CLOUD

CLOUD

CLOUD

CLOUD

CLOUD

Tech earnings reports from key enterprise software and infrastructure players this week underscore that information technology spending remains robust in the post-isolation economy.

That’s especially true for those companies that have figured out a coherent and compelling cloud strategy. Despite COVID variant uncertainties and hardware component shortages, most leading tech names outperformed expectations. That said, investors weren’t in the mood to reward all stocks and any variability in product mix, earnings outlook or bookings and billings nuances were met with a tepid response from the Street.

In this Breaking Analysis we’ll provide our commentary and new data points on key technology companies, including Snowflake Inc., Salesforce.com Inc., Workday Inc., Splunk Inc., Elastic NV, Palo Alto Networks Inc., VMware Inc., Dell Technologies Inc., Pure Storage Inc., HP Inc. and NetApp Inc.

Let’s start by rolling back a week or so and look at how stocks that are priced to perfection get affected by any negative news in this market.

On Aug. 20, we saw this headline hit:

The analyst report was put out by boutique firm Cleveland Research. The stock took a double-digit hit, as you can see in the chart above.

This author immediately got several texts from investors who know we follow the company asking what to do. Disclaimer: We don’t give stock picking advice, please do your own research.

But between theCUBE, Wikibon and Enterprise Technology Research, we see lots of data. And we’re happy to share that, which prompted this tweet:

Merv Adrian was tagged in the post. He’s a sharp data analyst from Gartner who responded: “I don’t speculate about revenues. No discernible shift in our client conversations, though. Interest still seems high.”

Looking deeper into the ETR data, correlating with market data and assessing statements by Snowflake last year gave us more confidence that Snowflake was not losing momentum.

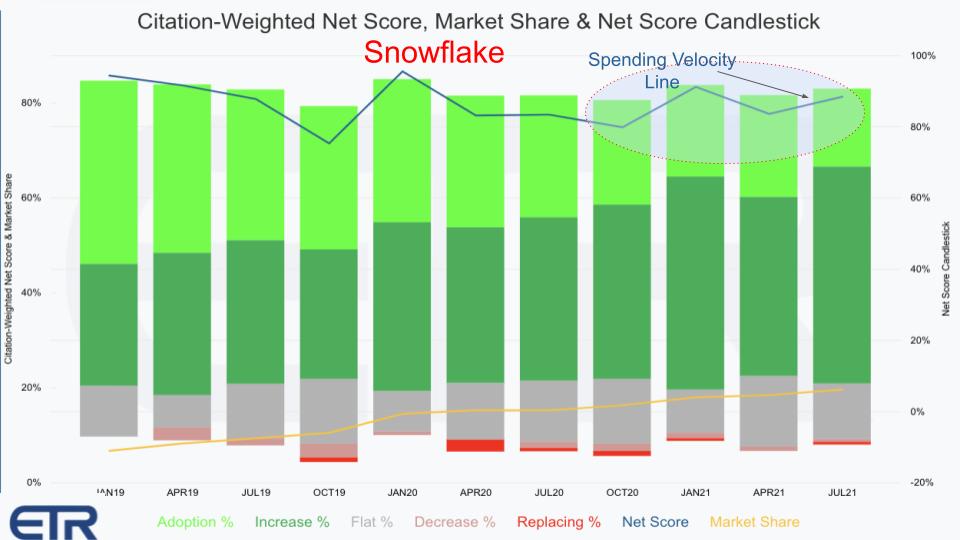

Above is a larger and more detailed version of the chart in the tweet. It’s a candlestick that shows a time series of the spending data on Snowflake using ETR’s Net Score methodology. The lime green stacked bars represent the percentage of customers in the survey that are newly adding the Snowflake platform. The forest green indicates the number of customers reporting that their spending is increasing by 6% or more. The gray is flat spend – plus or minus 5%. The pinkish stack is decreasing spend by 6% or more and the bright red is leaving the platform.

Subtracting the reds from the greens yields a Net Score, which for Snowflake in the July survey was a very elevated 81.3%.

We’ve highlighted the blue spending velocity line – that’s Net Score at the top. Put a picture of that blue line for Snowflake in your mind because we’re going to come back to it. The yellow line down below is Market Share, which is a measure of the pervasiveness in the survey – “mention share,” if you will.

Looking at the chart above, one might conclude that the lime green, that is new account acquisition, is compressing, which was the premise of Cleveland’s research. However in further analyzing the data, back in January 2019, Snowflake’s presence in the survey was much lower, only 35 accounts. In subsequent quarters that number has jumped to between 120 and 140 Snowflake accounts. So it’s a much higher N, and although the percentage mix of respondents adding new may be shrinking relative to the other categories, the absolute number of new accounts is growing.

Now on the earnings call, Snowflake said net new customers increased this past quarter to 458 up from 397 in the same period last year. So there’s continued new account growth, although the rate of growth may be decelerating.

But what’s telling is the forest green. On its very first earnings call as a public company, Snowflake Chief Financial Officer Mike Scarpelli said very clearly, the company’s revenue growth in the near term will come from existing customers. And the forest green – that is, existing customers spending more – is expanding in the ETR survey.

Analyzing this data combined with market information gives strong confirmation of the fundamental picture that Scarpelli painted.

Note the red in the chart above is virtually nonexistent. As such, it was no surprise that Snowflake handily beat its earnings on Aug. 25, which prompted a flurry of texts saying, “You were right, thanks.”

Don’t thank us. Do your own research. We’re just one data source.

The chart below is our popular XY view with Net Score or spending momentum on the vertical axis and Market Share or pervasiveness in the survey on the horizontal plane.

We talked about Snowflake already – but we’ll emphasize they’ve held that roughly 80% Net Score for 10-plus quarterly surveys now. And they’ve continued to move steadily to the right and expanded market presence.

Let’s make some comments on these other names and then dig in a bit more. Salesforce is the big player among these companies and as we’ve said in previous Breaking Analysis segments that it has become the next great software company, showing 20%-plus growth for five consecutive quarters, which is quite impressive.

Splunk, as we’re reported, has struggled in the survey, but you can see it has a great presence in the data set on the X axis. Splunk has an awesome customer base and the acquisition of SignalFx, plotted on the left with an elevated Net Score, represents a really good opportunity to enter new markets such as observability. And it helps accelerate Splunk’s move toward a subscription model. Splunk is embedding SignalFx into its go-to-market and product strategy efforts and using its deep customer relationships to transform the company for the digital era.

We also show Workday and we’re plotting the company’s core HCM business as well as its emerging Financials software suite. The latter represents Workday’s total available market expansion opportunity and the company appears to be back on track to show sustained growth.

Workday had a strong quarter, with improved remaining performance obligations or RPO of more than $10 billion, and it guided to the upside. It’s also impressively increasing operating cash flow forecasts to $1.5 billion for its current fiscal year. Subscription revenue topped $1 billion and we’d like to see Workday to get its subscription revenue growth back up over the magic 20% mark for a number of quarters and potentially years ahead. That would give the company a strong ongoing story in our view.

Elastic is also shown on the chart and has carved out a strong presence in the market with significant spending momentum, as shown by its position on the Y axis. Elastic has popularized the ELK stack, which comprises open-source tools Elasticsearch, Logstash and Kibana. The company is proving to be a cost-effective alternative to Splunk but is often cited by customers as requiring more expertise to leverage. As well, it’s smartly making moves by acquiring its way into the cybersecurity market.

Nonetheless, the company is executing well and is on its way to $1 billion in revenue and has achieved a $14 billion-plus market capitalization. More on Elastic in a moment.

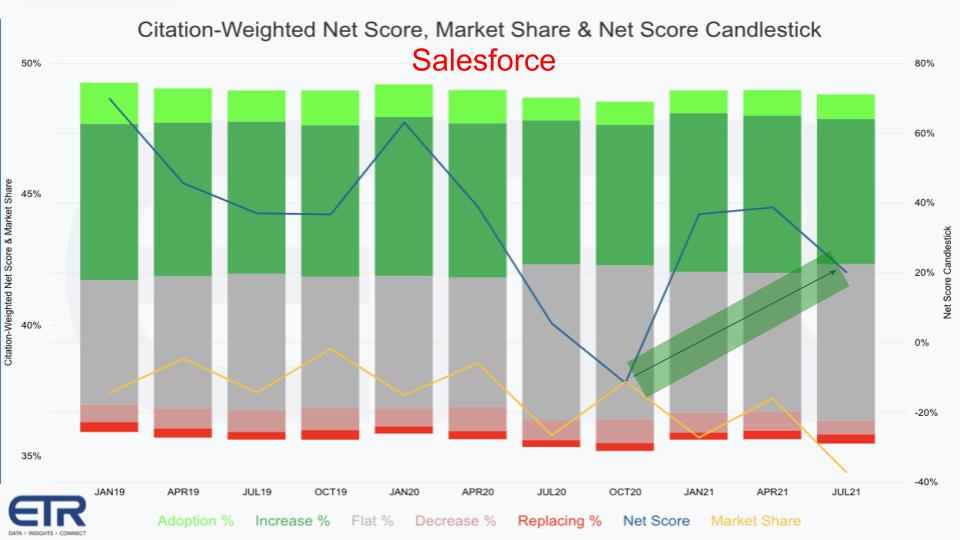

Below is the ETR spending profile for Salesforce.

Salesforce, as we showed earlier, has a huge and growing presence in the market and a consistently elevated Net Score in the ETR data set. And although the chart shows much more green than red and a strong uptick in spending momentum from last October’s survey, this doesn’t really tell the whole story.

Salesforce’s stock price rocketed out of the March 2020 crash and ran up to a peak last August and is on its way back. Salesforce has made a number of massive strategic acquisitions, including Tableau (about $15 billion), Slack ($28 billion), MuleSoft ($6 billion) and several other billion-dollar-plus buys, as well as a number of smaller acquisitions.

This past quarter saw 23% revenue growth with very solid 20% plus operating margins. Salesforce’s acquisition strategy is beginning to demonstrate the company’s promised operating leverage and Slack in our view will only add to that benefit, including continuous improvement in free cash flow. Salesforce revenue will blow through $25 billion this fiscal year. Salesforce is a company with a $250 billion market cap and appears to have meaningful upside momentum.

We believe Salesforce has earned its place as the next great software company, despite criticisms that its multiple parts cause difficult integrations and complexity. Although its revenues are smaller than Microsoft Corp., Oracle Corp. and SAP SE, it has momentum, it’s led by a dynamic founder and its execution can’t be denied.

One factor to watch is much of its growth is coming through acquisitions. This past quarter, for example, showed Slack’s contribution to RPO was higher than expected and so that somewhat lessens the enthusiasm for the company’s performance in other areas. But this can be looked at as a positive as well because the company is expanding its TAM. The larger portfolio gives it more operating leverage and hedges from market fluctuations.

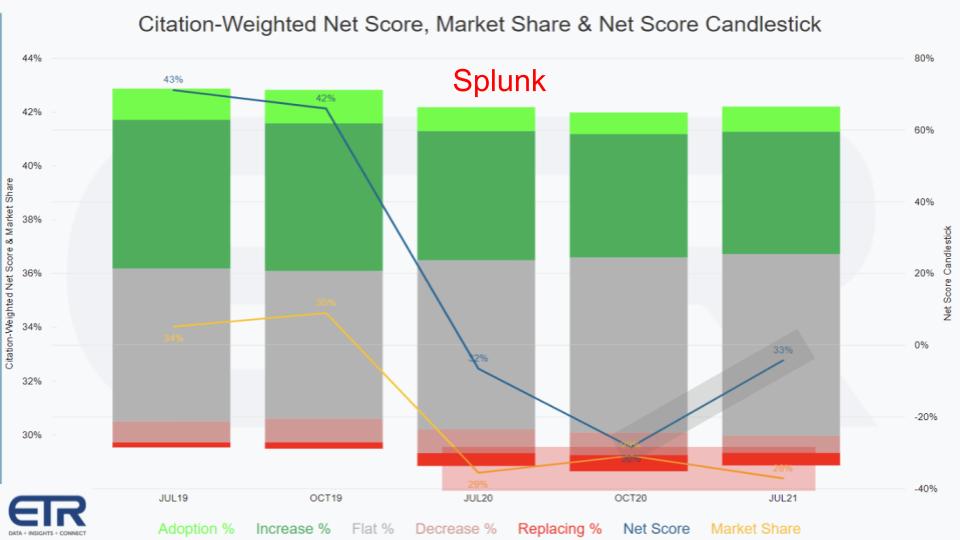

Below we show the same ETR candlestick for Splunk.

We’re finally seeing an uptick in Splunk’s spending momentum within the ETR data set. We’ve gone into depth with ETR’s Erik Bradley on this topic in previous Breaking Analysis segments.

The key point is we see Splunk has been transitioning from a traditional perpetual license to an annual recurring revenue or ARR model. It is finally showing signs that there’s light at the end of that tunnel. Investors don’t like companies in transition and, like Salesforce, Splunk saw its stock price run up to an all-time high last August, then come down hard, and it has never fully recovered. But it has come off its May lows and there were some real positives this past quarter.

Specifically, cloud ARR grew 72% and bookings grew 29% year on year. The company was conservative in its guidance and there still seems to be some uncertainty around cash flow, but more clear guidance by Splunk on the top line is a welcome sign. However, it would be a stronger sign if Splunk could return to more predictable and steady cash flows, which appears to be still a few quarters down the road.

One last point. Splunk has brought in new management, specifically notable is Teresa Carlson as president and go-to-market leader. We see this as critical in completing the transition to a more predictable ARR model and leveraging the SignalFx acquisition.

Another name we’ve been following that announced earnings this week is Elastic.

As you can see by the ETR data above, the company has an elevated Net Score with very little red in the bars. Now note the blue line, which is Net Score (spending velocity). Although it’s slowly decelerating, it remains very strong. Remember the comment earlier about freezing that Snowflake blue line in your head? The reason we said that is because for Snowflake to hold its roughly 80% Net Score position firmly over 10-plus quarters is quite astounding and for the most part unprecedented in the ETR data.

Back to Elastic. The company grew its top line this past quarter by 45%, which was a healthy beat, and that helped operating margins come in above expectations. Elastic has become the open-source poster child for observability but customers often cite challenges related to complexity and scaling, with the need to seek professional services help if it doesn’t exist in-house, which sometimes creates headwinds for customers.

Overall, Elastic had a very strong report, especially in its cloud business, which grew 89% relative to last year. Billings were somewhat light based on consensus, but the company noted some deals were pulled forward last year. The company guided above expectations but not enough to get investors excited and the stock has modestly declined since its earnings came out.

To our point at the opening of this post, anything other than a meaningful beat and raise is viewed negatively by investors, which may present opportunities for companies that you believe have a solid future.

Circling back to enterprise software broadly, there seems to be no end in sight to the shift to cloud-based offerings, both software-as-a-service and Snowflake-like consumption models, in which we are big believers. Digital transformation initiatives are real and meaningful and software spending, we believe, is going to be robust for quite some time.

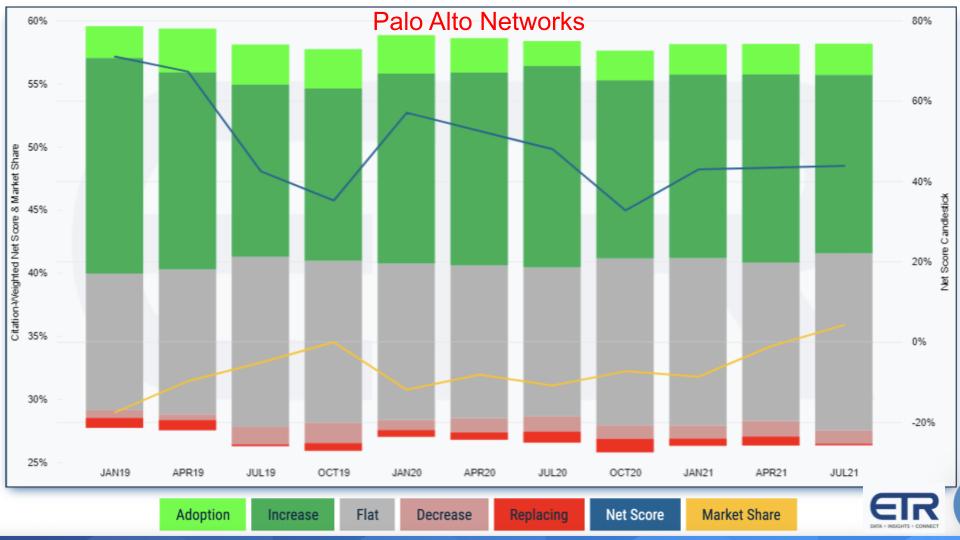

Let’s take a look at infrastructure, starting with Palo Alto Networks, and then take a broader look at some other more traditional hardware and software infrastructure players.

In February 2020, we reported the valuation divergence between Palo Alto Networks and Fortinet Inc. and cited challenges around the former’s shift to cloud as a headwind– especially its go-to-market problems. But at the same time, we said we were confident that Palo Alto would work through these issues and the chief information security officers from ETR panels and other anecdotal information from theCUBE community suggested the company would power through these challenges.

Well, it has. As shown in the ETR data above, Palo Alto has a huge presence in the market (yellow line) and consistently elevated Net Scores (blue line). Palo Alto’s stock is trading near its all-time high and it reacted well to its earnings report this past week, which showed revenue grew nicely at 28% year-on-year.

The company has consistently impressed, despite some hiccups of the past, and appears to be well-positioned for the emerging hybrid work economy.

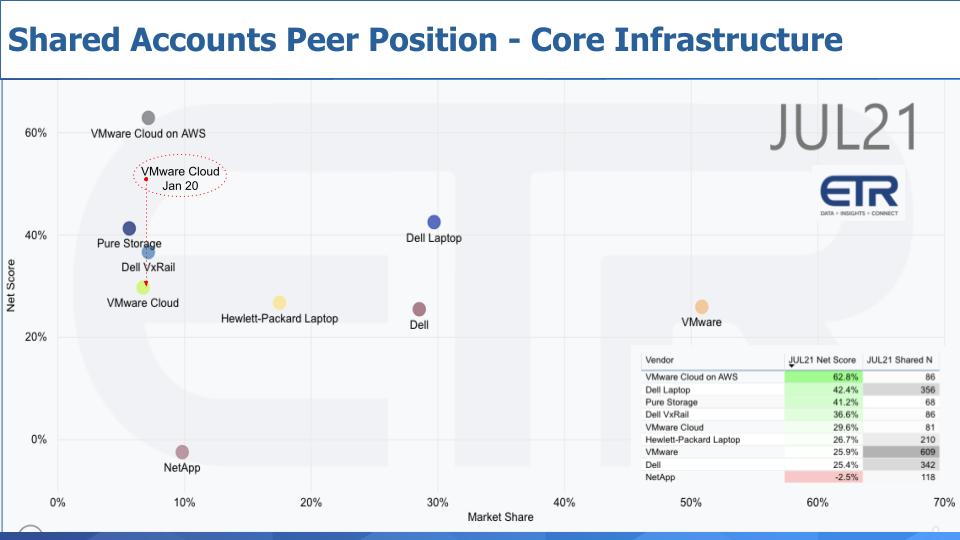

Let’s take a look at some of the key infrastructure players that announced this past week.

The chart above shows our XY view with Net Score or spending momentum on the vertical axis and Market Share or pervasiveness in the survey data on the horizontal axis. The table insert shows the raw data that determines the position of the dot.

VMware has the largest presence in the ETR data set among these players. VMware’s revenue grew 9% in the quarter, in line with estimates. The company had a solid quarter but only marginally beat. The stock got hit hard and fell almost 7% Friday.

VMware cited stronger-than-expected perpetual license sales and somewhat soft SaaS/subscription revenue. It’s not surprising that we’re going to see some lumpiness as the company transitions to a subscription model, but the Street didn’t like it.

VMware Cloud on AWS grew 80% and that’s confirmed in the data above. Compute was also strong. One concern in the ETR data is the VMware cloud (that is, VMware’s on-prem cloud tools such as VCF), which you can see above is well off its January Net Score highs.

Definitions of cloud for on-premises vendors and hybrids are fluid and it’s possible that this is a survey nuance. But generally we’ve discerned more spending momentum in VMware’s AWS offering than its on-prem cloud. So we’ll continue to watch that trend.

Overall, VMware’s business model remains solid and that’s seen in the numbers. A key milestone to watch is the VMware spin, which will happen in the November timeframe, assuming all goes according to plan. Once again, Dell will make a large cash withdrawal from the VMware ATM in order to complete the transaction. This event will mark a new era in VMware governance, creating a truly untethered independent VMware, which became part of EMC in 2004 and then Dell in 2015.

The two companies, Dell and VMware, will now be fully separated from an ownership perspective, but both companies will have the same chairman in Michael Dell. So while the governance structure will be untethered, we suspect the chairman will ensure alignment.

Practically, what this means is VMware will sell a ton of licenses through Dell, its largest channel, and Dell will continue to have a special relationship with VMware.

Dell had a great quarter. It grew top-line revenue by 15% year-on-year. Its client business grew 27%, and you can see above the elevated Dell Laptop Net Scores. ISG (the data center business) was up 3%, comprising Servers & Networking, up 6%, and storage, off 1%. Management reported that its midrange storage orders (not revenue) were up 17%. The challenge in storage is that the high end is cyclical and much of the midrange is eating away at the high-end business and continues to be a drag on revenue.

Said another way, high-end storage is a business in managed decline. It’s still large enough so that midrange growth cannot offset the declines at the high end. But it’s getting close.

We saw Dell’s earnings and were surprised to see the stock down 4.5% Friday. We think there are a couple of things at play here. The biggest factor is Dell’s stock price got dragged down with VMware. In a way, with VMware value comprising so much of Dell’s market cap, being down only 4% while VMware was down 8% implies that the core Dell business is viewed positively by the Street. We thought with the VMware spin coming later this year, investors might gravitate more aggressively toward Dell, but that didn’t happen.

The other factor could be HP, which we show above at a lower Net Score than Dell’s laptop business. HP cited supply chain issues and component shortages. Dell cited the same and maybe is off on sympathy. It’s clear that Dell is doing a much better job than HP with regard to managing component shortages. The frustrating thing for these companies is it might be a $50 part holding up a server or a laptop. But demand is good which is a positive.

There’s another possible ironic factor that might help Dell manage supply. This is just a theory, but there may be some merit to it. Dell is historically not known for being first with bleeding-edge technology. Dell competes on value, the industry’s broadest portfolio, great service and go-to-market excellence. As such, it tends to use more mature technologies longer than other competitors that have to be more bleeding-edge in order to compete.

Perhaps the portions of Dell’s portfolio that leverage older technologies are more widely available and allow Dell to generate revenue where others have retired more mature parts of their portfolio. Customers with pent-up demand are happy to take whatever solves their immediate problem.

You see NetApp on the chart above and it’s not a flattering picture. The company has not performed well in the ETR surveys for several quarters and has a negative Net Score. This is because of a low new adoption figure and a fat middle of flat spend… and a pretty high churn in the data set.

NetApp is another company that has been in transition. The company beat on top-line revenue and earnings this past quarter. It claims to have picked up 1,500 new customers in its cloud business. So maybe the ETR survey is not picking that up, or perhaps it’s existing NetApp customers that are moving to the cloud service and NetApp is counting them as new.

Regardless, the Street likes NetApp’s story. The stock has been acting well this year, outpacing the S&P 500. NetApp reported that its public cloud business grew revenue 155% in the quarter and that will become a key metric going forward as NetApp is re-factoring its business for cloud.

The question for NetApp is: Once it proves its business is back on track, what’s next? Will it remain a focused company in data storage or will it do what EMC did years ago and expand into adjacencies to grow its TAM?

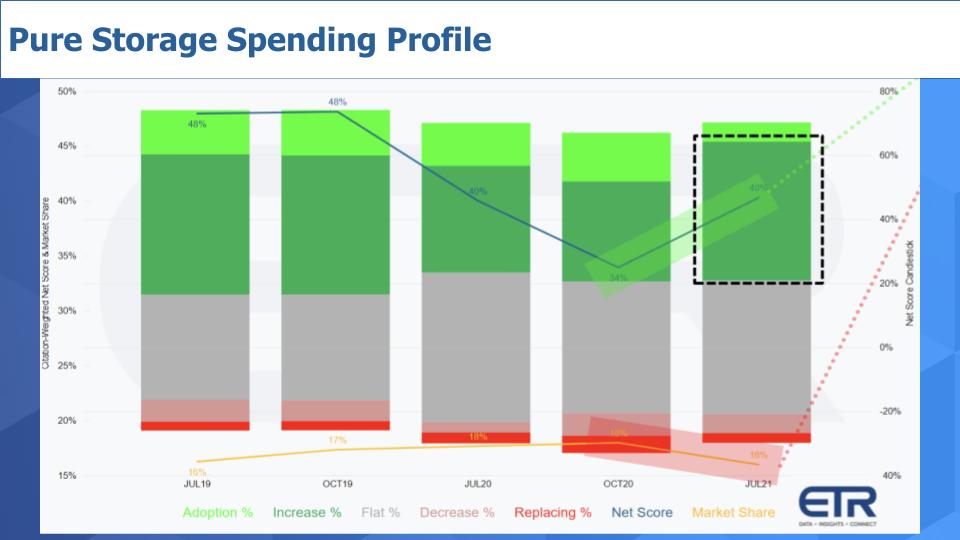

You see Pure on the chart above with a nicely elevated Net Score. The company also beat top and bottom lines this quarter and CEO Charlie Giancarlo promised roughly 20% revenue growth going forward.

The Street sure liked that story and the stock shot up nearly 20% on the news.

Above we show the ETR spending data and it’s trending in the right direction for Pure, supporting its recent quarterly report. Pure’s messaging is all around a modern data platform, and it’s clear from customer conversations that Pure’s storage products are easier to use than traditional storage offerings. And it has a leg up on as-a-service models, which Pure has been pursuing for years, while others are more recently bringing that to market.

Pure is still much smaller than the Dells and NetApps of the storage world, but if it can continue on a strong growth trajectory, it will become a larger company. The question will be how to continue to expand its TAM. The obvious path today is share gains, which over the years it has accomplished, but that won’t be as easy as it was last decade when Pure caught EMC in particular but also NetApp flat-footed without strong flash array strategies.

Pure’s Portworx acquisition is something to watch as it tries to transition the market to a true cloudlike programmable infrastructure model for storage and data.

One other thought: NetApp remains the lone large independent storage company today, with Pure becoming increasingly prominent. But Pure will have to triple its revenue to begin to approach NetApp’s size. Can it get there organically? Will Pure have to expand its TAM by entering new markets (such as data protection and data management)? Our bet is for the time being Pure will try to demonstrate consistent 20%-plus annual growth and package that a strong multiyear story — then figure it out from there once that plays out.

We’ll leave you with this thought about the infrastructure space generally and storage specifically: While cloud storage has exploded over the past several years, on-prem storage has been extremely soft. This in our view has been the result of the double whammy combination of cloud stealing share from on-prem storage demand and the massive flash injection. The latter suppressed the need to buy more spinning spindles and controllers in order to get better performance, and this hurt demand.

But as we predicted last year, we believe that there’s pent-up demand as people go back to work and headquarters need refreshes. There’s only so much blood IT managers can squeeze from the stone of storage utilization while maintaining adequate performance. Storage is no longer monolithic, and there are emerging use cases, especially ones that are data-centric. And different storage types are emerging.

As Satya Nadella said recently, we’ve reached peak centralization and as such that will create tailwinds for storage offerings that can accommodate cloud and on-prem (that is, the new hybrid). IT pros understand that moving data is expensive and risky. They understand it’s best to keep data where it belongs for reasons of performance and compliance.

So it looks like there’s a decent chance that the long on-prem storage winter is over and the market could return to solid growth, even in the face of a continued cloud explosion. This is important in our view because although compute is the revenue king, most of the margin in compute goes to Intel Corp. and Advanced Micro Devices Inc. Storage is a 60%-plus gross margin business and fundamentally more profitable than compute – at least for legacy vendors with high on-prem exposure.

Cloud economics for compute, of course, are different, as Amazon Web Services Inc. has demonstrated. So data storage remains a strategic business, especially for those firms that don’t own a public cloud.

Remember we publish each week on Wikibon and SiliconANGLE. These episodes are all available as podcasts wherever you listen.

Email david.vellante@siliconangle.com, DM @dvellante on Twitter and comment on our LinkedIn posts.

Also, check out this ETR Tutorial we created, which explains the spending methodology in more detail. Note: ETR is a separate company from Wikibon and SiliconANGLE. If you would like to cite or republish any of the company’s data, or inquire about its services, please contact ETR at legal@etr.ai.

Here’s the full video analysis:

Support our mission to keep content open and free by engaging with theCUBE community. Join theCUBE’s Alumni Trust Network, where technology leaders connect, share intelligence and create opportunities.

Founded by tech visionaries John Furrier and Dave Vellante, SiliconANGLE Media has built a dynamic ecosystem of industry-leading digital media brands that reach 15+ million elite tech professionals. Our new proprietary theCUBE AI Video Cloud is breaking ground in audience interaction, leveraging theCUBEai.com neural network to help technology companies make data-driven decisions and stay at the forefront of industry conversations.