CLOUD

CLOUD

CLOUD

CLOUD

CLOUD

The ever-expanding cloud has become ubiquitous. No longer is the cloud some remote set of services, somewhere up in the sky. Rather, the cloud is seeping into every industry, hybrid on-premises models, edge workloads and telco markets, and it has its sights set on space.

The market size is staggering and will surpass $1 trillion in revenue in 2025 when including infrastructure — infrastructure as a service and platform as a service — as well as software as a service and professional services. Much artificial intelligence work is being done today in the public cloud and, despite indications that bringing AI to on-premises data will be a growing trend, it’s unlikely that the cloud will stop expanding anytime soon.

In this Breaking Analysis, we share our latest cloud market update with an expanded view beyond the typical big four hyperscalers on which we typically focus. We’ll also break down the market in more granular detail with the addition of four vendors and a more comprehensive view of the overall market. In addition, we’ll drill into the IaaS and PaaS markets and set up a framework for future research.

First, let’s start with the survey data from Enterprise Technology Research to understand how customers think about their cloud platforms.

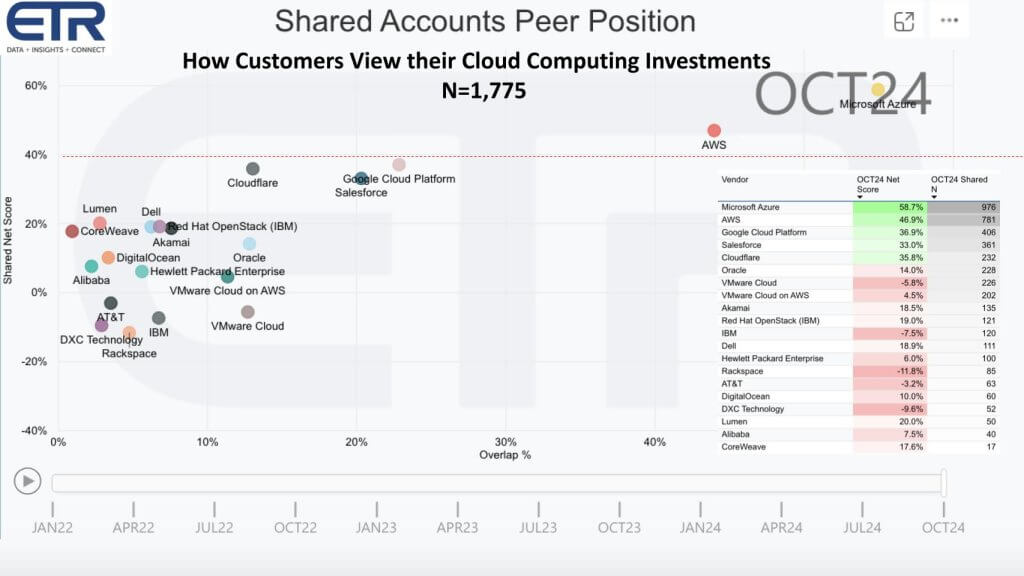

This two-dimensional chart above is a common view we like to share. It’s based on ETR’s October TSIS survey (Technology Spending Intentions Survey) of 1,775 information technology decision makers. This view represents the cloud computing sector. Approximately 1,200 of those 1,775 respondents in the N above provided data on their cloud platform spending patterns. The vertical axis shows Net Score or spend momentum on a particular platform and the horizontal axis shows Overlap or penetration within those respondent accounts.

The table insert shows each vendor, their Net Score and the N number of responses, which is an indication of market penetration. This data informs how the dots are plotted. You can see Microsoft Corp. and Amazon Web Services Inc. are prominent and dominant with 976 and 781 N respectively. Note the red line at 40%. That’s an indication of a highly elevated Net Score and only AWS and Microsoft are above that line.

Google Cloud is close to that line and we’ve seen increased penetration on the X-axis since the launch of ChatGPT. It’s clear AI is a tailwind for Google as it closes in on AWS within the ML/AI sector (not explicitly shown). Notice Salesforce Inc. and now CoreWeave Inc. have hit the list for the first time. Del Technologies Inc., Red Hat Inc., IBM Corp., Hewlett Packard Enterprise Co., Oracle Corp., VMware Inc., Rackspace Technology Inc., DXC Technology Co., AT&T Inc., Digital Ocean Inc., Cloudflare Inc., Alibaba Group Ltd., Akamai Technologies Inc. and Lumen Technologies Inc. also show up on the chart.

The point is, this is how customers view cloud when you ask them which clouds they’re using. Their responses represent a wide variety of platforms, from public cloud hyperscalers to SaaS companies to service providers, hosting companies and more.

With this background, it’s a good point to look at a more comprehensive view of the cloud market than in our previous episodes — in other words, a view of the cloud market beyond the four big hyperscalers and one that aligns more closely with how customers look at their clouds.

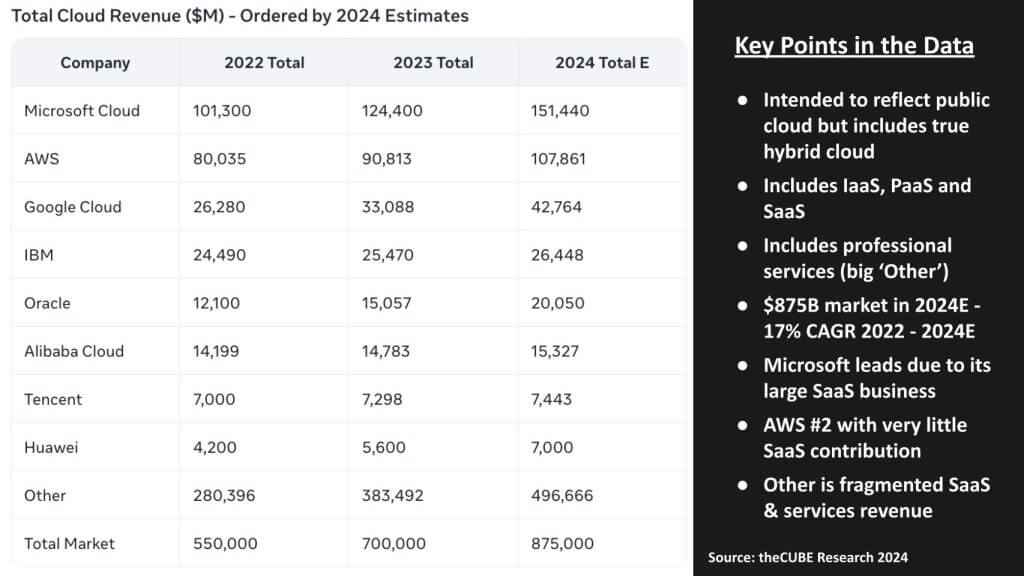

The table above shows our attempt to size the total cloud market. We’ve expanded the scope beyond the four hyperscalers we usually focus on (AWS, Azure, GCP and Alibaba) to include hybrid cloud players such as IBM and Oracle, which both own public clouds, and two additional cloud players in China, Tencent Holdings Ltd. and Huawei Technologies Co. We’re attempting to size IaaS, PaaS, SaaS and include cloud-based professional services. Notice the big “Other,” which includes both other SaaS and professional services.

We pursued a top-down methodology to size the overall market using the following logic. IT spending is around $5 trillion worldwide, of which about two-thirds is staffing. So that means about $2 trillion is vendor revenue and cloud at $875 billion makes up about 40% of that spend, a figure we’ve derived from our work with ETR survey data and other information we’ve modeled over the years. The total market is growing at a 17% CAGR from 2022 to 2024. You can see Microsoft is No. 1 because of its large SaaS contribution. AWS is second in this view with very little SaaS and services.

At these growth rates, the market surpasses $1 trillion in 2025.

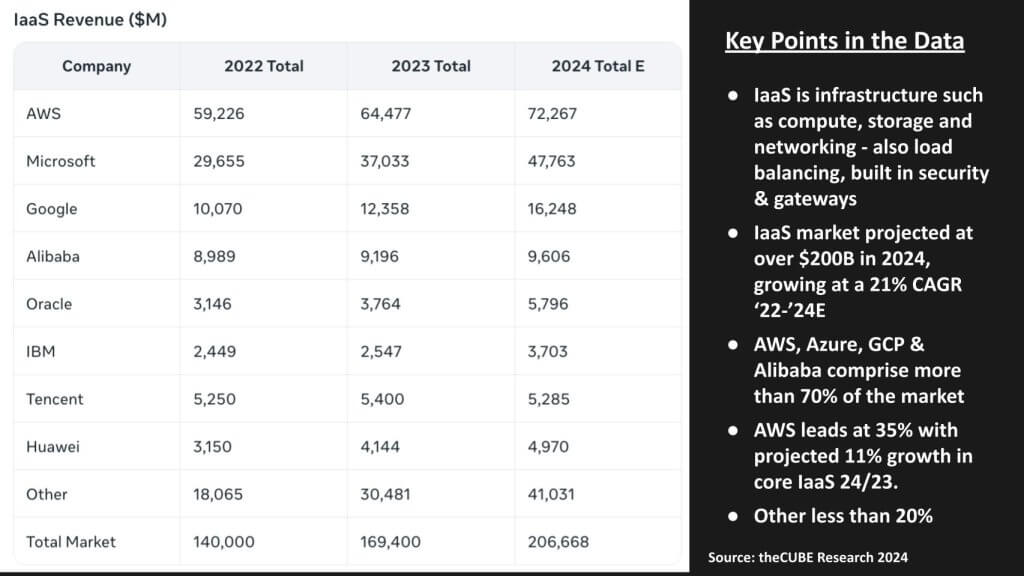

The previous data provides a view of the very big picture of cloud computing. Let’s break it down further starting with IaaS. It includes the core compute, storage and networking services. We also include in our definitions services such as load balancing, any built-in security, gateways and other core infrastructure.

The market as shown above is projected to approach $207 billion in 2024, which is a 21% CAGR from 2022 to 2024. AWS, Azure GCP and Alibaba dominate with more than 70% of the market. AWS leads with 35% of the market and we believe its IaaS business is growing more slowly than its overall cloud business as AWS’ PaaS mix increases and SaaS grows from a much smaller base.

Oracle is a big growth story in this space as it gears up OCI, procures graphics processing units from Nvidia Corp. and provides mission-critical database and application infrastructure powered by Advanced Micro Devices Inc., Intel Corp. and Ampere Computing Inc. Meanwhile, the players in China are sorting through local market economic challenges and some restructuring of their cloud business models. But as you can by their revenue, they are major players in local China and Asia-Pacific regions.

Unlike in SaaS and services, “Other” in this segment accounts for less than 20% of the revenue.

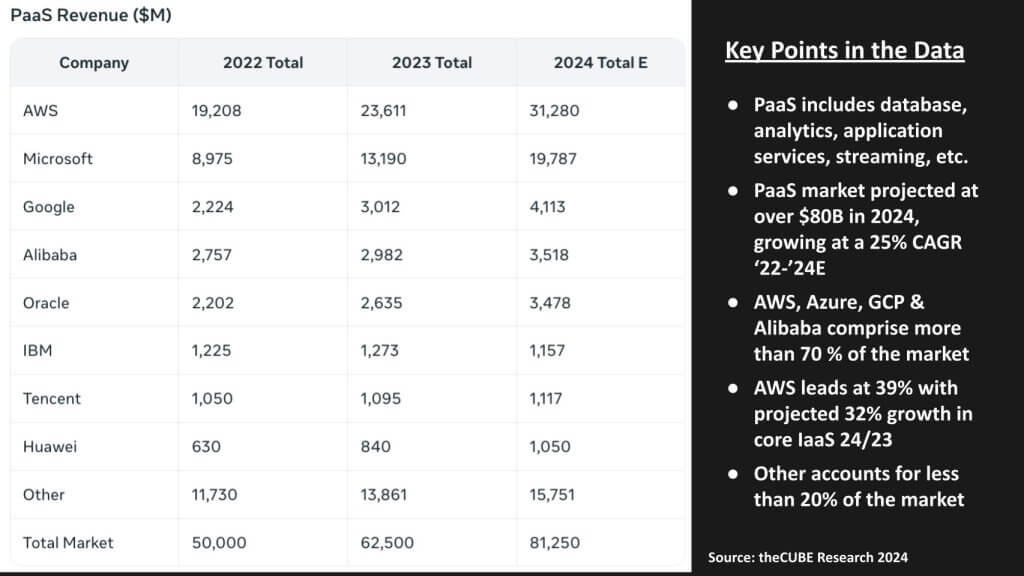

Let’s take a look at the platform-as-a-services projections. PaaS includes core database and related services, analytics, application services, streaming, machine learning and AI tools and related platform services. The market, as shown below, is projected to grow to over $80 billion this year at a 25% compound annual growth rate from 2022 to 2024. As with IaaS, the big four cloud players account for more than 70% of the market and the “Other” players are less than 20%.

PaaS is increasingly strategic and is the glue between infrastructure and applications.

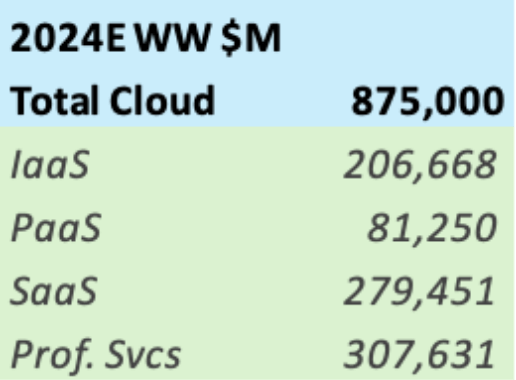

Our top-down, bottom-up methodology takes our estimates of IaaS and PaaS and subtracts them from the total market to quantify the leftover portion of the market which we have assumed represents SaaS and cloud professional services. In total it represents more than $500 billion in 2024 estimated revenue, of which we believe just over 50% represents professional services. So roughly speaking, our 2024 estimates are as shown below:

We’re not ready to expose our SaaS and cloud professional services granularity at the moment. You saw in the ETR data names such as Salesforce and DXC, representing both software and services firms. But there are many more. ServiceNow Inc. and Workday Inc. for example in SaaS and Accenture plc in services. IBM is services- and SaaS-heavy, as are many others. Unlike IaaS and PaaS, where “Other” comprises less than 20% of the market, in SaaS and Services, our “Other” category currently accounts for almost 75% of the spend. So we need to do more work before we release that data to the public.

Notably, the marginal economics of SaaS are extremely attractive, whereas the same is not true for professional services. As such separating those two is an important next step in our research.

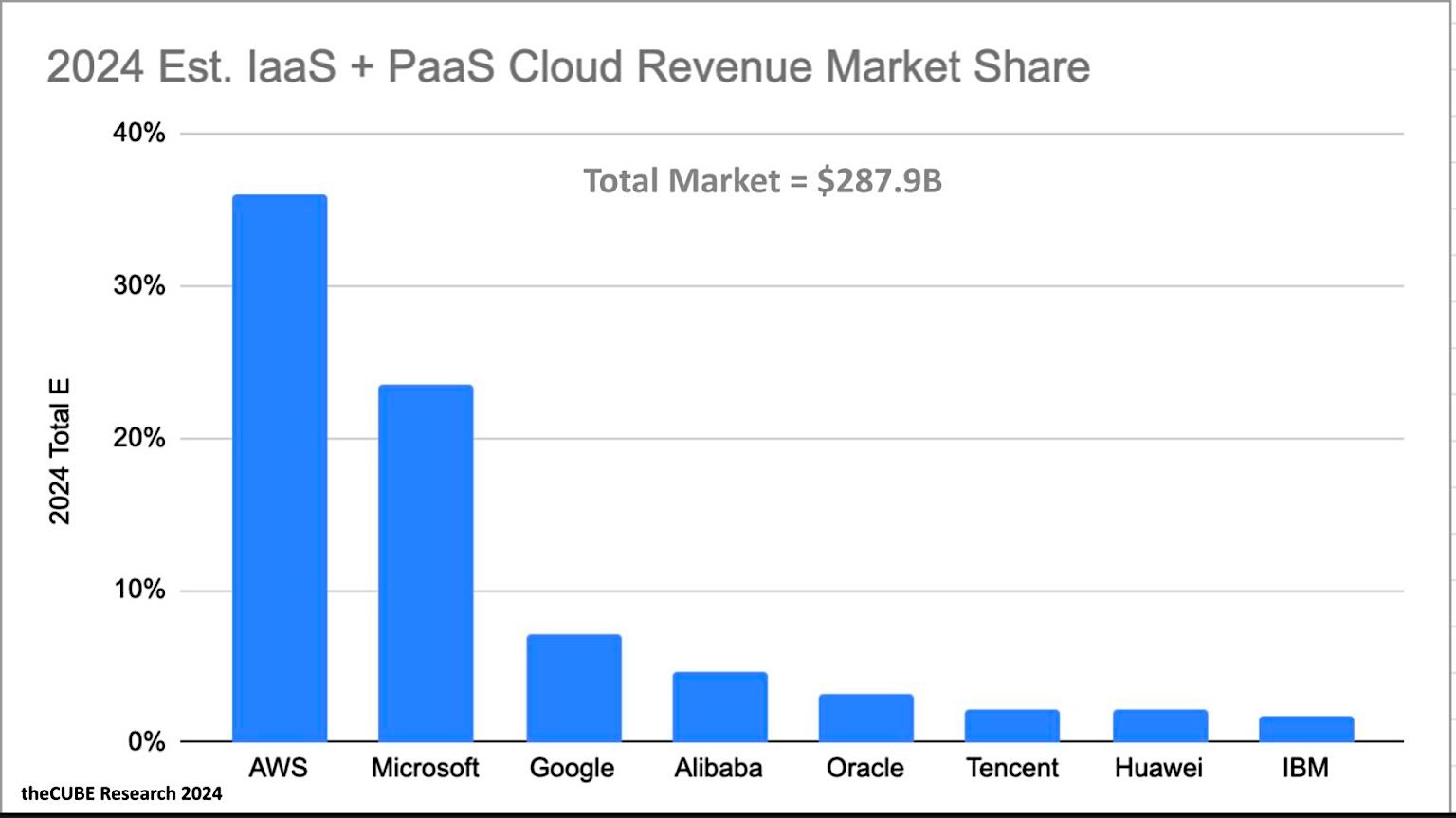

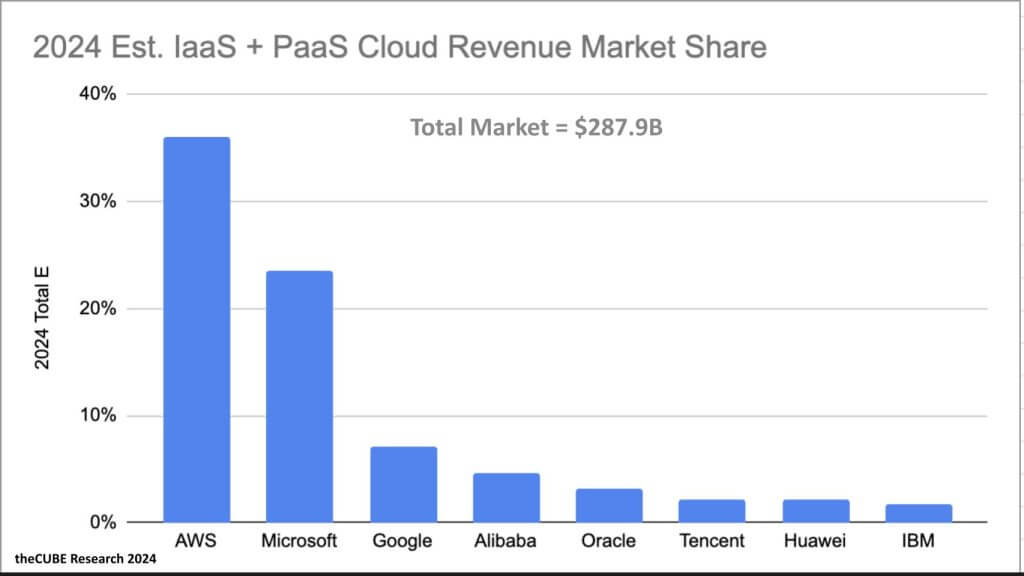

We’ll close with a consolidated look at the IaaS and PaaS markets, stripping out Microsoft’s large SaaS business. Same with Google. This gives us more of an apples-to-apples comparison with AWS’ business.

Above we show the revenue shares for our eight cloud companies in the combined IaaS/PaaS cloud market at nearly $300 billion projected for 2024. AWS has 36% of this combined market, Microsoft 23% and Google 7%. Alibaba, Oracle Tencent Huawei and IBM combine for around 14% of the market with “Other” (not shown) at 20%.

The cloud market continues to grow rapidly, driven by increasing adoption of cloud services across industries. AWS, Microsoft and Google remain the top players, while Oracle and other players are gaining traction.

When including SaaS and services and accounting for the preponderance of “Other” players the market takes on a different dimension. The SaaS and services markets are highly fragmented and while much of the SaaS industry runs on the public cloud, the revenue captured by non-hyperscalers is substantial. Professional services, always the largest category, consumes another big chunk of revenue.

Remember, these models use a combination of top-down and bottom-up methodologies. The IaaS and PaaS figures for AWS, Microsoft, Google and Alibaba have the highest degree of confidence — notwithstanding the fact that interpreting financial data and mapping to create an apples-to-apples comparison is as much art as it is clean financial math.

The Oracle and IBM data are somewhat more precise than the other vendors, but both firms have somewhat opaque and often fluctuating reporting methods for their cloud businesses with frequently changing definitions. But anecdotal data is strong for both companies given their respective histories and U.S.-based locations. As well, survey data is more available for these U.S.-based firms. The data on Tencent and Huawei are interpreted through bits and pieces of information, financial reports, limited survey data and conversations with local sources in China, including individuals in the community that have visibility on those firms.

Much of the SaaS and services data is interpreted through top down methodologies, taking into account financial statements, management commentary on cloud performance, guidance on earnings calls and subtracting IaaS and PaaS estimates from total cloud figures, which we derived based on the top-down methodology discussed earlier. As indicated, the SaaS and services markets are highly fragmented, definitionally opaque in earnings reports and extremely large. The same is true for “cloud” as each vendor has a different interpretation of what they include in their cloud reporting.

So there you have it. We’ve tried to give you additional granularity in our data sets as a service to the community. We’ll continue to refine this over time and appreciate your feedback on where you think we got it right and how we can improve the models.

Let us know.

Support our mission to keep content open and free by engaging with theCUBE community. Join theCUBE’s Alumni Trust Network, where technology leaders connect, share intelligence and create opportunities.

Founded by tech visionaries John Furrier and Dave Vellante, SiliconANGLE Media has built a dynamic ecosystem of industry-leading digital media brands that reach 15+ million elite tech professionals. Our new proprietary theCUBE AI Video Cloud is breaking ground in audience interaction, leveraging theCUBEai.com neural network to help technology companies make data-driven decisions and stay at the forefront of industry conversations.