INFRA

INFRA

INFRA

INFRA

INFRA

Updated:

In its first quarter as a newly public company, Dell Technologies Inc. today reported marginally better-than-expected quarterly revenue growth but a higher-than-expected net loss.

The 9 percent revenue growth was centered in servers and networking gear as well as in Dell’s share of the spoils from its 80 percent ownership of computing virtualization giant VMware Inc., which also reported upside results today.

The computer, storage and data center services giant reported its net loss for its fiscal 2019 fourth quarter more than doubled from a year ago, to $287 million, on revenue of $23.84 billion. Before interest payments, adjustments on the value of its equity investments and certain other costs, it earned an operating profit of $2.7 billion. Analysts had expected a much lower net loss of $45 million on revenue of $23.83 billion.

It was difficult to gauge year-over-year changes because Dell didn’t initially provide per-share profits, which is the way Wall Street customarily track profits, because share counts changed mid-quarter thanks to the transaction that brought Dell public again. But later it pegged the adjusted profit at $1.86 a share, a bit above the consensus $1.81.

Dell also didn’t provide guidance for future quarters or the year.

Perhaps a bit uncertain about what to think, investors pushed shares up only about 1 percent in initial after-hours trading. Shares later wavered up and down a point or so before settling down about a half-point. Update: After sleeping on it, investors felt more confident, with shares rising nearly 3 percent Friday.

Shares before today had risen 15 percent on the year, better than the S&P 500 index’s 11 percent, and had jumped 20 percent in the last month alone. In regular trading today, the stock fell three-quarters of a point, to $55.82 a share.

In prepared remarks, Chief Financial Officer Tom Sweet cited double-digit revenue growth for the full year across all three of its business units and as well as “profitable share gains” across its product portfolio. “In fiscal 2020 we’ll continue to run the business in a disciplined way,” he said. “We will remain focused on generating long-term relative growth, share gain and cash flow while driving long-term value for shareholders and serving our customers’ full range of needs.”

Enderle Group analyst Rob Enderle took that to mean that Dell not surprisingly will be focused on cutting costs. “I would expect Dell going forward to work harder to contain their losses than this quarter reflected,” he told SiliconANGLE.

But Dell also is showing strength relative to some traditional rivals. For example, Hewlett Packard Enterprise Co. last week reported a 2 percent quarterly decline in revenue, breaking a four-quarter string of higher sales.

“Growth is impressive for such a large, $90 billion-plus company — quite impressive that such a large whale can show that type of growth,” said Dave Vellante, chief analyst at SiliconANGLE sister market research firm Wikibon.

For the year, Dell said it reduced its operating loss by 92 percent, to $191 million, and earned an adjusted operating profit of $8.9 billion, up 14 percent from fiscal 2018. Net loss fell 25 percent, to $2.1 billion.

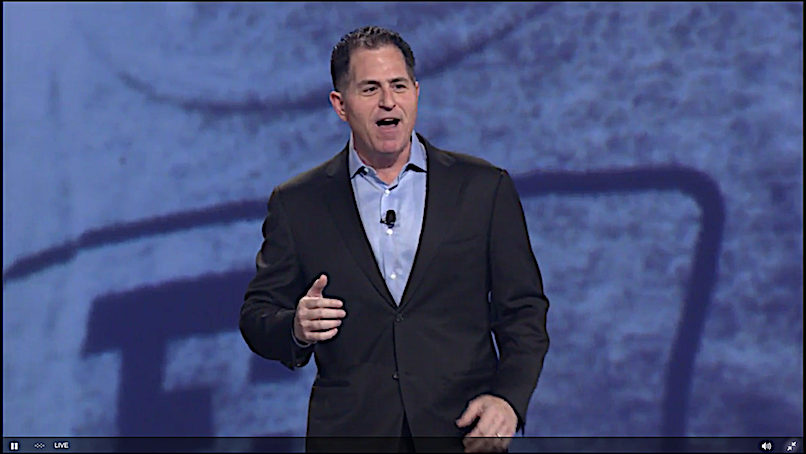

A remaining question has been how quickly the company founded by Chief Executive Michael Dell (pictured) can pay off the remaining $50 billion in debt from its $67 billion purchase of storage giant EMC Corp. in 2016. It said today it has paid down $14.6 billion since the EMC deal closed.

About $1.3 billion of that was paid down in the third quarter. In the fourth quarter, it paid off only $200 million, apparently because of $5 billion in additional debt incurred in the process of returning to public-company status.

“The key issue remains the balance sheet and that’s why the stock is trading the way it does,” said Vellante. “Consider that VMware is valued at $70 billion and Dell owns 80 percent of the company — an ownership stake which is worth $56 billion. Yet Dell’s market value is $40 billion.”

That, he said, implies that the core Dell is worth negative $16 billion. “So this is a cheap way to own VMware, a company that’s undervalued, or a company that has some real work ahead. I think all three actually.”

Paying down debt will take some time, he added. “In the meantime Dell isn’t in a position to do aggressive M&A or stock buybacks,” he said. “But if the market stays strong, I think they’ll be just fine.”

Dell’s core Infrastructure Solutions Group, which includes products sold into data centers, saw revenue rise by 10 percent, to $9.9 billion, led by a 14 percent increase in servers and networking revenue. Storage showed slower growth, about 7 percent, despite recent gains in market share. But operating income rose 21 percent.

Personal computers didn’t fare as well, with revenue up only 4 percent overall and operating income down 1 percent. Commercial PC sales accounted for all the upside, rising 9 percent, while consumer PC revenues fell 4 percent.

Revenue from VMware jumped 17 percent, to $2.6 billion, though operating income rose only 4 percent, to $872 million. Still, that was enough to beat forecasts, and shares were rising 3 percent in extended trading. “VMware is obviously the gem,” said Vellante. “Its 33 percent operating income compares to 11 percent for Dell’s infrastructure group and 4 to 5 percent for the PC business.”

Dell also owns smaller stakes in Pivotal Software Inc. and SecureWorks Inc., and also owns RSA Security LLC, cloud management firm Virtustream and cloud services integration platform Boomi. Fourth-quarter revenue from these other businesses rose 5 percent in the quarter, to $593 million. For the year, they saw revenue rise 6 percent, to $2.3 billion.

Support our mission to keep content open and free by engaging with theCUBE community. Join theCUBE’s Alumni Trust Network, where technology leaders connect, share intelligence and create opportunities.

Founded by tech visionaries John Furrier and Dave Vellante, SiliconANGLE Media has built a dynamic ecosystem of industry-leading digital media brands that reach 15+ million elite tech professionals. Our new proprietary theCUBE AI Video Cloud is breaking ground in audience interaction, leveraging theCUBEai.com neural network to help technology companies make data-driven decisions and stay at the forefront of industry conversations.