INFRA

INFRA

INFRA

INFRA

INFRA

Throughout the pre-vaccine COVID era, information technology buyers indicated budget constraints would squeeze 2020 spending by roughly 5% relative to 2019 levels. But the forced march to digital, combined with increased cybersecurity threats for remote workers, created a modernization mandate that powered fourth-quarter spending last year.

This momentum has carried through to 2021. Although COVID variants have delayed return-to-work and business travel plans, our current forecast for global IT spending remains strong at 6% to 7%, slightly down from previous estimates. But the real story is that chief information officers and IT buyers expect a 7% to 8% increase in 2022 spending, reflecting investments in hybrid work strategies and a continued belief that technology remains the underpinning of competitive advantage in the coming decade.

In this Breaking Analysis, we’ll share the latest results of Enterprise Technology Research’s macro spending survey and update you on industry and sector investment patterns.

Based on ETR’s latest survey, currently with 869 responses as shown above, we expect a slight pullback in spending expectations from CIOs and IT buyers to roughly 6% to 7% down from 7% to 8% earlier this year, reflecting caution over return-to-office strategies. But buyers continue to expect robust spending into next year as they support hybrid models, modernize their headquarters infrastructure and continue to move forward on digital transformation efforts.

Cybersecurity and cloud remain the top two priorities ,with data initiatives overtaking collaboration and productivity on the priority list – although all three of these areas remain strong, as does robotic process automation.

Organizations now expect about 44% of employees to be working in a hybrid model over the long term, with 37% currently working in a hybrid fashion.

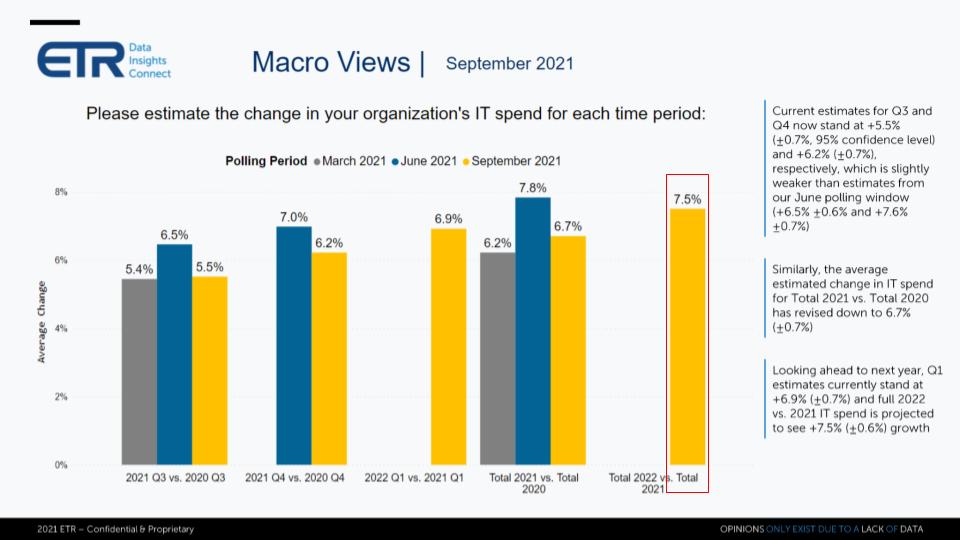

The chart below compares the spending growth expectations from the March, June and September 2021 ETR surveys.

These are not radical changes, as you can see by the downward trajectory of the yellow bar. It reflects the reality of the continued uncertainty caused by the pandemic. Organizations are dealing with that reality and remaining flexible with regard to strategies and spending outlook. But the 2022 bar on the far right at 7.5% is telling, as buyers expect spending levels in 2022 to outpace historical norms.

We believe this pattern reflects two factors: 1) The slight slowdown in second-half 2021 spending is shifting into 2022; and 2) CEOs recognize the strategic imperative and urgency of transforming their organizations and the importance of technology as an accelerant.

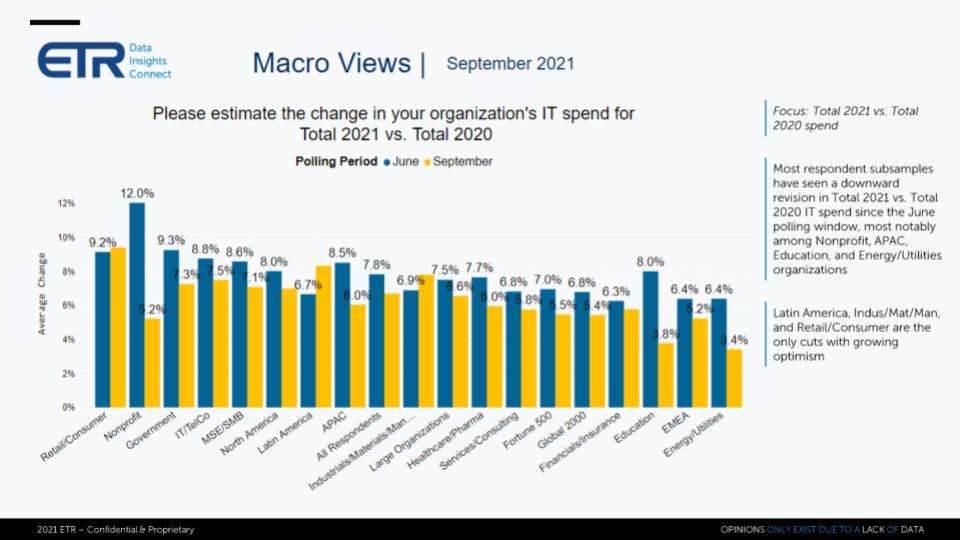

As shown below, only Latin America, Industrial/Materials/Manufacturing and Retail/Consumer show an uptick from previous surveys, with Non-profits, Education, Energy and APAC showing the steepest downward spending revisions in the latest survey.

The chart below shows that generally, the outlook for 2022 spending is robust, with retail, consumer and government spending leading the charge.

Only the historically cautious education sector stands out as noticeably softer than the pack, but even so, its spending outlook is comparable to historical norms. Be careful putting too much emphasis on Latin America, since the Ns are small as noted by ETR in the callouts.

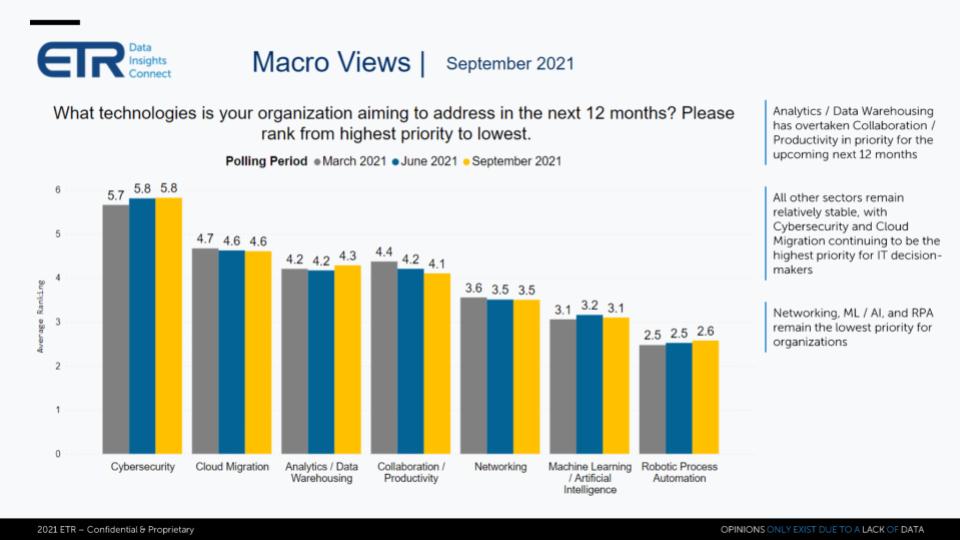

This picture below has been consistent for several quarters. ETR asks respondents to rank their spending priorities. The chart shows the results for the top technology sectors cited. Note: This data only shows the top seven sectors so even though RPA appears down on the list it maintains one of the highest rankings in the survey.

Cybersecurity stands out above the rest, with cloud migration remaining very strong. The data sector – analytics and data warehousing – has overtaken collaboration and productivity as the No. 3 priority. However, collaboration remains strong, as do networking, artificial intelligence and robotic process automation.

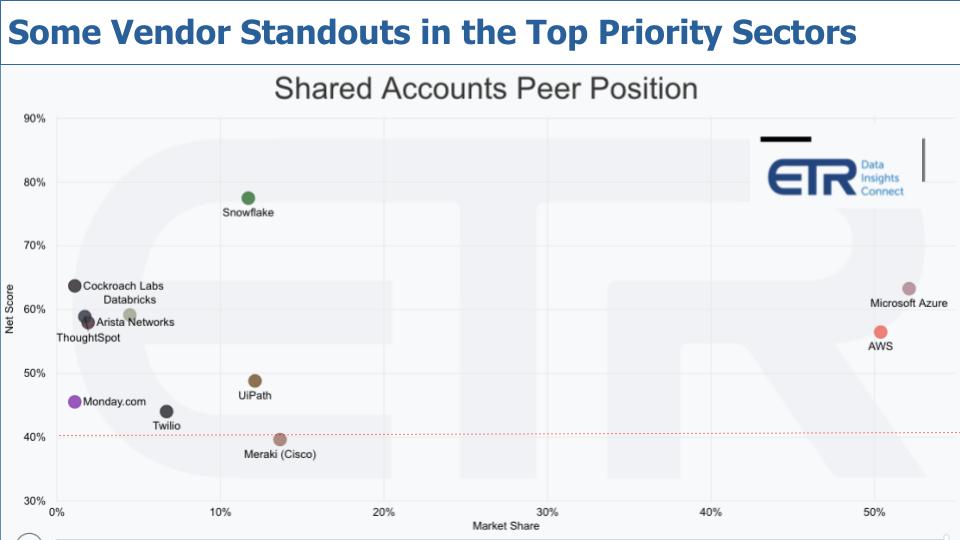

Let’s dig into some of these sectors to see which vendors are showing spending momentum. The chart below shows Net Score or spending velocity on the vertical axis and Market Share or pervasiveness on the horizontal axis. We’ve filtered the data on the seven sectors cited as the top priorities in the survey and have highlighted some of the names that stand out. The red dotted line at 40% on the Y-Axis represents elevated levels in our view.

In addition to the large cloud players, especially Amazon Web Services Inc. and Microsoft Corp., Snowflake Inc. continues to hover at nearly its 80% Net Score level. Some others that we haven’t cited as much that are popping up – either with spending momentum or showing a larger presence in the market within these sectors. For example, Cockroach Labs Inc. and Databricks Inc. are showing momentum. Although their presence on the horizontal axis is not as high, their spending momentum is notable.

ThoughtSpot Inc., the AI specialist, hovers well above the 40% red line. Datadog Inc. also stands out. In networking, Arista Networks Inc. shows momentum and Cisco Systems Inc.-owned Meraki, which has a large presence in the data with well over 100 mentions, is notable at the 40% line. Monday.com Ltd. has also hit our radar in collaboration and Twilio Inc. is also strong.

UiPath Inc. continues to lead in the survey with the highest presence among RPA vendors and an elevated Net Score of nearly 50%.

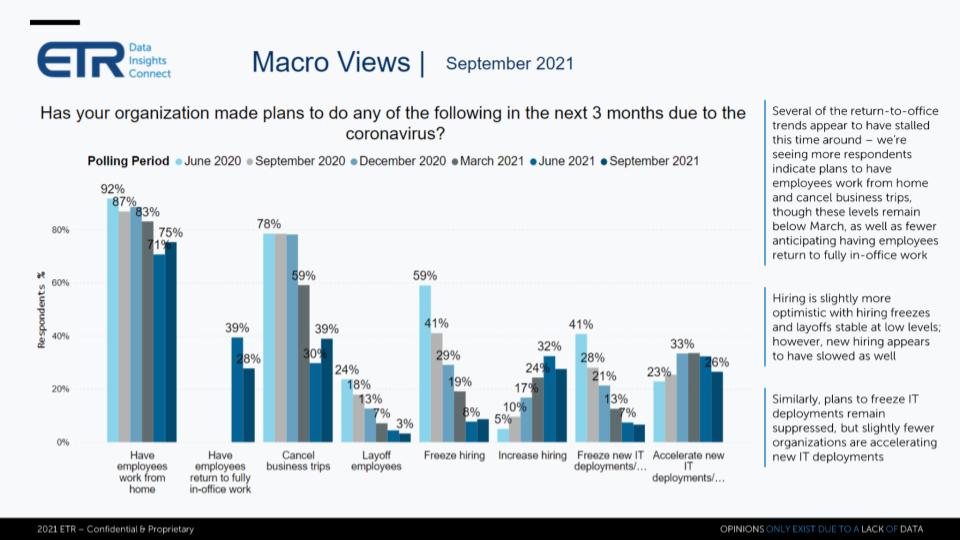

The chart below highlights the return-to-office trends and the actions organizations have taken as a result of COVID. The data show the time series going back to the June 2020 survey.

Let’s start with the percentage of organizations with employees working from home, and you’ll note that’s ticked down since June but is now back up to 75%. And you can see the noticeable drop in the percentage of companies that have employees fully returning to the office. Also, more organizations are cancelling business trips. So these are some of the factors contributing to the slightly more cautious spending outlook for the second half of 2021.

Continuing down the chart, even though layoffs continue to trend downward – which is no surprise given the skills shortage – you do see a slight uptick in hiring freezes and a downtick in new hiring. New IT deployment freezes remain low, but there’s a slight downtick in the acceleration of new IT deployments.

Although these aren’t radical changes, they do reflect the ongoing day-by-day, month-by-month, quarter-by-quarter adjustments we’ve seen companies make throughout the COVID era. And they underscore the need for organizations to be more agile, flexible, resilient and responsive to change. That means modernizing infrastructure and apps, better leveraging data, applying AI and taking care of governance, compliance and security.

Importantly, CIOs expect these priorities to continue for the foreseeable future — at least for the next 15 months.

Interestingly, we see some companies mandating a return to work. For example, some Wall Street firms are demanding workers return fully vaccinated. But tech is a leading example of advocating remote or hybrid work. To wit, Michael Dell’s public posture that he’s wide open to remote and/or hybrid work. And CEO Frank Slootman has moved Snowflake’s executive offices to Bozeman, Montana, reflecting his sentiment that the days of big corporate towers are over. And why not? Productivity is through the roof and the cost savings from working remotely can be enormous.

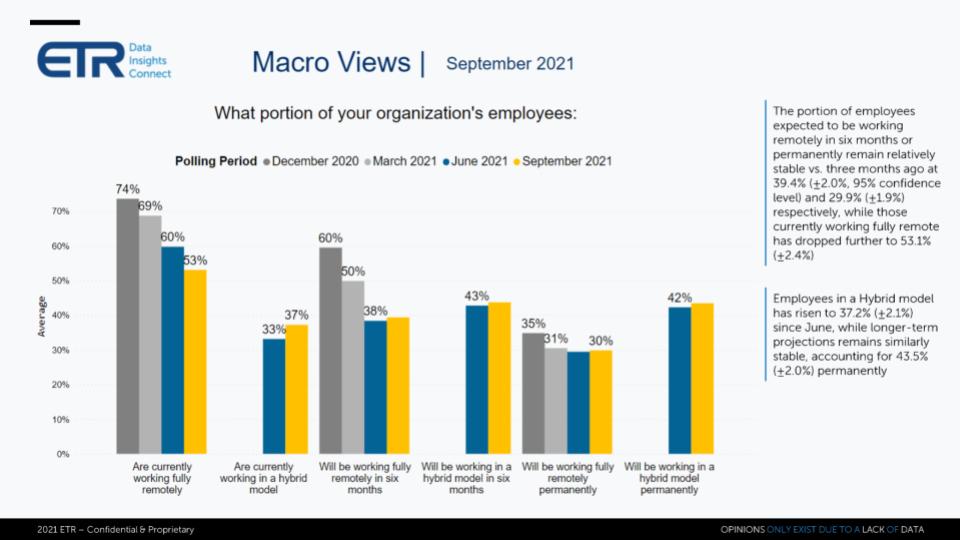

The chart above shows data back to the December 2020 survey. We’ve seen a steady decline in remote work, but it’s still the dominant model at 53% of the workforce. Jump to the third set of bars and organizations expect about 39% of employees to be working remotely in six months. Back to the second set of bars, 37% of employees are currently working in a hybrid model, up from 33% in June and jump to the fourth set, and the expectation is about 44% will be working in a hybrid model in six months.

Organizations expect the percentage of remote workers to settle in at 30%, down from previous highs of 35% last December but up significantly from the historical norm of 15% to 16%. And the expectation, as you see in the last set of bars, is that more than 40% of employees will be working in a hybrid model on a permanent basis.

The world is going hybrid. It’s the future and that requires technology investments to support new ways to work. And that’s one main reason why we see the spending momentum continuing into 2022.

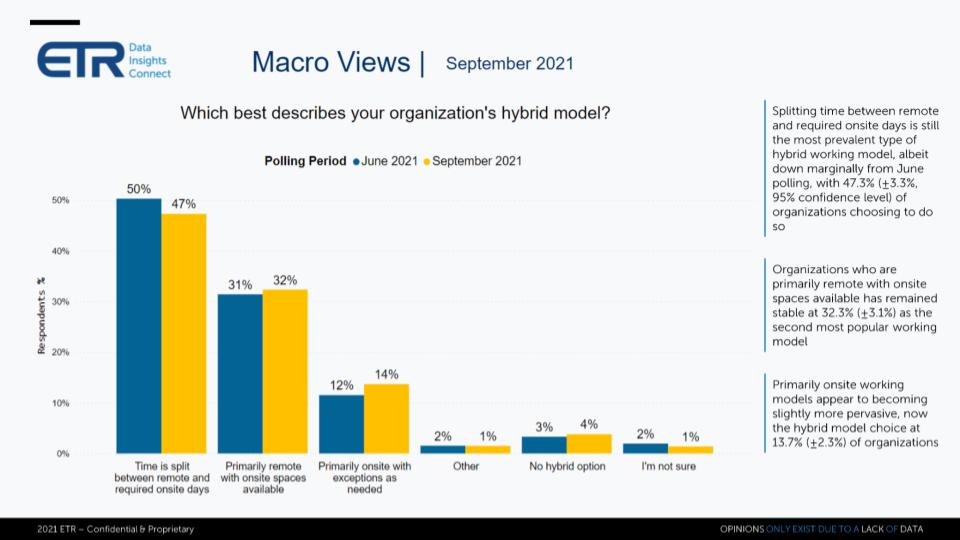

Let’s drill into how are organizations thinking about their hybrid models.

The chart above shows the responses from the June and September surveys when ETR began asking organizations to describe their hybrid approaches.

The dominant model, around 50%, say time will be split between remote and required onsite days. This is where leaders will ask employees to come to the office at designated times for whiteboard sessions, planning meetings and the like. So hybrid is the dominant model.

Then we see a big drop to primarily onsite with exceptions as needed and a low single-digit number of organizations with no hybrid option.

The message is clear. Hybrid is the way forward and IT infrastructure will evolve to support these models. This bodes well for tech spending. It speaks to continued cyber investments, leveraging the cloud for flexible capacity, shoring up on-premises infrastructure, modernizing applications, evolving the network architecture, driving automation and putting data at the core of digital business strategies.

These are the technology approaches that organizations are tapping to deal with the changing dynamics of the pandemic and adapting to new business models. Across the board, technology generally and data specifically has become one of the most important enablers for competitiveness in the coming decade and we expect the momentum to continue until some exogenous factors derail the spending trend.

At the moment, that risk doesn’t appear to be a slowdown in the economic recovery, although we continue to watch uncertainties around interest rates, inflation, tax policy and global economic tensions, especially with China. And as always, we’ll be here to update you as the data changes.

Remember we publish each week on Wikibon and SiliconANGLE. These episodes are all available as podcasts wherever you listen. Email david.vellante@siliconangle.com, DM @dvellante on Twitter and comment on our LinkedIn posts.

Also, check out this ETR Tutorial we created, which explains the spending methodology in more detail. Note: ETR is a separate company from Wikibon and SiliconANGLE. If you would like to cite or republish any of the company’s data, or inquire about its services, please contact ETR at legal@etr.ai.

Here’s the full video analysis:

All statements made regarding companies or securities are strictly beliefs, points of view and opinions held by SiliconANGLE media, Enterprise Technology Research, other guests on theCUBE and guest writers. Such statements are not recommendations by these individuals to buy, sell or hold any security. The content presented does not constitute investment advice and should not be used as the basis for any investment decision. You and only you are responsible for your investment decisions.

Support our mission to keep content open and free by engaging with theCUBE community. Join theCUBE’s Alumni Trust Network, where technology leaders connect, share intelligence and create opportunities.

Founded by tech visionaries John Furrier and Dave Vellante, SiliconANGLE Media has built a dynamic ecosystem of industry-leading digital media brands that reach 15+ million elite tech professionals. Our new proprietary theCUBE AI Video Cloud is breaking ground in audience interaction, leveraging theCUBEai.com neural network to help technology companies make data-driven decisions and stay at the forefront of industry conversations.