INFRA

INFRA

INFRA

INFRA

INFRA

We’re getting used to the phrase “higher for longer,” referring to the realization that interest rates are expected to remain elevated for a period of time. This trend is having an inverse effect on enterprise tech spending growth rates.

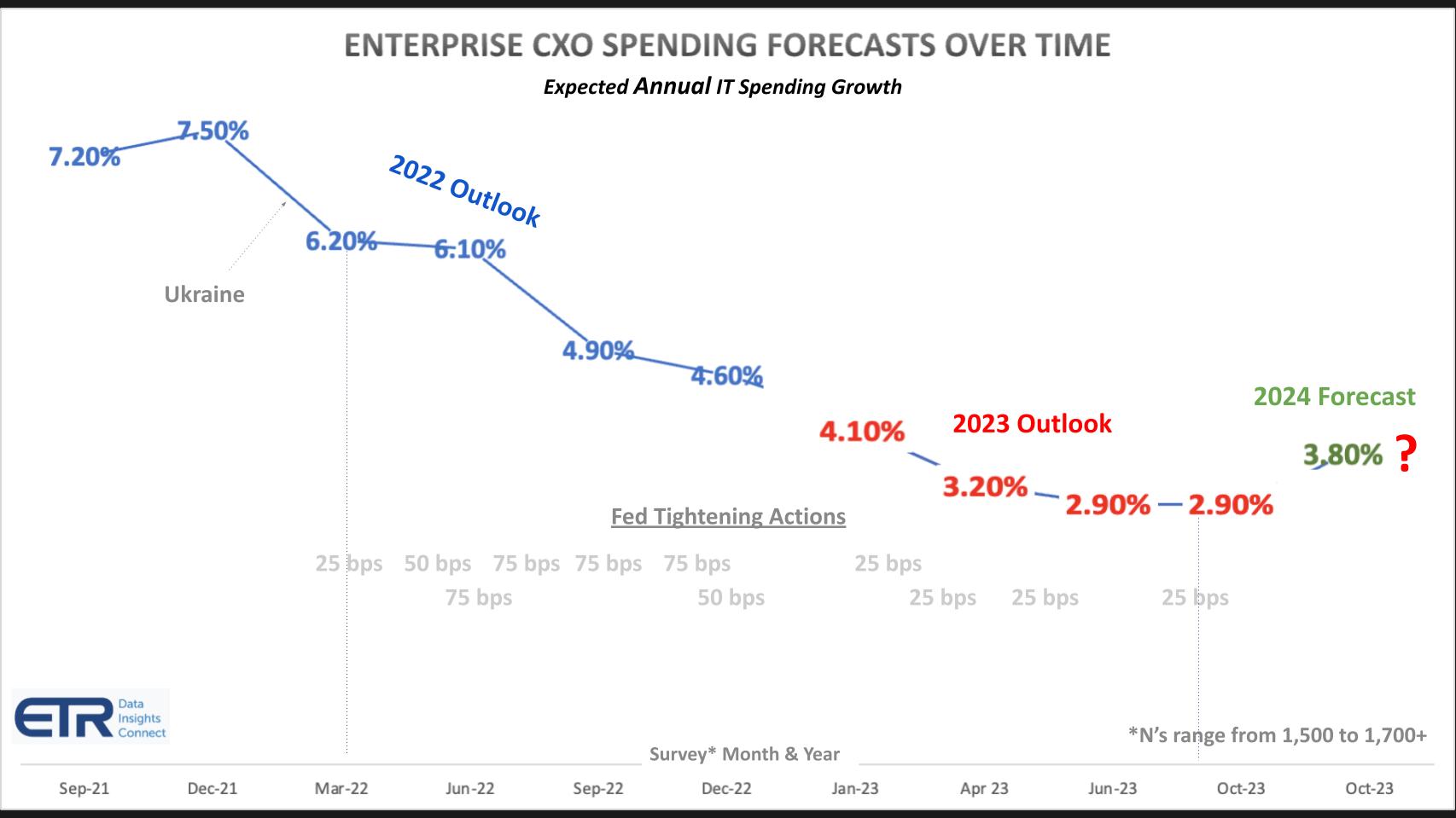

Prior to the Fed’s tightening binge for example, information technology decision makers in aggregate expected annual technology spending to increase by 7.5%. Eleven Federal Reserve interest rate hikes later, ITDMs estimate that their 2023 budgets will be up only 2.9%, with an expectation, or perhaps it’s a wishful hope, that their budgets will increase 3.8% in 2024.

In this, our 200th Breaking Analysis, we preview the current spending climate and where AI fits in relation to other sectors. We’ll also share with you a snapshot of the leaders in terms of spending velocity for their platforms; and how their performance compares to peers relative to earlier survey periods.

One of the superpowers of Enterprise Technology Research’s approach is its strict adherence to consistency over time. This allows for apples-to-apples comparisons that highlight changes at the margin.

In the above graphic we take an example using enterprise tech spending projections. The chart shows ITDMs’ expectations for annual spending growth over the past 10 quarters. The survey month and year is shown at the bottom starting with the September 2021 survey and the time series runs quarterly through October 2023. The survey Ns each quarter range from 1,500-plus to more than 1,700 completes.

The blue line shows the 2022 outlook starting in the September 2021 survey. At that time, ITDMs expected their 2022 spending levels to grow by a robust 7.2%. That figure peaked as we exited 2021 to 7.5%. Then as we progressed through the year, two significant events changed the outlook: 1) Russia’s invasion of Ukraine that February; and 2) the Fed’s relentless tightening cycle. The result is obvious in terms of a deceleration in spending expectations for the year 2022, exiting the year at 4.6%.

(Note: Actual 2022 growth estimates have from Gartner and IDC have ranged from flat to up 5.5%. We believe the figure was somewhere in the low single digits for 2022.)

The expectations for 2023 are shown on the red line. Fed tightening was having the desired effect – at least on tech spending, perhaps not so much on the consumer side. Entering 2023, expectations for the year were for 4.1% spending growth. Notice the meaningful deceleration as the Fed actions continued through September of this year to where ITDMs now believe their 2023 budget growth will be around 2.9%.

They’re hopeful that in 2024, we’ll see an uptick to spending increases of 3.8%. But given the current climate, uncertainty around debt, the election and divisive politics, the likelihood of more downward revisions is currently higher than lower.

Generative artificial intelligence is in some ways both a blessing and a curse. The excitement, potential and magic of large language models is fantastic. It creates urgency and mobilizes teams to focus on creating new forms of value, new business models, restructure processes and the like. But given the economic climate, what we’re seeing is generally not a lot of new money coming into IT budgets at the top line. Rather, there’s a reprioritization happening.

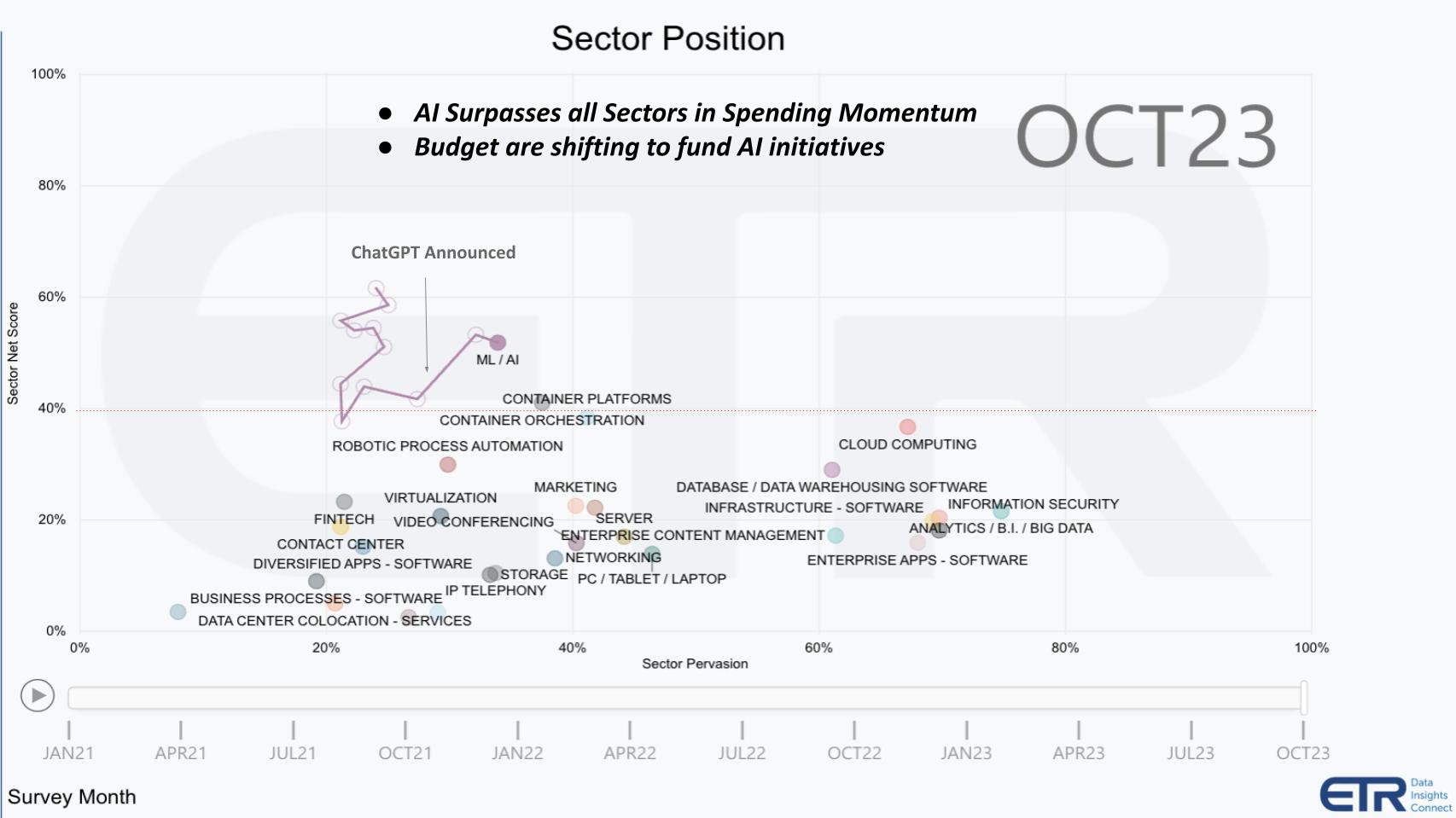

The chart above shows relative spending activity across the nearly 30 sectors in the ETR taxonomy. The vertical axis is Net Score for the sector, which is ETR’s proprietary measure of spending momentum. It essentially represents the percentage of customers that are accelerating spending in a sector by netting out those managing spending levels that are flat to down. The horizontal axis shows Sector Pervasion, which is calculated by the number of customers spending in a particular sector divided by the total N of the survey, which is around 1,725. Think of it as a proxy for market presence on an account basis, not a dollar basis.

The red line at 40% represents a highly elevated spending level. Note that during the pandemic, cloud, containers, robotic process automation and AI were the four sectors consistently above 40% on the Y axis.

The squiggly line at ML/AI represents the change in position over time. Spending levels in AI began decelerating in late 2021. Firms had over-rotated a bit on the sector and we’re directing funds to refresh infrastructure as we exited the isolation economy. But then ChatGPT is announced and the accelerated momentum returns. Almost every other sector – not all but most – started to decelerate on the vertical axis, which is an indication of shifting budget priorities to fund AI.

With generative AI, clear business value is still being sought. Budgets remain tight and other projects are being delayed while the AI experiments ramp up.

Generally, established tech companies are adapting to this new reality. Many Series B and C startups that aren’t AI companies or haven’t nailed product or go to market fit are struggling. However, mainstream enterprise tech firms raised a lot of capital during COVID, they have strong balance sheets, they’re making moves such as Cisco Systems Inc. with Splunk Inc. and many, such as CrowdStrike Holdings Inc. and Palo Alto Networks Inc., are growing. Big-name bellwethers such as Dell Technologies Inc. are throwing off cash and, in the case of Dell, it’s promising to return 80% or more of free cash flow back to back to investors. So company managements have generally adjusted nicely and have revised earnings estimates to what appear to be conservative levels.

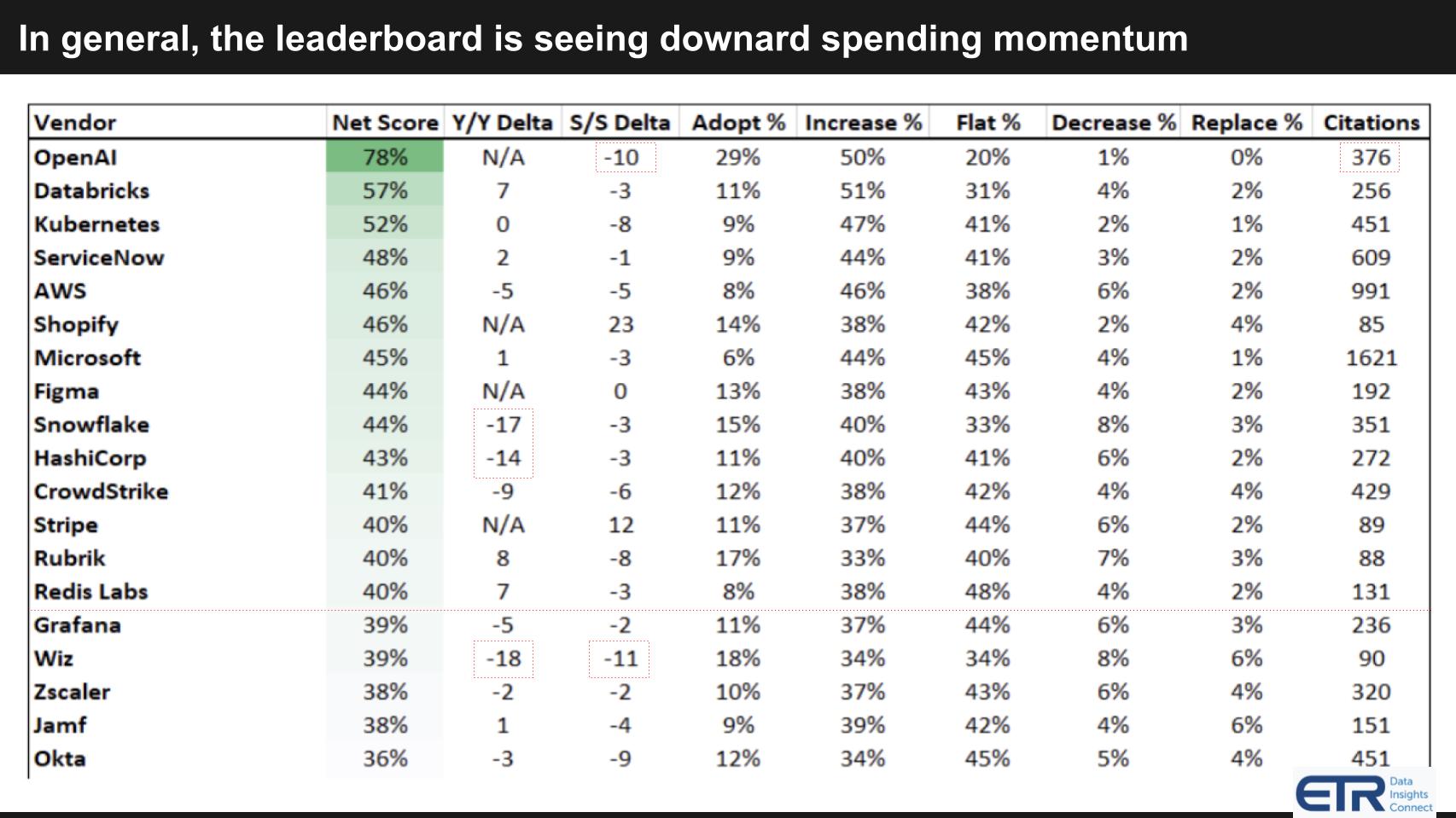

The chart below shows the leaderboard in terms of spending velocity or Net Score on their respective platforms.

The chart shows the Net Score granularity in more detail with the percent of the citations shown in the last column (i.e. survey Ns). Net Score breaks down by new adoptions, spending increasing, flat spending, spending decreasing and replacements. Net Score is calculated by subtracting the spend lesses from the spend mores and that’s what you get in the green column.

Note the red line at 40% representing a highly elevated level.

You’re probably not surprised that OpenAI LP shot up to the No. 1 position and is holding that with a 78% Net Score. They are far ahead of any other player, even though their Net Score is down 10 percentage points from last quarter’s survey. But they weren’t even in the survey last year at this time and yet they have an N that’s higher than Databricks Inc. and Snowflake Inc.

Snowflake was No. 1 in this metric for years and they came down to Databricks’ level a couple of quarters ago. Snowflake’s Net Score continues to decelerate. Remember this is an account-based metric; it doesn’t reflect spending levels. Both Snowflake and HashiCorp have come down to earth and they each show a meaningful year-over-year Net Score decline. But also notice that this is largely due to the percent of customers shifting to flat spending as opposed to spending declines and defections.

Wiz Inc. is the other notable call out on this chart as we’re seeing a meaningful change both year-over-year and survey-to-survey.

ETR recently added a FinTech sector to its taxonomy and the data on Shopify Inc. and Stripe Inc. is interesting, but out of scope for this Breaking Analysis.

We’re somewhat limited in how deep we can go with the current survey because ETR is in its quiet period and has two webcasts this month to release its results. So for now we’ll leave it there and wrap up with some thoughts on what to look for in the months and quarters ahead.

As we’ve highlighted, thus far, AI initiatives are not creating meaningful incremental funding for ITDMs. Rather, they’re stealing from other budget buckets.

Although 75% of enterprise customers are actively evaluating gen AI, of those, the vast majority (~80%) are still in evaluation mode – with privacy, legal and compliance concerns presenting key hurdles before production deployment is feasible. Plenty of “shadow AI” activity is happening, but the risks are more in focus than was the case in previous cycles such as cloud and big data.

In our view, until definitive business value can be realized via labor cost reductions or revenue generation, it is likely that the spending climate will remain cautious as higher for longer interest rates appears to be the new normal.

Right now, prudent guidance from company managements is in play and comparisons are somewhat easier than they were coming out of the pandemic. But uncertainty remains and a significant shift in sentiment could bring earnings estimates down and cause market ripples.

The world is eagerly waiting for AI to widely benefit firms beyond Nvidia Corp., internet giants and the pure-play AI companies. The real test of AI in our view will not only be the benefit that accrues to technology firms, but rather the adopters of AI across all industries. Meaningful increases in productivity can address economic headwinds and a sizzling job market and drive earnings growth. But until then, that will require technologies such as generative AI to go into production at scale and drive clear business value.

Until there’s clear evidence of economic impact, it’s best to keep watching for icebergs in the waters.

Many thanks to Alex Myerson and Ken Shifman on production, podcasts and media workflows for Breaking Analysis. Special thanks to Kristen Martin and Cheryl Knight, who help us keep our community informed and get the word out, and to Rob Hof, our editor in chief at SiliconANGLE.

Remember we publish each week on Wikibon and SiliconANGLE. These episodes are all available as podcasts wherever you listen.

Email david.vellante@siliconangle.com, DM @dvellante on Twitter and comment on our LinkedIn posts.

Also, check out this ETR Tutorial we created, which explains the spending methodology in more detail. Note: ETR is a separate company from Wikibon and SiliconANGLE. If you would like to cite or republish any of the company’s data, or inquire about its services, please contact ETR at legal@etr.ai.

Here’s the full video analysis:

All statements made regarding companies or securities are strictly beliefs, points of view and opinions held by SiliconANGLE Media, Enterprise Technology Research, other guests on theCUBE and guest writers. Such statements are not recommendations by these individuals to buy, sell or hold any security. The content presented does not constitute investment advice and should not be used as the basis for any investment decision. You and only you are responsible for your investment decisions.

Disclosure: Many of the companies cited in Breaking Analysis are sponsors of theCUBE and/or clients of Wikibon. None of these firms or other companies have any editorial control over or advanced viewing of what’s published in Breaking Analysis.

Support our mission to keep content open and free by engaging with theCUBE community. Join theCUBE’s Alumni Trust Network, where technology leaders connect, share intelligence and create opportunities.

Founded by tech visionaries John Furrier and Dave Vellante, SiliconANGLE Media has built a dynamic ecosystem of industry-leading digital media brands that reach 15+ million elite tech professionals. Our new proprietary theCUBE AI Video Cloud is breaking ground in audience interaction, leveraging theCUBEai.com neural network to help technology companies make data-driven decisions and stay at the forefront of industry conversations.