NEWS

NEWS

NEWS

NEWS

NEWS

RedMonk analyst Rachel Stephens has just updated the firm’s analysis of the price differences among the top cloud Infrastructure-as-a-Service (IaaS) providers for the first time in two years. The most striking thing about the report, IaaS Pricing Patterns and Trends, is it shows that the trend of constant price cuts seems to have bottomed out.

Stephens’ findings suggest that providers seem to be growing wary of trying to be the cheapest on the market, and are instead focusing on one price point.

There is one notable exception to this trend however, in the shape of Google. It’s no secret that Google lags some way behind Amazon Web Services (AWS) and Microsoft Azure, and the analysis shows that it’s still trying to differentiate on price by massively undercutting the competition in both compute units and in-memory pricing.

As with any analysis of this type, there are lots of caveats to be aware of. Because providers structure their price plans in a way that makes apples to apples comparisons effectively impossible, Stephens compared list prices instead of actual prices. It’s also worth noting that Hewlett-Packard Enterprise (HPE) no longer publishes pricing for its Helion cloud, so its been omitted from the analysis altogether. Stephens also tried to add Oracle to her analysis, but was unable to obtain pricing and was forced to exclude the company.

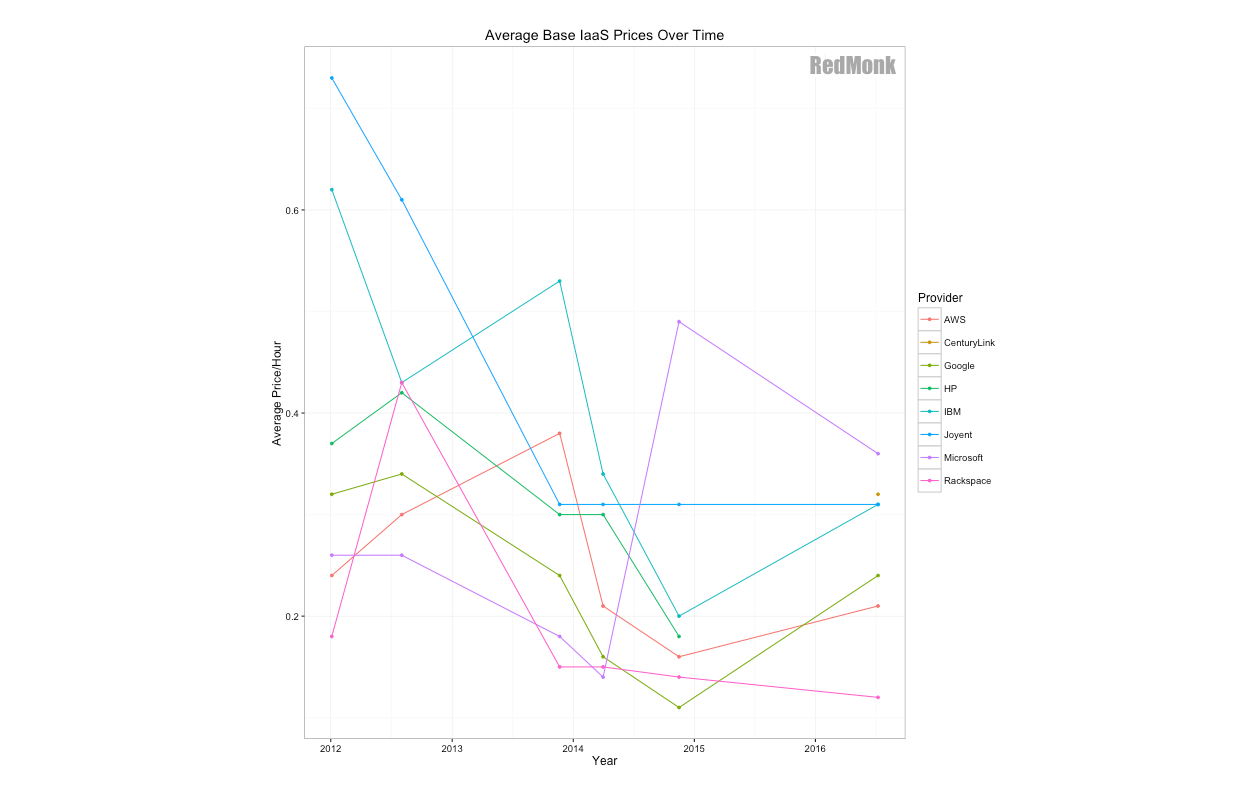

Much of the analysis simply reinforces what many of us have already known about the market, but RedMonk’s price comparison charts for disk space by price/hour, memory by price/hour and compute units by price/hour are still worth a look if you’re interested in seeing which providers stand out and where.

More interesting is the last chart, which shows each vendor’s average base IaaS prices and how they’ve evolved over time. Back in 2014, every vendor’s prices were moving in a downward trend, with the sole exception of Microsoft. This time around, the results are a mirror image, with Microsoft the only vendor showing a significant downward trend in its prices, while all the other’s prices are either static or slightly higher.

“One interpretation of this development is that infrastructure is reaching a commodity status,” Stephens wrote. “Google in particular is still attempting to differentiate itself via price offerings, but generally speaking this analysis showed increased clustering of many of the providers’ offerings.”

But just because providers are no longer competing as aggressively on price as they once were, by no means is it an indication that competition will be any less fierce. Instead, the analysis indicates that providers are looking to differentiate themselves through the strength of their products and services alone, betting that customers will be willing to pay whatever is asked so long as it offers value.

THANK YOU