CLOUD

CLOUD

CLOUD

CLOUD

CLOUD

The steepest drop in the stock market since June 11 flipped the narrative and sent investors scrambling this week. Tech got hammered after a two-month run and people are asking questions: Is this a bubble popping or a healthy correction? Are we now going to see a rotation into traditional stocks like banks and certain cyclicals that have lagged behind the technology winners?

In this week’s Breaking Analysis we want to give you our perspective on what’s happening in the technology market and unpack what this sentiment flips means for the balance of 2020 and beyond. As always we’ll reference survey and model data from Enterprise Technology Research to support our opinions.

The tech markets recoiled this week as the Nasdaq composite index dropped almost 5% in a single day. Apple Inc.’s market cap alone lost $178 billion. The big four — Apple, Microsoft Corp., Amazon.com Inc. and Google LLC owner Alphabet Inc. lost a combined value that approached a half-trillion dollars. For context, this number is larger than the gross domestic products for countries as large as Thailand, Iran, Austria, Norway, the UAE and many more.

The tech stocks that have been running thanks to COVID-19 got crushed. These are the ones we’ve highlighted as best positioned to thrive in the pandemic — the work-from-home, software-as-a-service, cloud and security stocks. We’re talking about Zoom Inc., ServiceNow Inc., Salesforce.com Inc., DocuSign Inc., Splunk Inc. and the security names such as CrowdStrike Holdings Inc., Okta Inc. and Zscaler Inc. By the way, Docusign, CrowdStrike and Okta all had nice earnings beats but still got killed, underscoring the sentiment shift.

The broader tech market was off in sympathy and this trend continued into the Labor Day holiday.

There are many opinions on what happened. First, many like us are relatively happy because this market needed to take a break. As we have said before, the stock market is not reflecting the realities of the broader economy. As we head into September in an election year, uncertainty kicks in. But it really looks like this pullback was fueled by a combination of an overheated market and technical factors.

Specifically, volatility indices were high yet markets kept rising. Robinhood millennial investors who couldn’t bet on sports realized that investing in stocks was as much of a rush and potentially more lucrative. The other big wave, which was first reported by the Financial Times, is that SoftBank Holdings Inc. made a huge bet on tech and bought options tied to around $50 billion worth of high-flying tech stocks.

So the options call volume skyrocketed. The call-versus-put ratio was getting way too hot, and we saw an imbalance in the market. Market makers will often buy an underlying stock to hedge call options to ensure liquidity in these cases.

To be more specific, delta in options is a measure of the change in the price of an option relative to the underlying stock. And gamma is a measure of the volatility of the delta. Usually volatility is relatively consistent on both sides of the trade – calls and puts – because investors will hedge their bets. But in the case of many of these hot stocks, such as Tesla for example, you’ve seen the call skew be much greater than the skew on the downside.

So for example, if people are buying cheap out-of-the-money calls, a market maker might buy the underlying stock to hedge for liquidity. Then if Elon Musk puts out some good news, the stock goes up, market makers have to buy more of the underlying stock, algorithms kick in to buy more and then the price of the call goes up as it approaches its money price. That forces the market makers to keep buying more of the underlying stock and the melt-up continues.

That is, until it stops and the market flips like it did this week. When stock prices begin to drop, market makers will rebalance their risks and sell their underlying stocks and then the rug gets pulled out from the market for these stocks that have run.

So why am I spending so much time on this? And why am I not freaking out? Because I think these market moves are largely technical versus fundamental. It’s not like 1999 where you had a double whammy of technical rug pulls combined with poor underlying fundamentals for high-flying companies such as CMGI and Internet Capital Group, whose business was all about placing bets on dot-coms that had no business models other than unmonetized eyeballs.

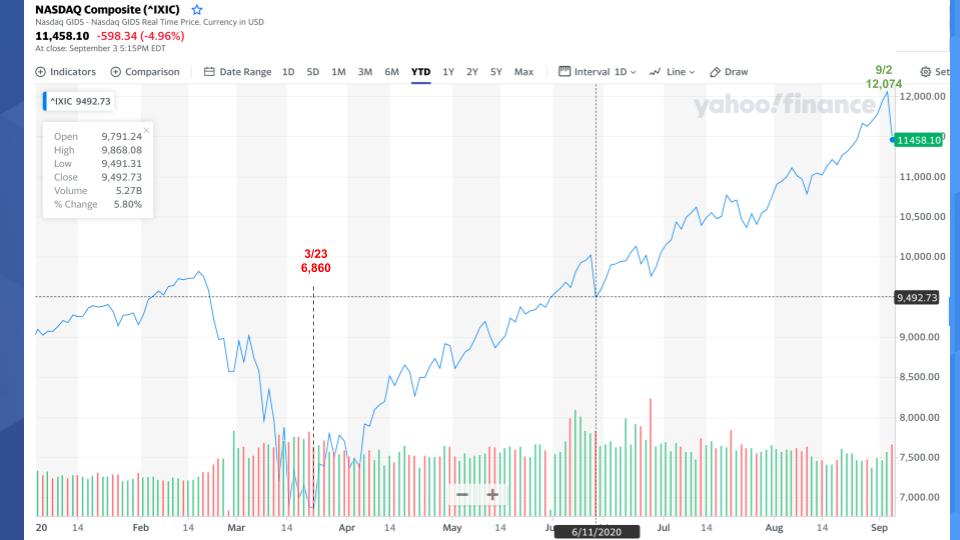

Below is a year-to-date chart of the Nasdaq. You can see it bottomed on March 23 at 6860, then ran up until June 11 and had that big drop but was still elevated at 9492. Then it ran up to over 12,000 and an all-time high. And then the big drop.

The trend continued on Friday morning. The NASDAQ composite traded below 11,000. It actually corrected to 10% off its high – 9.8%, to be precise. And then it snapped back but pulled back again at the close of day.

But even at its low, that’s still up over 20% for the year. In the year of COVID-19, would that have surprised you in March?

So to us this pullback is a relief. It’s good and actually very normal and predictable. The exact timing of these pullbacks, on the other hand, is entirely unpredictable.

The economy continues to improve. The August jobs report was good with 1.4 million new jobs and 340,000 coming from the government. Those are positive numbers and translate into a drop in unemployment to 8.4%. This is good relative to expectations and yet the selloff continued, which suggested the market wanted to keep correcting. So good, maybe some buying opportunities will emerge over the next several months for those that have been waiting. Still, the market snapped back, so we will see.

But we think there are more opportunities ahead because there’s so much uncertainty., such as what’s going to happen with the next round of stimulus. The jobs report could be a catalyst for a compromise between the Democrats and the Republicans.

U.S. debt is projected to exceed 100% of GDP this calendar year. Does that give you a good feeling? And we talked about the election already. So there’s lots to think about.

As we’ve been projecting for months with our colleagues at ETR, despite the stock market’s rise and some real tech winners, we still see a contraction in 2020 information technology spending of 5% to%. And we talk a lot about the bifurcation in the market from COVID accelerating trends that were already in place – that is, digital transformation, SaaS and cloud, but then work-from-home kicked in other trends, including videoconferencing and a shift in security spending.

We think this will continue for years. However, because these stocks have run up so much, they are going to have very tough compares in 2021.

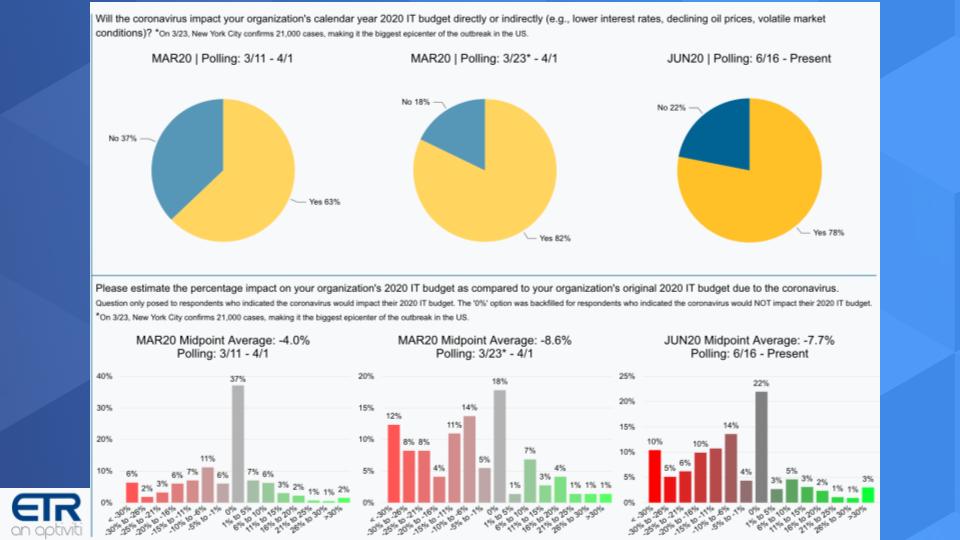

The data below is from a series of surveys ETR conducted to better understand spending patterns due to COVID. The yellow slices of the pies show the percentage of customers that indicate that their budgets will be affected by pandemic. And you can see the steady increase from mid March to June – from 63% to 78% saying yes.

The bottom part of the chart shows the degree of change. Some 22% say no change in the latest survey, but you can see much more of a skew to the red declines on the left versus the green upticks on the right of the charts.

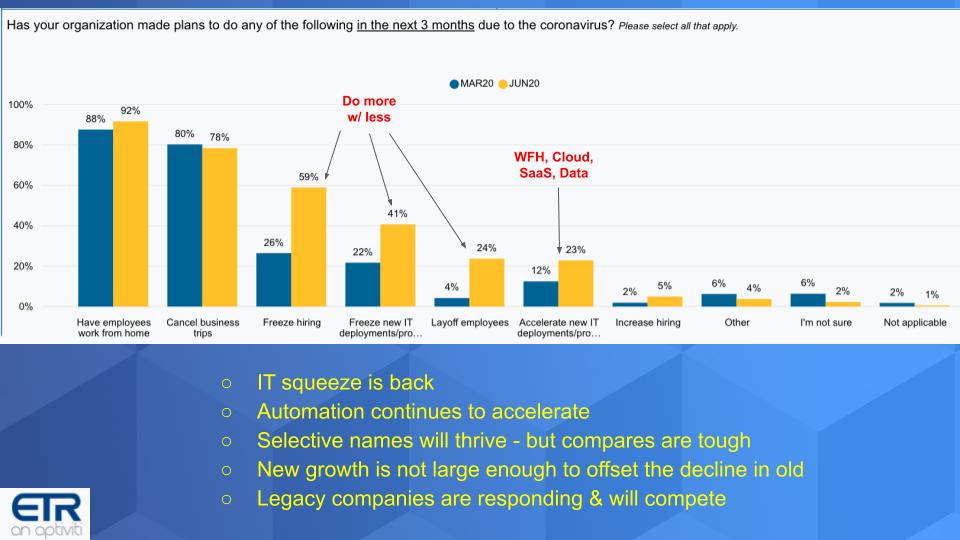

The chart below shows what companies are doing as a result of COVID-19.

Of course everyone’s working from home and not traveling (first two bar categories). But look at the increases in hiring freezes, freezing new IT deployments and the sharp rise in layoffs. So IT is again being asked to do more with less.

We see this driving an acceleration to automation and that will benefit the RPA players, cloud providers and modern software vendors. It will precipitate a tailwind for more aggressive artificial intelligence implementations.

And many other selected names are going to continue to do well, those in the work-from-home, cloud, SaaS and modern data sectors.

But the problem is those growth sectors are not large enough to offset the declines in the core businesses of the legacy players – which have a much higher market share. So overall the IT spend declines.

Now where it gets interesting is that the legacy companies all have growth businesses. IBM Corp. has its hybrid cloud business and Red Hat. Dell Technologies Inc. has VMware Inc. and work-from-home solutions, Oracle Corp. has SaaS and cloud, Cisco Systems Inc. has its security business, Hewlett Packard Enterprise Co. has its as-a-service initiative and so forth.

These businesses are growing faster, but they are not large enough to offset the declines in core on-premises legacy business and drive anything more than flat growth overall at best. And by the time they are large enough, we will be on to the next big thing.

But these legacy companies will compete with the upstarts and that’s where it gets a bit fuzzy for market forecasters.

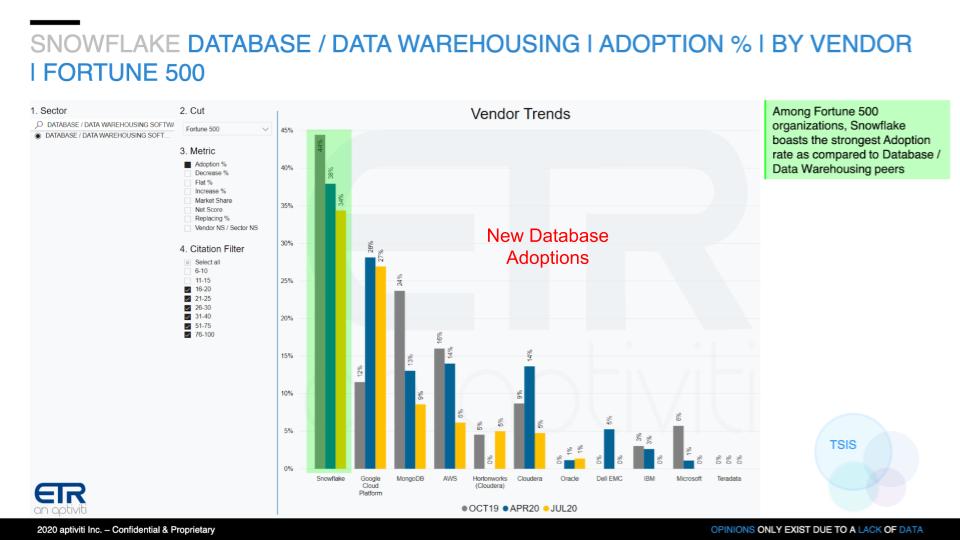

We’ll start with one of our favorites below: Snowflake Inc. Like Asana Inc. and JFrog Ltd., Sumo Logic Inc. and Unity Technologies, Snowflake has a highly anticipated upcoming initial public offering.

This chart shows new adoptions in database. Snowflake, while down from the October 2019 survey, is far outpacing its competitors with the exception of Google, where BigQuery is doing very well. MongoDB Inc. and Amazon Web Services Inc. remain strong and I’m actually encouraged that it looks like Cloudera Inc. has righted the ship and you saw this in its recent earnings report.

But my point is that Snowflake is a share gainer and will likely continue to be one for a number of quarters and years, if it can execute and compete with the big cloud players. We think it can.

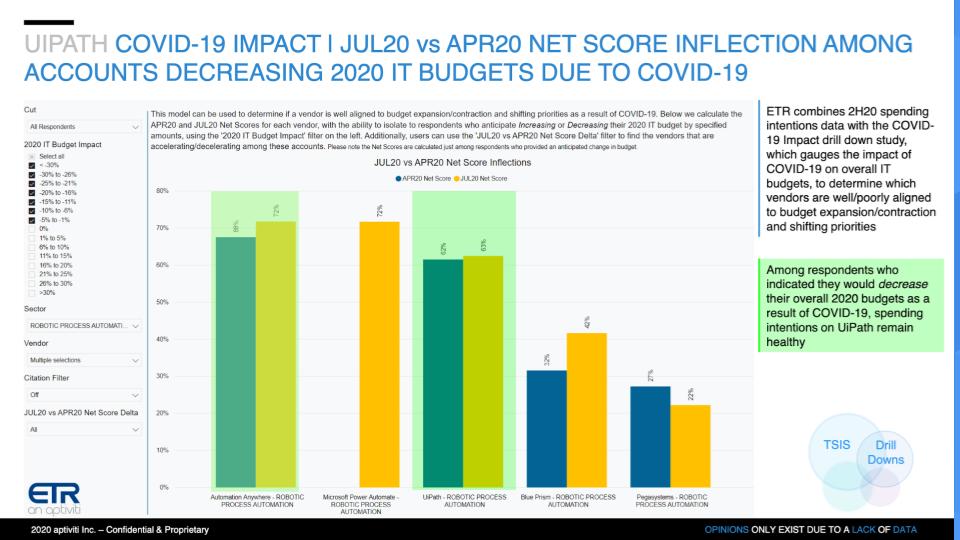

This is another market segment we’ve covered a lot, focusing on two leaders, UiPath Inc. and Automation Anywhere Inc.. But we still like Blue Prism Group and we especially like Pegasystems Inc., which has for years been embarking on a broader automation agenda.

The chart above shows Net Score or spending velocity data for those customers that said they were decreasing spend in 2020 – those red bars we showed earlier. And you can see both AA and UiPath show elevated levels. Microsoft, as we’ve reported, is elbowing its way into the market with what is currently an inferior product — but it is Microsoft so we can’t ignore them.

The chart below cherry-picks a few of our favorite names and shows the Net Score granularity for some of the leaders and emerging players.

All these players are in the green as you can see in the upper right and they all have a decent presence in the data set based on the Ns. Okta is at the top of the list with a 58% Net Score. Palo Alto Networks Inc. is a more mature player but still has an elevated Net Score. CrowdStrike’s Net Score dropped this quarter, which is a bit of a concern but it’s still high, followed by SailPoint Technologies Inc. and Zscaler. The big three trends in this market right now are cloud security, identity access management and endpoint security. And we think these trends have legs.

Now everyone on this chart has reported earnings except Zscaler, which reports on Sept. 9. And all of these companies are all doing well and exceeding expectations. But as I said earlier, next year’s compares won’t be so easy. And their stock prices all got killed as a result of the rug pull. So we really feel this isn’t a fundamental problem for all of these firms – it’s more technical.

We don’t know about AA and UiPath because they are not public and we think they need to get their house in order so they can IPO, so we’ll see when they make it to public markets. We don’t think that’s an “if” They will IPO, but the fact that they haven’t filed yet says they’re not ready. Why wouldn’t you IPO if you were ready in this market – despite the recent pullback?

OK, all you new investors out there who think you’re a stock picking pro. Any fool can make money in a market that goes up every day. But trees don’t grow to the moon. There are bulls, bears and pigs, and pigs get slaughtered. And I could throw a dozen other cliches at you. But we are excited that you’re learning. Maybe you made a few bucks playing the options game – it’s not as easy as you may think. We hope you don’t trade on margin.

But look, we think there will be some buying opportunities ahead– there always are. Be patient. It’s very hard – actually impossible – to time markets and we’re fans of dollar cost averaging. And young single people making less than $137,000 a year: Load up on your Roth IRA. It’s a government gift that we wish we could’ve tapped when we were newbie investors. And as always, do your homework.

Remember these episodes are all available as podcasts – please subscribe. We publish weekly on Wikibon.com and SiliconANGLE.com so check that out, and please do comment on the LinkedIn posts we publish. Don’t forget to check out ETR for all the survey action. Get in touch on twitter @dvellante or email david.vellante@siliconangle.com. Breaking Analysis posts, videos and podcasts are all available at the top link on the Wikibon.com home page.

Here’s the full video analysis:

Support our mission to keep content open and free by engaging with theCUBE community. Join theCUBE’s Alumni Trust Network, where technology leaders connect, share intelligence and create opportunities.

Founded by tech visionaries John Furrier and Dave Vellante, SiliconANGLE Media has built a dynamic ecosystem of industry-leading digital media brands that reach 15+ million elite tech professionals. Our new proprietary theCUBE AI Video Cloud is breaking ground in audience interaction, leveraging theCUBEai.com neural network to help technology companies make data-driven decisions and stay at the forefront of industry conversations.