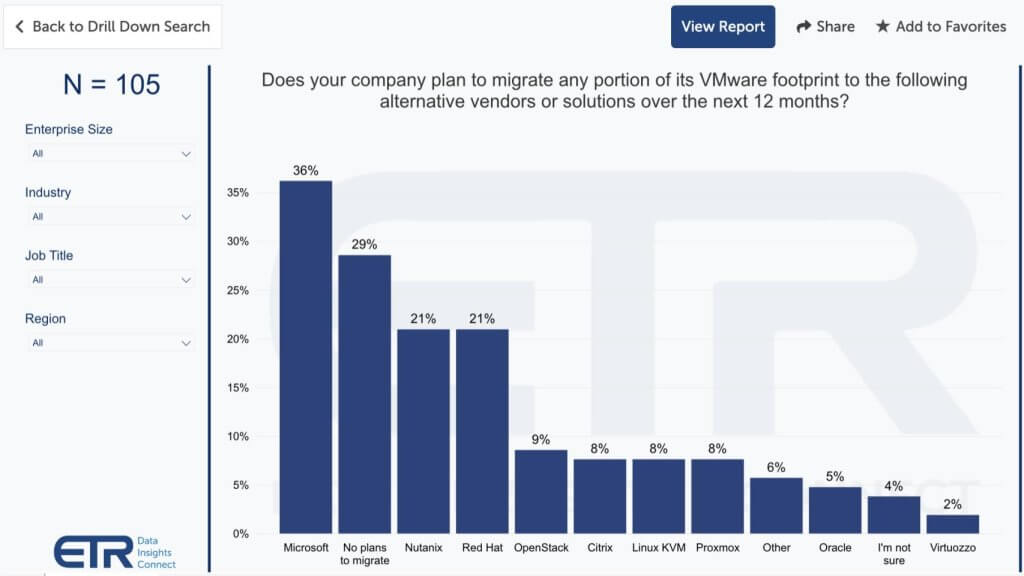

Let’s first look at where customers are moving as shown below.

Notably, 36% of customers cite Microsoft Corp. and it’s likely they’re moving to AVS (Azure VMware Solution), which is a managed private cloud offering from Microsoft that essentially bundles VCF, including key elements such as vSAN. From a licensing perspective, customers can acquire VCF from Microsoft or bring their own VCF licenses. The managed-service aspects are compelling for many customers and allow firms to basically eliminate VMware admin staff.

Nearly 30% of respondents in the survey have no plans to migrate, with Nutanix Inc. and Red Hat Inc. vying for the next options behind Microsoft. Followed by other opens including open source alternatives and a few other names.

The Microsoft Azure option that Broadcom allows is a dramatic shift from the previous VMware cloud strategy. Readers of this series may remember that at one point VMware tried to compete directly with Amazon Web Services Inc. When that strategy failed, the company pivoted and made AWS a preferred partner with VMware Cloud on AWS, which gained significant traction. VMware also cut deals with other hyperscalers and cloud providers, but AWS was its preferred option.

Why is this change significant? After years of hand-wringing, navel-gazing and market confusion, legacy VMware effected a strategy that relied on partnerships with cloud players, sharing the wealth. This made sense during the “cloud-first” era and supported customer wishes to run VMware in the cloud.

Broadcom has killed this strategy for the following reasons:

Historically, Broadcom’s software operating margin is above 70%. We believe that over time, VMware operating margins will follow suit and be nearly as high as most SaaS firms’ gross margin.

Several industry surveys indicate a large proportion of customers are looking to migrate off VMware. On an account basis it’s perfectly reasonable that a much higher percentage than the 29% shown in the previous graphic above are looking to move some workloads, especially as the ETR respondents were exclusively from large customers. We’ve seen surveys that even show nearly 50% of customers are looking to migrate some workloads.

The natural reaction is to conclude that Broadcom has made a big mistake shelling out $69 billion for VMware.

But migrations are hard and almost always more expensive than staying put. It’s true that in legacy markets such as VMware, the risk of lock-in and price gouging are real threats. Broadcom’s calculus is to construct a strategy where customers get more value by staying with the platform. Their promise is, despite the new packaging, crackdown on perpetual licenses and more revenue they’re extracting, the company will:

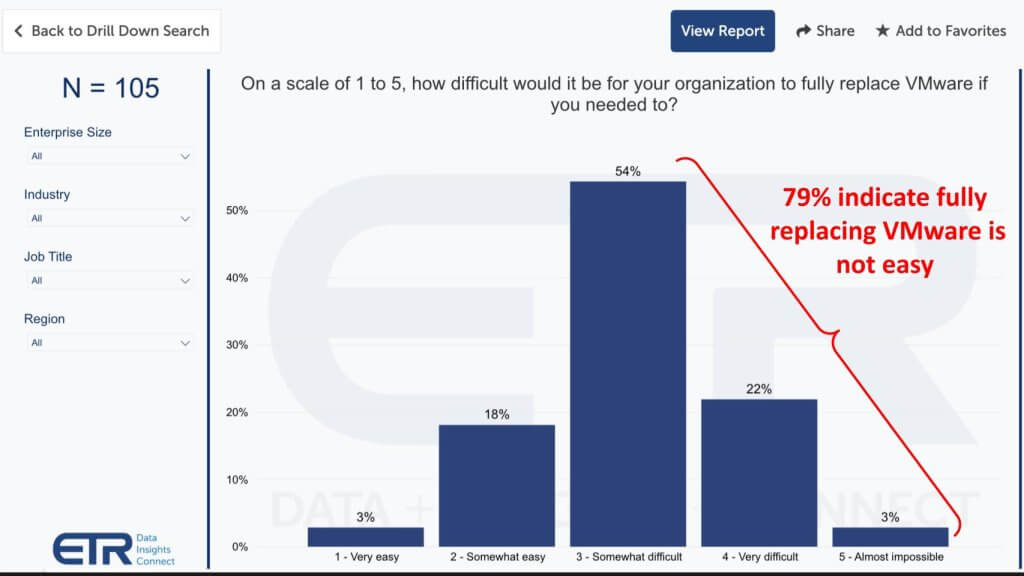

Below is a final datapoint that gives some indication of the non-trivial nature of migrations. Taking into account change management, business process disruption, application portfolio impacts, skills required, error rates and the effort to abstract away the complexity of migration pain, in many cases the juice, as they say, isn’t going to be worth the squeeze.

It seems counterintuitive that Broadcom, by completely altering VMware’s packaging, pricing and partnership strategy, would be a win for anyone other than Broadcom. But the reality is the world needs a viable on-prem alternative to public clouds. Initiatives such as Project Monterey, the Nitro-like functionality VMware continues to pursue, are necessary to keep pace with cloud innovators. Here’s the logic behind our thinking:

For customers. You are going to pay more for Broadcom to pursue a streamlined roadmap. The downside is the checks your write to Broadcom will be larger but at the same time you won’t have the latest VMware acquisition du jour jammed down your throat; and you ideally won’t have to deal with a collection of less than ideally integrated and offerings. Not all workloads are going to yield better ROI and lower TCO over the long run, so you should perform a workload rationalization exercise and decide what to keep on VMware, what to migrate, which workloads to kill immediately that aren’t delivering any value, and what to let die through attrition. You may find that this exercise helps pay for the Broadcom hit.

For competitors. Broadcom’s non-GAAP operating margins are historically above 60% and four to six times better those of most virtualization competitors and partners (Dell Technologies Inc., Nutanix, Red Hat/IBM, Hewlett Packard Enterprise Co. and the like). Microsoft is the obvious exception. As such, the business Broadcom is pushing away is likely at least as profitable for these firms as their existing business. It can drive new top-line revenue and open up new vectors of growth in a market that previously was untouchable with VMware’s historical model.

For Broadcom and its investors. A price of $69 billio is hefty. It brings new debt to Broadcom that has to be managed, especially with today’s higher interest rates. But VMware is on track to hit $4 billion in quarterly revenue and $8.5 billion in adjusted EBITDA. Originally Broadcom promised the latter result within three years of the acquisition but is on track to achieve or exceed that goal in FY 2025.

Back-of-napkin math: Broadcom’s valuation is roughly 25 to 30 times adjusted EBITDA. At an $8.5 billion EBITDA target, that’s roughly $200 billion to $250 billion in incremental market value in less than the promised three-year timeframe. Of course, valuations can fluctuate, but that’s at least a 3X return in valuation terms to shareholders in a couple of years.

Take into consideration that Broadcom’s commentary on its earnings calls and anecdotally in the field speaking with customers suggests that VMware is a long-term play that will pay significant dividends in the future.

Our belief is that much of the trade press negative narrative is misplaced. While competitors to VMware are undoubtedly seeing activity, the conclusion that this spells bad news for Broadcom and VMware is also misguided.

Our advice to customers remains the same:

Moreover, customers should spend ample time understanding VMware’s AI roadmap. We’ve always had concerns in this regard given VMware’s lack of a coherent data play. “Good” data is increasingly becoming the No. 1 obstacle in executing successful AI strategies and it’s unclear how VMware helps in this regard. We don’t fully understand the company’s strategy and ecosystem partners approach when it comes to data that feeds AI.

On balance, however, we believe Broadcom is executing ahead of expectations on its VMware progress and is establishing the basis for a long-term platform asset that will be an industry force for the next decade and perhaps beyond.

THANK YOU