BIG DATA

BIG DATA

BIG DATA

BIG DATA

BIG DATA

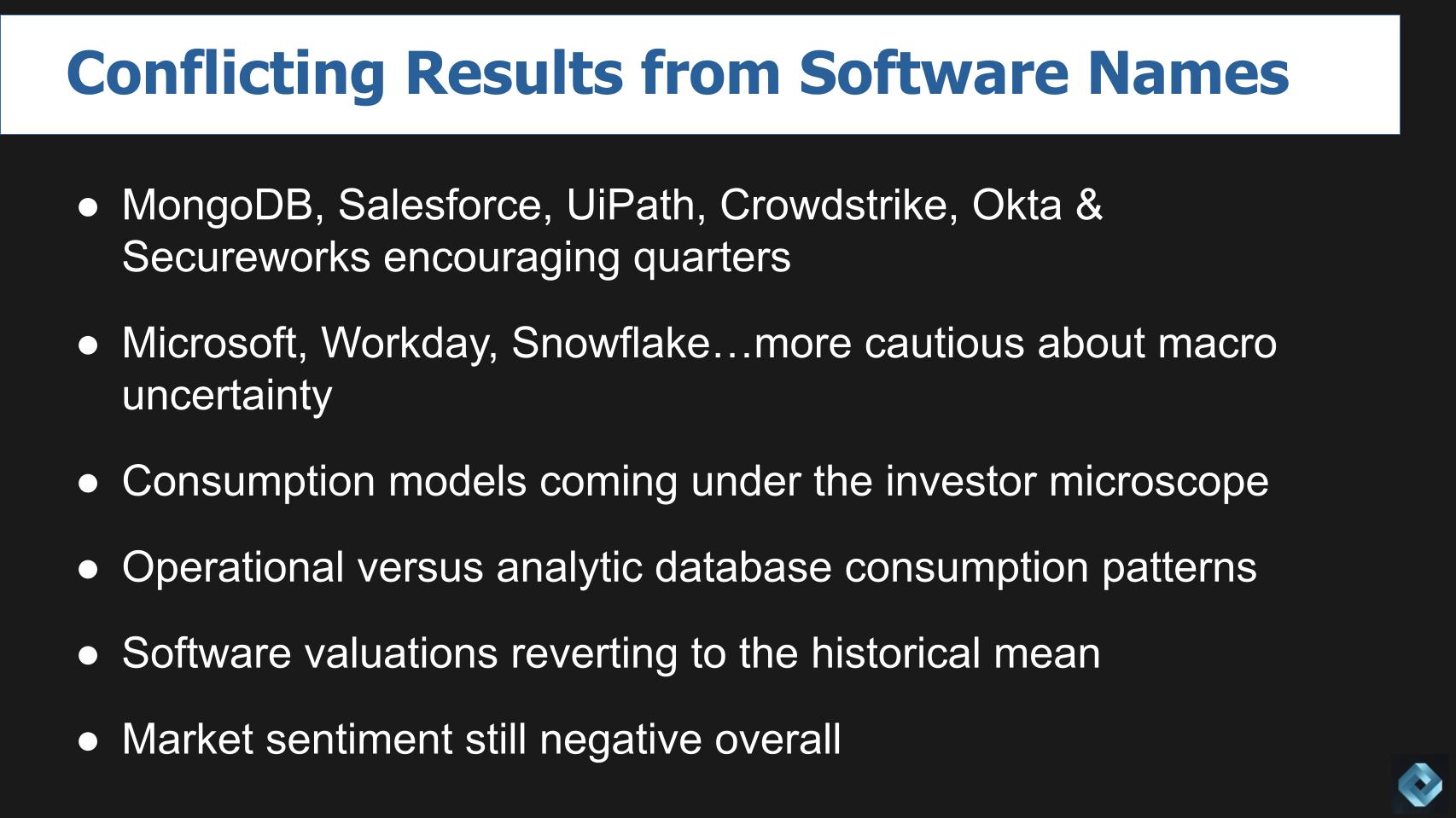

Earnings season has shown a conflicting mix of signals for software companies. Most firms are expressing caution over macro headwinds citing a combination of Ukraine, inflation, interest rates, overseas softness, currency, supply chain and general demand for technology.

But MongoDB Inc., along with a few other names appeared more sanguine, thanks to a beat in the recent quarter and a cautious but upbeat outlook for the near term.

In this Breaking Analysis, ahead of MongoDB World 2022, we drill into the company’s business and what ETR survey data tells us in the context of overall demand and the patterns from other software companies. (* Disclosure below.)

We’re seeing some distinctly different results and guidance from major software companies in recent days.

We’ll dig deeper into MongoDB in this post. The company beat earnings per share by 30 cents and revenue by more than $18 million this past quarter. Salesforce Inc. had a great quarter and its diversified portfolio is paying off as seen by the stock’s noticeable uptick post earnings. UiPath Inc., which had been hammered prior to this quarter has brought in a co-chief executive and its business is showing a nice rebound with a three-cent EPS beat and a nearly $20 million top line beat. CrowdStrike Holdings Inc., Okta Inc. and Secureworks Inc. showed demand for security software remains strong.

Meanwhile, managements at Microsoft Corp., Workday Inc. and Snowflake Inc. expressed greater caution about the macroeconomic climate. Especially on investors’ minds is concerns about consumption pricing models. Snowflake, which had a small top-line beat, cited softness and negative effects from reduced consumption, especially from certain consumer-facing customers… which has analysts digging more deeply into the predictability of their models.

Barclays analyst Raimo Lenschow published an especially thoughtful piece on this topic, concluding that Mongo was less susceptible to consumption headwinds than, for example, Snowflake. That’s essentially for three reasons: 1) Atlas, Mongo’s cloud managed service, comprises only about 60% of Mongo’s revenue; 2) A premise that Mongo is supporting core operational applications that can’t be easily dialed down; and 3) Snowflake customers are more concentrated and because of the fact that a preponderance of its revenue is consumption-driven, it will be more sensitive to swings in consumption patterns.

Our view is that consumption pricing models are here to stay and the much-preferred model by customers. The appeal of consumption is you can actually dial down spend if needed. And that’s what happened with certain Snowflake customers this quarter, adding credibility to the model. In fact, many business cases include this dynamic as a benefit of moving to a platform with consumption-based pricing. Admittedly, procurement often wants to put caps and limits on the spend or negotiate volume discounts.

But to the point about Mongo supporting core applications versus Snowflake workloads being more discretionary: We believe that over time you will see the increased emergence of data products and services that will become core monetization drivers for organizations. We’re already seeing that today, in fact, in data markets for example, where data is the product. Snowflake, along with other data platforms, feeds these data products and will become increasingly less susceptible to the sensitivities we heard about on the Snowflake earnings call and are being discussed in the community.

The last two points in the slide above speak to valuations and market sentiment. Software valuations have reverted to their historical mean, which is a good thing in our view – we’ve taken some of the air out of the bubble and a return to more normalized valuations is a welcome buying opportunity for many investors. And we’re still in a lousy market for stocks, which, together with lower valuations, could mean a bottom is forming. The market tends to be at least six months ahead of the economy and often, not always, a good predictor of what’s ahead. We’ve had some tough compares to the boom in tech during the pandemic and we’ll be watching next quarter closely because the macro headwinds have now been firmly inserted into the guidance assumptions of software companies — meaning if demand picks up and companies rebound next quarter, the market could improve.

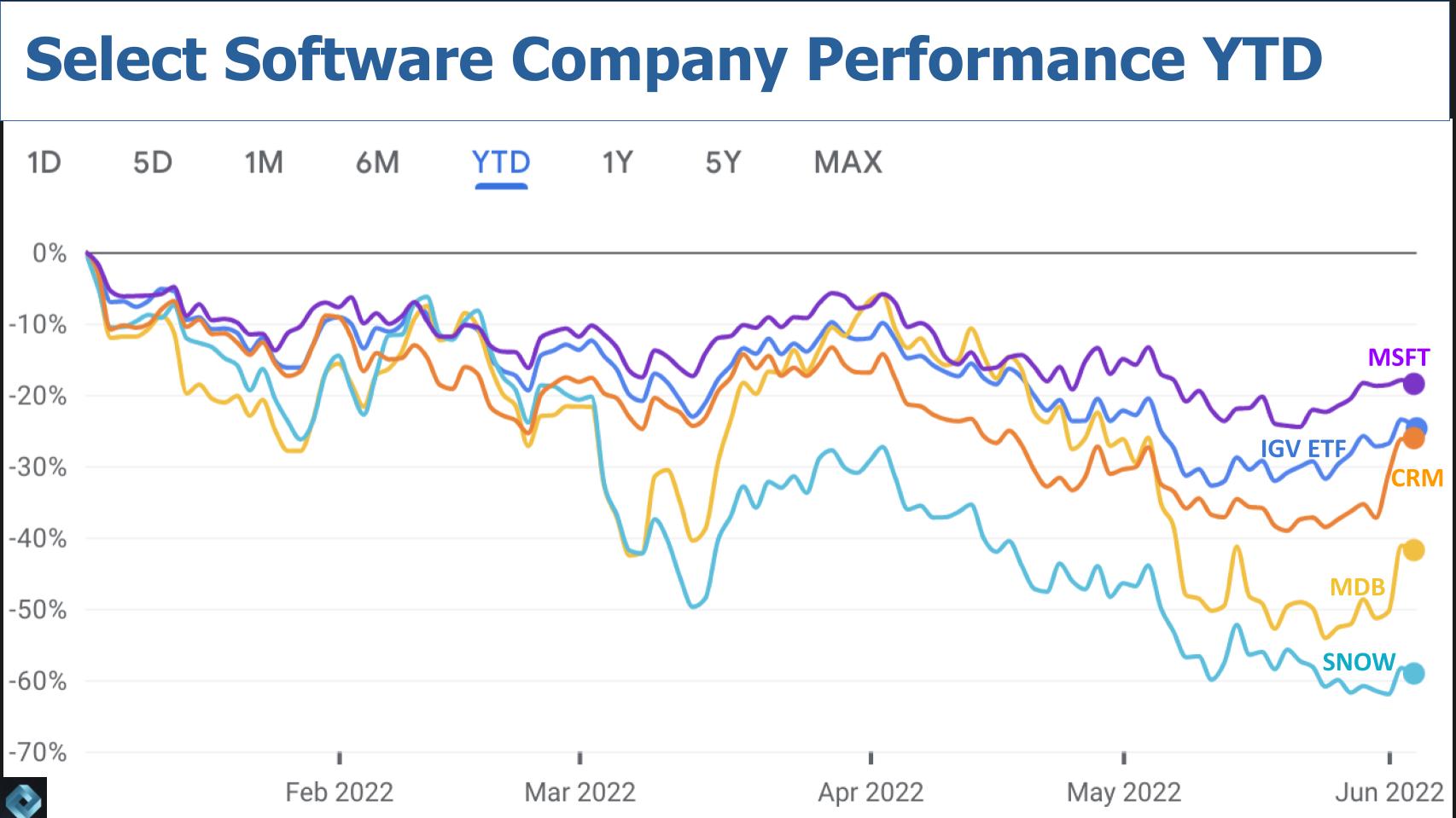

Let’s have a look at how two proxies for high-flying names, MongoDB and Snowflake, have fared relative to the broader software market and some larger, more profitable software companies.

The chart above shows year-to-data data comparing the performance of Microsoft, Salesforce, MongoDB and Snowflake to the IGV Software-heavy ETF (the darker blue line). The ETF doesn’t own Snowflake or Mongo, by the way. You can see the super-caps, Microsoft and Salesforce, have fared pretty well relative to the benchmark, whereas Mongo and especially Snowflake – i.e. the higher-growth companies — have been much more impacted.

We don’t show Oracle Corp. in the chart, but it’s another example of a profitable, large-cap stock that has outperformed the software benchmark we’ve used. In fact, Oracle for most of the year has outperformed even Microsoft.

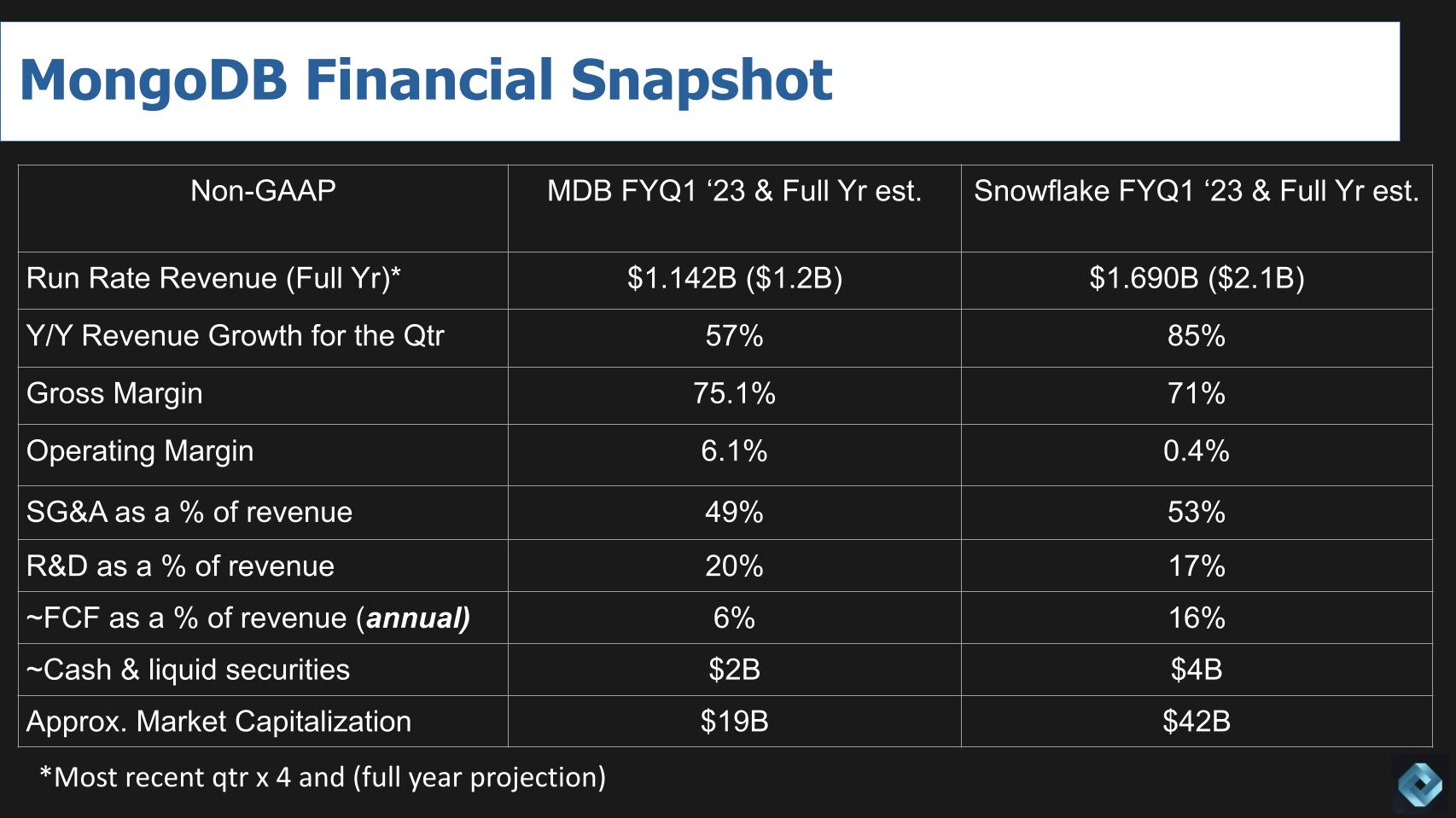

What we’ve done above is take the most recent quarter’s revenue and multiplied it by four times to get a revenue run rate — and parenthetically added a projection for full-year revenue. Mongo will do north of a billion dollars in revenue, while Snowflake will surpass $2 billion in FY 2023. Snowflake is on its way to $3 billion in FY 2024 revenue. Its billings will likely hit $2.7 billion in FY 2023. MongoDB, on the other hand, will likely land in the $1.5 billion to $1.6 billion range in FY 2024. You can see Snowflake is growing faster at 85% this past quarter and is projected to grow faster than MongoDB into FY 2024.

We took most of these profitability ratios from the current quarter except for free cash flow. Both companies have high gross margins, but as we’ve discussed, not as high as some traditional software companies, in part because of their cloud COGS but also their maturity. Both Mongo and Snowflake, because they are in growth mode, have thin operating margins. They spend about half their revenue on growth – that’s the SG&A line, mostly the S category. They are companies with a specialized focus so they spend a fair amount of their revenue on R&D… maybe not as high as you might think but a hefty percentage.

We calculated the free cash flow as a percentage of revenue line from the full-year projections, and you can see Snowflake’s free cash flow will settle in at around 16% this year versus Mongo’s 6%. Rounding up, Snowflake has about $4 billion in cash and marketable securities on its balance sheet, with little to no debt, whereas Mongo has about $2 billion with some longer-term debt.

And you can see Snowflake’s market capitalization is about double that of Mongo’s, so you’re paying for higher growth, the Frank Slootman/Mike Scarpelli execution expectation, a stronger balance sheet and quite a bit more hype. But Snowflake’s market cap is well off its roughly $100 billion valuation that it touched during the pandemic.

As an aside, Mongo has around 33,000 customers – about five times the number of customers Snowflake has. So it’s a bit of a different customer mix and concentration. Both companies have no lack of market in our view.

Let’s dig a little deeper into Mongo’s business and bring in some Enterprise Technology Research survey data.

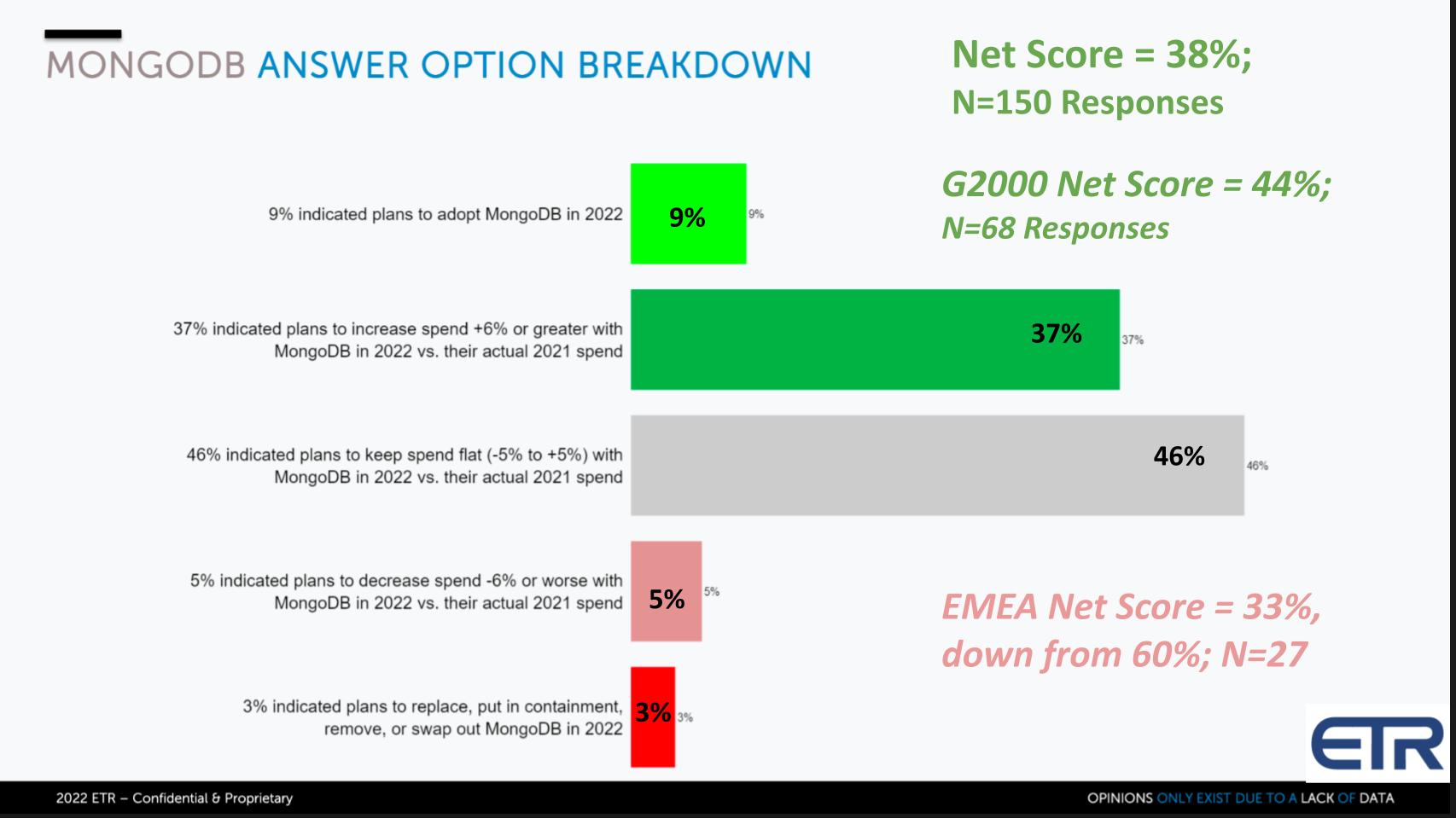

The colorful chart above shows the breakdown of Mongo’s Net Score. Net Score is ETR’s proprietary methodology that measures the percent of customers in their quarterly survey that are adding the platform new – that’s the lime green at 9%. Existing customers spending 6% or more on the platform – that’s the forest green at 37%. Flat spend – the gray at 46%. Decreasing spending by 6% or more – the pinkish at 5%. And churning, that’s the red at 3%. Subtract the reds from the greens and you net out to 38%: a very solid spending picture for Mongo.

Note that this survey of 1,200-plus organizations includes 150 MongoDB customers. It includes 68 Global 2000 MongoDB customers and those larger firms are showing a spending velocity of 44% – so it’s notably higher among larger clients. And while it’s a smaller sample of only 27, EMEA’s Net Score for Mongo is 33%, down from 60% last quarter. Mongo cited softness in its European business, so that aligns with the ETR survey data.

In the chart below, we plot Mongo relative to some other data platforms. These don’t all necessarily compete head-to-head with MongoDB, but they reflect data and database platforms that can serve a variety of workloads.

The chart depicts an XY graph with Net Score or spending momentum on the vertical axis and Overlap or presence in the dataset on the horizontal axis. The red dotted line at 40% indicates an elevated level of spending. We’ve highlighted Mongo, which is very close to that line and has a strong presence on the X axis — right there with Google Cloud Platform. Snowflake, as we’ve reported several weeks ago, has come down to earth, again aligning ETR data with the earnings results. But Snowflake remains well elevated relative to its peers. Amazon Web Services Inc. and Microsoft have many data platforms that are captured in this data, so their plot positions reflect broad data platform portfolios, massive estates and their large presence in the market.

And you see the pack of others, including Cockroach Labs Inc. – small but elevated — Couchbase Inc., creeping up since its IPO, Redis Ltd., MariaDB Corp., and some legacy platforms, including the leader in database, Oracle, along with IBM Corp. and Teradata Corp.’s cloud and on-premises platforms.

One interesting side note is that on Mongo’s earnings call, executives clearly cited the advantages of its increasingly all-in-one approach, relative to others that offer a portfolio of bespoke, “horses for courses” databases. Mongo cited the advantages of its simplicity and lower costs as it adds more and more functionality for developers. Oracle ironically often makes a similar argument, especially targeting AWS. MongoDB doesn’t call out AWS as does Oracle, but clearly Amazon is the poster child for lots of data platforms that are more focused on specific workloads, versus trying to put more function into a single database service to consolidate platforms.

And of course Mongo would differentiate from Oracle, making the argument that Oracle, as a traditional relational database, is more complex, less flexible and less appealing to developers. And Oracle would counter and that they now support a MongoDB API, so why go anywhere else? To us, this gives credence to the fact that if Oracle is trying to capture business by offering a Mongo API… Mongo must be doing well!

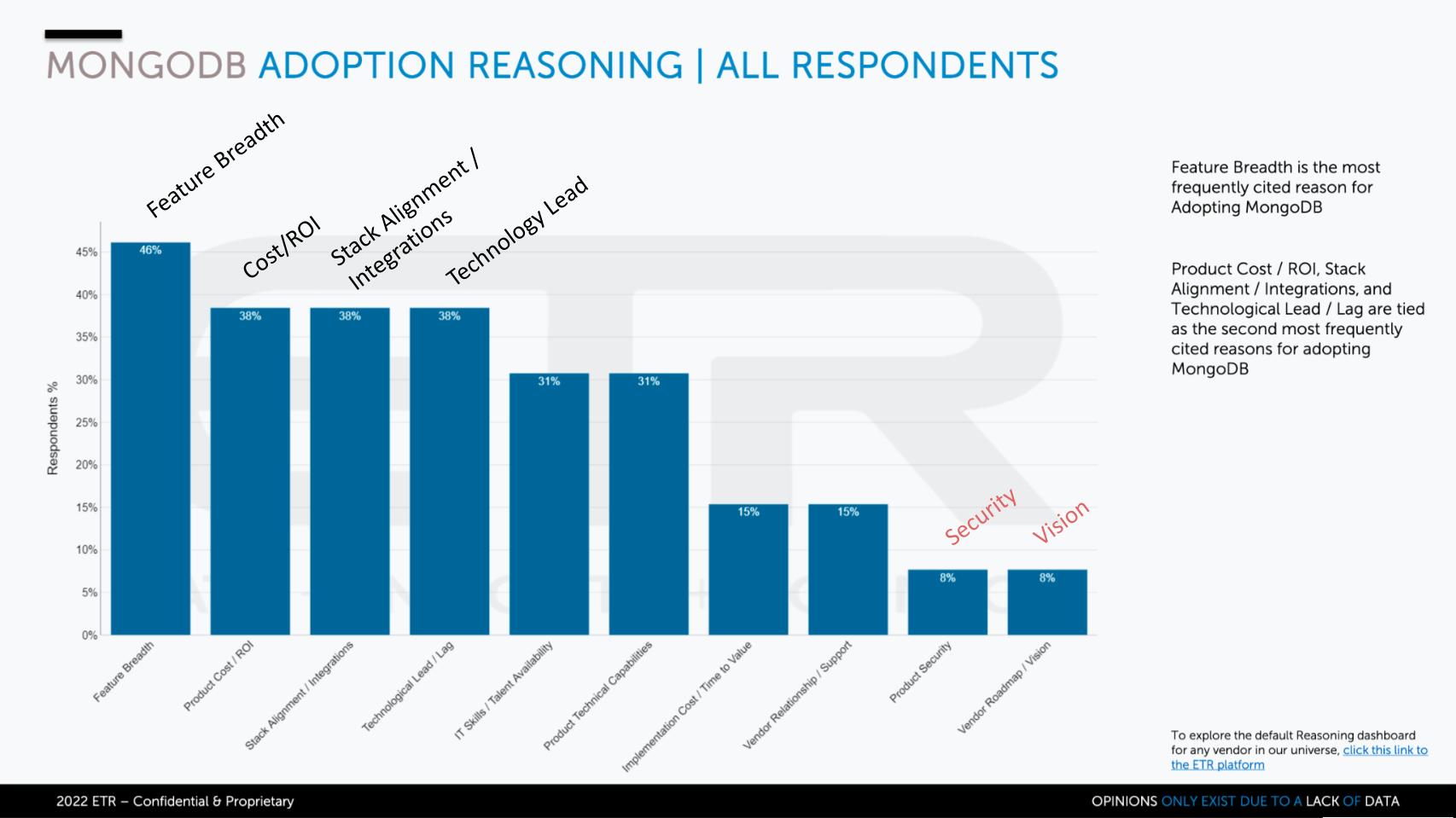

The data above is an ETR chart that addresses the reasons for adopting the platform. Mongo customers cite its feature breadth as the No. 1 reason, followed by lower costs/better ROI No. 2, integrations and stack alignment No. 3 and Mongo’s technology lead No. 4. Security and vision are much lower as shown on the right. This doesn’t necessarily mean Mongo has security issues, although it has been cited as a concern by customers.

Mongo is a document database. It has become a viable alternative to traditional relational databases, meaning you have much more flexibility over your schema. You can pretty much put anything into a document database. Developers seem to love it because it’s simple for them. Generally it’s fair to say Mongo’s architecture favors consistency over availability… it uses a single master architecture as a primary node. Customers will create secondary nodes in the event of a primary failure, but you have to think about that and consider recovery more carefully.

No fixed schema means it’s not a tables-and-rows structure and you can shove anything you want into the database, but you have to think about how to optimize performance. So there are nuances and tradeoffs as with any architecture, but Mongo’s approach is gaining traction in the market because simplicity with lots of functionality is a winning formula.

To that point, Mongo has been hard at work evolving the platform from its early days as a pure document database by adding things such as graph processing and time series, making search easier and more embedded into the platform. Atlas is a fully managed cloud database, which as we said earlier, now comprises 60% of Mongo’s revenue. The company has developed Kubernetes integrations and dozens and dozens of other features. Mongo has done a great job of creating a leading data platform today that is loved by customers and highly functional.

TheCUBE will be at MongoDB world next week and here are some of the things we’ll be watching:

Mongo will always have a main focus on developers, as the company prides itself on being a developer-friendly platform. Look for new features especially around security and governance and simplification of configurations and cluster management. Mongo will likely continue to advance it’s all-in-one appeal and add more capabilities that reduce the need to spin up bespoke platforms.

We would also expect enhancements to Atlas as that is the future of the company’s product portfolio. Expect more cloud-native features and integrations, perhaps simplified ways to migrate to Atlas and improved access to data sources. The focus will likely be on generally making the lives of developers and data analysts easier.

These are the main things we’ll be scoping out at the event. So please stop by if you’re in NYC at the show or tune into our coverage on theCUBE.net.

Thanks to Stephanie Chan, who researches topics for this Breaking Analysis. Alex Myerson is on production, the podcasts and media workflows. Special thanks to Kristen Martin and Cheryl Knight, who help us keep our community informed and get the word out, and to Rob Hof, our editor in chief at SiliconANGLE. And special thanks this week to Andrew Frick, Steven Conti, Anderson Hill, Sara Kinney and the entire Palo Alto team.

Remember we publish each week on Wikibon and SiliconANGLE. These episodes are all available as podcasts wherever you listen.

Email david.vellante@siliconangle.com | DM @dvellante on Twitter | Comment on our LinkedIn posts.

Also, check out this ETR Tutorial we created, which explains the spending methodology in more detail. Note: ETR is a separate company from Wikibon and SiliconANGLE. If you would like to cite or republish any of the company’s data, or inquire about its services, please contact ETR at legal@etr.ai.

Here’s the full video analysis:

All statements made regarding companies or securities are strictly beliefs, points of view and opinions held by SiliconANGLE media, Enterprise Technology Research, other guests on theCUBE and guest writers. Such statements are not recommendations by these individuals to buy, sell or hold any security. The content presented does not constitute investment advice and should not be used as the basis for any investment decision. You and only you are responsible for your investment decisions.

(* Disclosure: Many of the companies cited in Breaking Analysis are sponsors of theCUBE or clients of Wikibon. None of these firms nor other companies have editorial control over or advance viewing of what’s published in Breaking Analysis.)

Support our mission to keep content open and free by engaging with theCUBE community. Join theCUBE’s Alumni Trust Network, where technology leaders connect, share intelligence and create opportunities.

Founded by tech visionaries John Furrier and Dave Vellante, SiliconANGLE Media has built a dynamic ecosystem of industry-leading digital media brands that reach 15+ million elite tech professionals. Our new proprietary theCUBE AI Video Cloud is breaking ground in audience interaction, leveraging theCUBEai.com neural network to help technology companies make data-driven decisions and stay at the forefront of industry conversations.