CLOUD

CLOUD

CLOUD

CLOUD

CLOUD

Twenty-one straight quarters of declining revenue: No wonder investors are getting a little weary of IBM Corp.’s turnaround attempt, dubbed “tedious” by one analyst Monday.

Today’s second-quarter earnings report didn’t change anybody’s mind. The computer and services giant reported a profit before certain items such as acquisition and retirement costs of $2.97 a share, up 1 percent from a year ago. Revenue fell 5 percent, to $19.3 billion, or down 3 percent adjusted for currency changes.

The bottom line beat analysts’ forecast of an adjusted profit of $2.75 a share, but the top line fell short of the $19.46 billion analysts had expected and marked the steepest fall in five quarters. IBM reiterated a forecast for this year of “at least” a $13.80-a-share profit for 2017 before certain costs, while analysts peg it at $13.68.

Investors reacted with mild displeasure as IBM’s shares fell more than 3 percent in after-hours trading following a 2 p.m. earnings conference call. That was a less negative reaction than the 5 percent drop after the first-quarter announcement on April 18. In regular trading today, IBM’s shares rose about 0.7 percent, to $154 a share. The stock is down about 8 percent on the year.

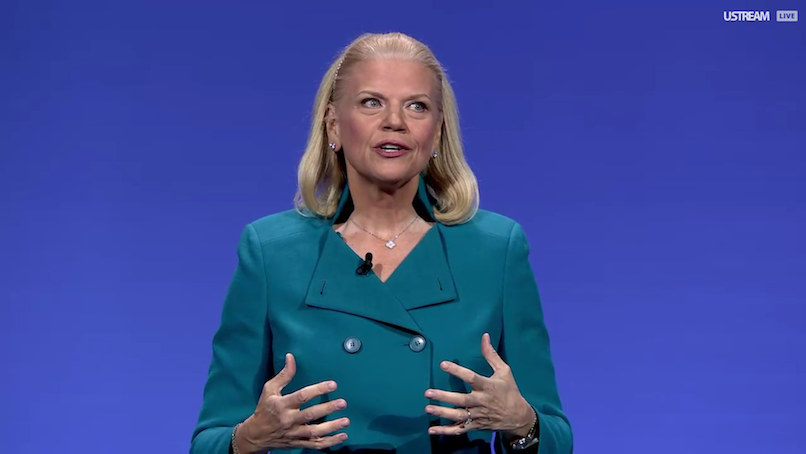

Under Chief Executive Ginni Rometty (pictured) for the past six years, IBM has been struggling to move from a decades-long dependence on mainframes and related software and services to offering cloud computing services such as those dominated by Amazon Web Services Inc., Microsoft Corp.’s Azure and others.

IBM’s “strategic imperatives” in cloud, big data analytics, security and other areas are growing. In the second quarter, revenues from them rose 5 percent from a year ago, or 7 percent absent currency shifts, to $8.8 billion — though that was a considerable slowdown from 12 percent in the first quarter. Cloud revenue in particular rose 15 percent, and IBM said annual run rate of as-a-service subscription revenue jumped 30 percent from a year ago, to $8.8 billion.

“We strengthened our position as the enterprise cloud leader and added more of the world’s leading companies to the IBM Cloud,” Rometty said in a statement. In particular, IBM singled out several big, multiyear cloud deals with Lloyds Banking Group plc, American Airlines Inc. and Bombardier Inc.

But the new businesses still aren’t yet big enough, or growing fast enough, to offset declines in its traditional businesses. “IBM is very liberal with what they count as ‘strategic,’ which is growing as a percentage of their business, but it’s still not turning the aircraft carrier yet,” said Ralph Finos, an analyst with Wikibon, owned by the same company as SiliconANGLE.

Even its Watson artificial-intelligence system has appeared to lose traction. One analyst, Jefferies & Co.’s James Kisner, late last week said IBM is getting “outgunned” in AI by the likes of Google Inc., Microsoft, Amazon.com Inc. and Facebook Inc. Indeed, IBM said revenues from its Cognitive Solutions business of which Watson is a part fell 2.5 percent, to $4.6 billion, from a year ago.

IBM continues to pin at least some of its hopes on mainframes, the latest model of which it announced Monday. But overall, it’s pitching itself as the best way for large enterprises to use cloud computing. “We know how to migrate them from one era to another,” Martin Schroeter, IBM’s chief financial officer, said on the conference call. As a result of pending big new deals, he said, “We expect our revenue trajectory to improve in the second half,” though he didn’t predict actual revenue growth.

Analysts remain doubtful. Barclays analyst Mark Moskowitz said in a note to clients Monday that IBM’s multiyear turnaround effort was becoming “tedious” thanks to “a lot of investments in next-gen tech but with little revenue impact and with increasing dependence on cost take-outs or below-the-line items to manage EPS.” He reiterated the point in a research note Wednesday, partly based on slowing strategic-imperative revenues. “There are no major changes in place to drive a high-quality revenue and margin recovery,” he wrote.

Indeed, every segment in IBM’s business was down, from Cognitive Solutions to Global Business Services (down 3.7 percent, to $4.1 billion), Technology Services & Cloud Platforms (down 5.1 percent, to $8.4 billion), Systems (down 10.4 percent, to $1.7 billion) and Global Financing (down 2.2 percent, to $415 million).

Skepticism about IBM’s prospects also stems from an essential dilemma: The more it gets customers to move to its cloud, the more it reduces its core business.

“Their primary cloud business is converting the largest, most complex enterprises from IBM’s own non-cloud platforms onto their infrastructure-as-a-service cloud platforms — which is going to result in less revenue for IBM,” Finos said. “At some point they get ahead of the curve with their installed base of highly desirable users, but just how long is this going to take?”

As the latest quarter appears to indicate, it could take quite a while.

Support our mission to keep content open and free by engaging with theCUBE community. Join theCUBE’s Alumni Trust Network, where technology leaders connect, share intelligence and create opportunities.

Founded by tech visionaries John Furrier and Dave Vellante, SiliconANGLE Media has built a dynamic ecosystem of industry-leading digital media brands that reach 15+ million elite tech professionals. Our new proprietary theCUBE AI Video Cloud is breaking ground in audience interaction, leveraging theCUBEai.com neural network to help technology companies make data-driven decisions and stay at the forefront of industry conversations.