INFRA

INFRA

INFRA

INFRA

INFRA

Investors hammered Nutanix Inc.’s shares today as the maker of enterprise computer virtualization and storage appliances and software beat analysts’ quarterly expectations but issued a weaker-than-expected outlook for the current quarter.

The company reported a fiscal-second quarter loss before certain costs such as stock compensation of 28 cents a share. Revenues rose 77 percent, to $182.2 million. Analysts on average had expected a larger loss of 35 cents a share on $178.4 million.

The company, which went public last fall in a blockbuster offering, sells “hyperconverged” systems that combine computing, storage and software into a single machine to provides a cloudlike setup on customers’ own premises, said it expects to post a loss of 45 to 48 cents a share on revenues between $180 million and $190 million.

Investors didn’t like it, knocking the shares down more than 14 percent in after-hours trading. Nutanix’s stock had risen 1.3 percent, to $31.12, in regular trading today. That was already down considerably from the immediate post-IPO high of $46.78.

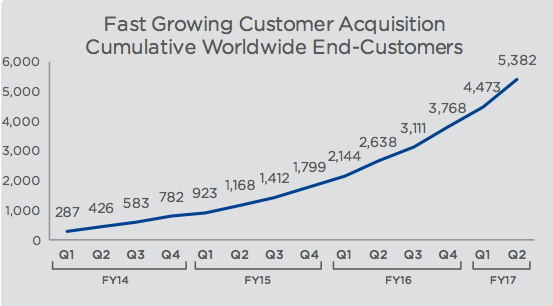

Nutanix Chief Executive Dheeraj Pandey (pictured) emphasized the company’s sales momentum during the earnings conference call, with 900 new customers in the quarter, up from 700 in the first quarter, for a total of 5,300 customers. He also said the company’s “land and expand” sales model, with customers of 18 months or more averaging almost four times their initial purchase levels.

Nutanix Chief Executive Dheeraj Pandey (pictured) emphasized the company’s sales momentum during the earnings conference call, with 900 new customers in the quarter, up from 700 in the first quarter, for a total of 5,300 customers. He also said the company’s “land and expand” sales model, with customers of 18 months or more averaging almost four times their initial purchase levels.

But the company also shed some light on the lower-than-expected third-quarter guidance. Chief Financial Officer Duston Williams said Nutanix had fewer-than-expected deals of more than $500,000 a quarter, mostly in North America. He said the company may have underestimated the impact on productivity of promoting some of its most successful sales reps into management, but he said that productivity should rebound in the next few quarters.

Williams said its outlook is conservative, taking into account a seasonally slow quarter and moves to fix North American salesforce productivity. He also expects a 30 percent to 40 percent increase in DRAM memory chips prices in the third quarter alone, but it’s uncertain whether Nutanix’s own product price increases will offset that.

Analysts ratcheted down their expectations after the report. Morgan Stanley analysts, for instance, set a new target price of $20, down from $29, for several reasons. For one, Hewlett Packard Enterprise Co.’s recent acquisition of SimpliVity and Cisco’s recent success with HyperFlex mean more competition as well as fewer potential selling partners for Nutanix’s software, leaving the company more dependent on lower-margin hardware sales. Moreover, expiration of a post-IPO selling hold on some 84 million shares on March 28 as well as changes to the U.S. sales force could pressure growth and profits.

Support our mission to keep content open and free by engaging with theCUBE community. Join theCUBE’s Alumni Trust Network, where technology leaders connect, share intelligence and create opportunities.

Founded by tech visionaries John Furrier and Dave Vellante, SiliconANGLE Media has built a dynamic ecosystem of industry-leading digital media brands that reach 15+ million elite tech professionals. Our new proprietary theCUBE AI Video Cloud is breaking ground in audience interaction, leveraging theCUBEai.com neural network to help technology companies make data-driven decisions and stay at the forefront of industry conversations.