CLOUD

CLOUD

CLOUD

CLOUD

CLOUD

This past week, we saw two of the Big Three cloud providers present an update of their respective cloud visions, business progress, announcements and innovations. The content at these events had many overlapping themes, including modern cloud infrastructure at global scale, applying advanced machine intelligence, end-to-end data platforms, the future of work, automation and a taste of the metaverse and Web 3.0. And more.

Despite the striking similarities, the differences between these two cloud platforms, and that of Amazon Web Services Inc., remain significant. Microsoft Corp. is leveraging its massive application software footprint to dominate virtually all markets, and Google LLC doing everything in its power to keep up with the frenetic pace of today’s cloud innovation that was set into motion a decade and a half ago by AWS.

In this Breaking Analysis, we unpack the immense amount of content presented by the chief executives of Microsoft and Google Cloud at Microsoft Ignite and Google Cloud Next. We’ll also quantify with Enterprise Technology Research survey data the relative position of these two cloud giants in four key sectors – cloud infrastructure as a service, business intelligence analytics, data platforms and collaboration software.

Google Cloud Next took place live over 24 hours in six cities around the world with the main gathering in New York City. Microsoft Ignite, normally attended by 30,000 people, had a smaller event in Seattle with a virtual audience around the world. AWS re:Invent, of course, is much different. Yes, there’s a virtual component, but it’s all about a big live audience gathering.

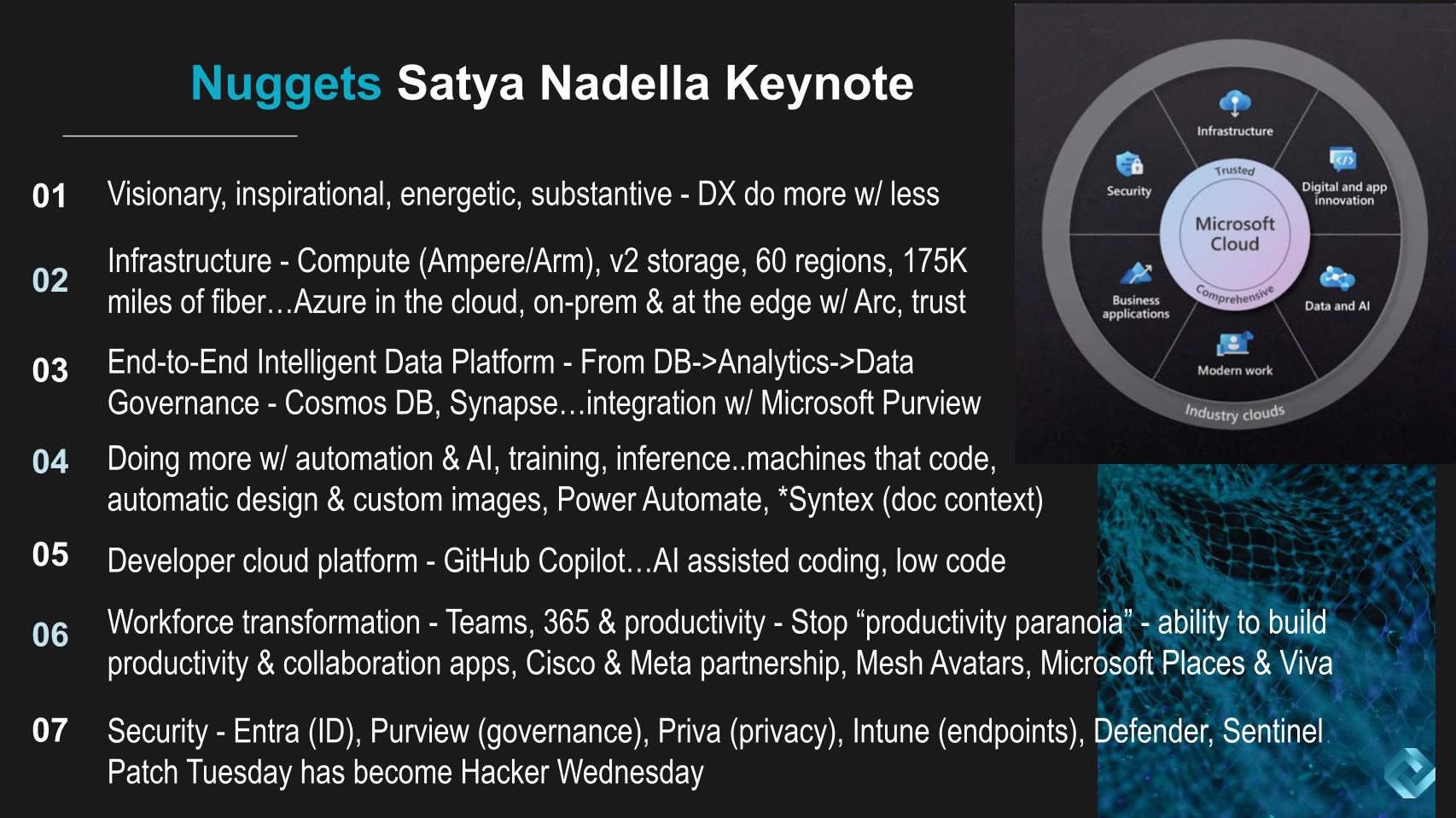

Regardless, Microsoft CEO Satya Nadella’s keynote address was pre-recorded, highly produced and substantive. It was visionary and energetic with a strong message that Azure was a platform to allow customers to build their digital business – doing more with less was a key theme.

Nadella covered a lot of ground — starting with infrastructure from the compute, highlighting a collaboration with Arm-based Ampere Computing LLC processors, new block storage, 60 regions and 175,000 miles of fiber cables around the world. He presented a meaningful multicloud message with Azure Arc to support on-premises and edge workloads and talked about confidential computing at the infrastructure level — a theme we hear from all cloud vendors.

He then went deeper into the end-to-end data platform that Microsoft is building from the core data stores to analytics to governance and the myriad tooling Microsoft offers.

AI was next with a big focus on automation, AI and training. Nadella showed demos of machines coding and debugging code, machines automatically creating designs for creative workers and how Power Automate, Microsoft’s robotic process automation tooling, would combine with Microsoft Syntex (content processing) to understand documents and provide standard ways for organizations to communicate.

There was, of course, a big focus on Azure as a developer cloud platform, with GitHub Copilot as a linchpin using AI to assist coders, and he spoke about low-code/no-code innovations that are coming.

Another giant theme was workforce transformation and how Microsoft is using its heritage in collaboration and productivity software to move beyond “productivity paranoia” – i.e., are remote workers doing their jobs – to a world where collaboration is built into intelligent workflows. Nadella showed a glimpse of the future with AI-powered avatars and partnerships with Meta Platforms Inc. and Cisco Systems Inc. around Microsoft Teams.

And finally there was security, with a bevy of tools from identity, endpoint governance and the like stressing a suite of tools from a single provider – Microsoft.

There are several point we’d like to make on the keynote, including the following:

Despite the outstanding presentation by Nadella, there were a couple of statements that should raise questions.

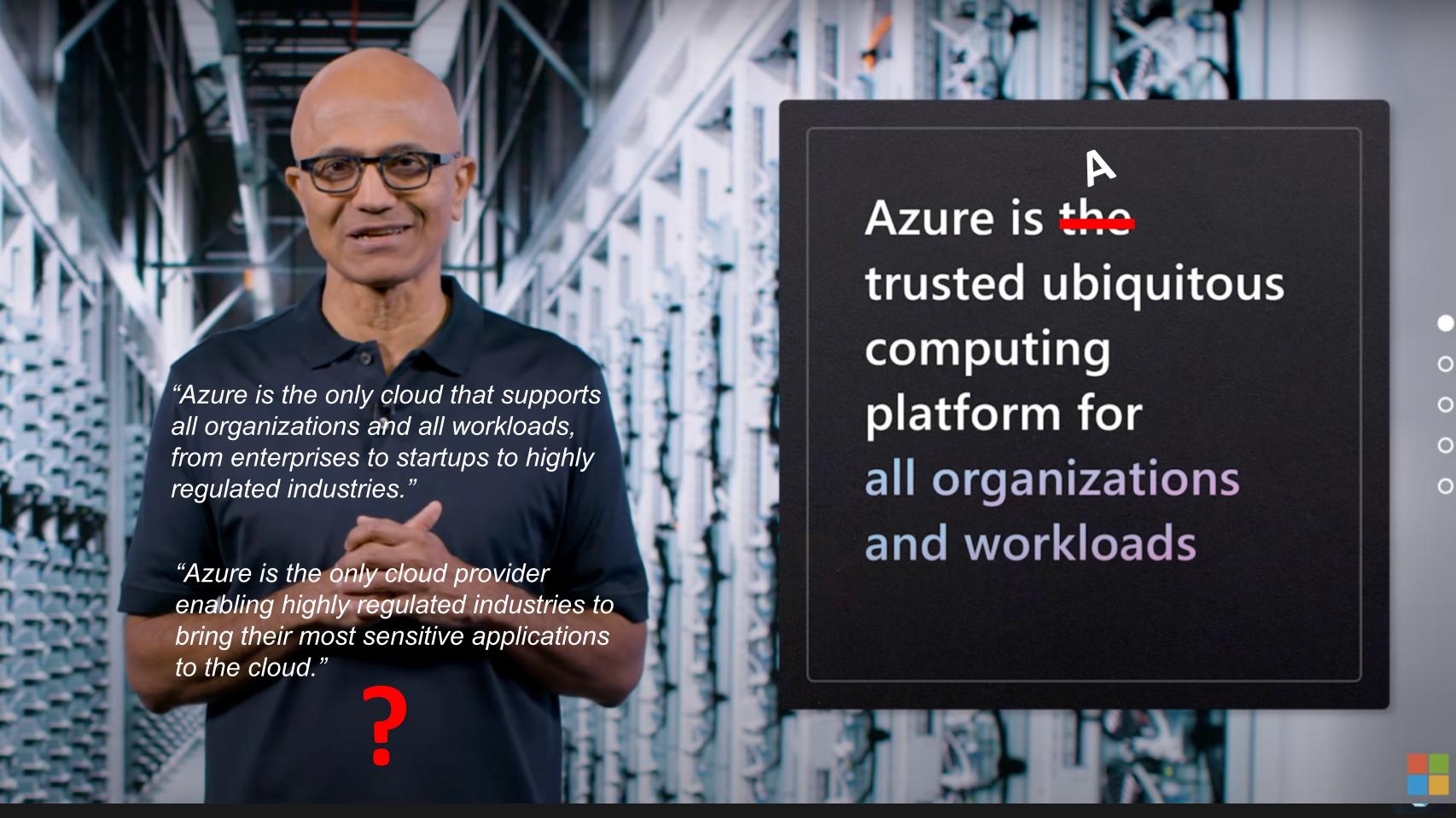

We’ve made a convenient edit to the callout on the right above. We agree Microsoft is trusted and ubiquitous cloud – but don’t quite agree that is “the” one and only. Nadella made at least two other statements that we felt warranted a challenge:

Azure is the only cloud that supports all organizations and all workloads from enterprises to startups to highly regulated industries.

And…

Azure is the only cloud provider enabling highly regulated industries to bring their most sensitive applications to the cloud.

We reached out to CUBE collaborator Sarbjeet Johal about these statements. He as well was surprised by this claim. He pointed out that AWS has supports more certifications than Microsoft and we would think it has a reasonable case to dispute these claims. As well, on claiming that Azure is the only cloud provider enabling highly regulated industries to bring their most sensitive applications to the cloud, we think reasonable people can debate whether AWS is there yet but very clearly Oracle Corp. and IBM Corp. would have something to say about that statement.

Perhaps Nadella doesn’t consider Oracle and IBM as clouds. We would agree they’re not in the class of the Big Three hyperscale clouds, but they are clouds in our view.

Nadella also made the claim that the Edge browser, “no questions asked,” is the best browser for business. We can see some people having questions about that. Like – isn’t Edge based on Chrome?

So we just have to question these statements and challenge Microsoft to defend them because to us it’s a bit of BS and makes one wonder what else in his excellent keynote was real and what was hyperbole.

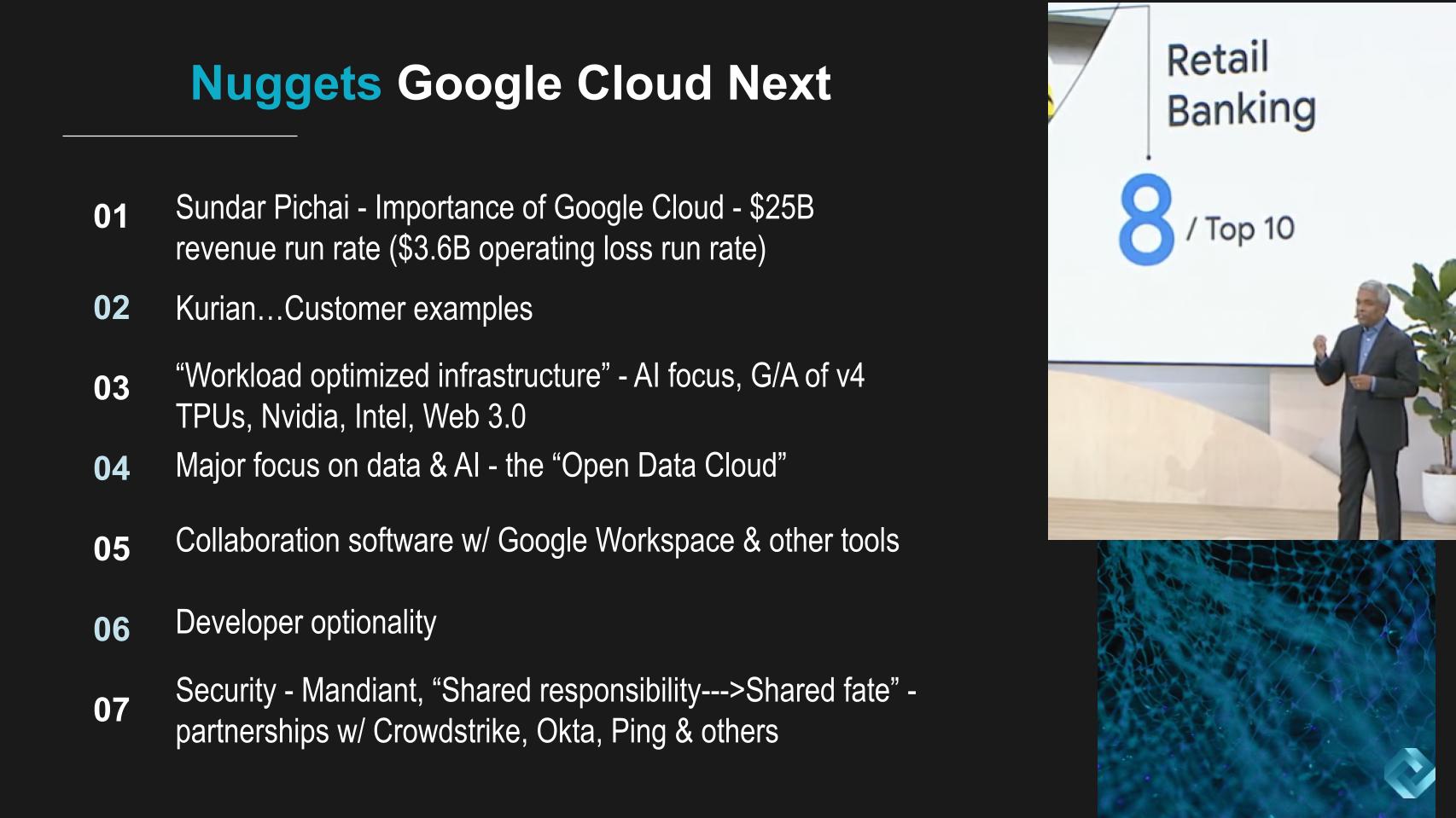

The Google keynote started with CEO Sundar Pichai doing a remote session stressing the importance of Google Cloud. He mentioned that Google Cloud, based on its third-quarter earnings was on a $25 billion annual run rate. Pichai didn’t mention that it’s also on a $3.6 billion annual operating loss run rate based on its first-half performance. And we’ll dig into this issue more a bit later in this post.

He also stressed that the investments that Google has made to support its core business such as its global network of 22 subsea cables, YouTube innovations, BigQuery to support search, its threat analysis and AI, all leveraged by Google Cloud Platform.

This is all true. Google has awesome tech. Pichai’s remarks were forward-thinking and laid out a vision of the future but he didn’t address in our view today’s challenges to the degree that Microsoft did – and we expect AWS will at re:Invent this year.

Google Cloud CEO Thomas Kurian then took over and did a very good job of highlighting customers. Nine of the 10 top media firms use Google Cloud; eight out of the top 10 manufacturers; nine of the top 10 retailers; same for telecom, same for healthcare, and eight of the top 10 retail banks. Kurian and Pichai specifically referenced Avery Dennison, Groupe Renault, H&M, Johns Hopkins, Prudential, Mina Bank, ANZ Bank and many others during the session. And they gave many examples of customers not just utilizing Google’s productivity tools but substantive work in data, AI and other services from GCP.

Like Microsoft, Google talked about infrastructure – Kurian announced the general availability of the latest tensor processing units for training… and emphasized compute optionality, mentioning partnerships with Intel Corp. and Nvidia Corp. He also talked about the buildout of cloud regions and the requisite storage services.

Kurian also stressed how new workloads were emerging that required new infrastructure. Again, as we’ve extensively discussed in Breaking Analysis, in our view, when it comes to compute, AWS via its Annapurna acquisition is well ahead of the pack with regard to custom silicon. But all three companies are investing in that area and heavily in infrastructure, which is great news for customers and the ecosystem.

Data and AI go hand-in-hand and there was no shortage of data talk. Google didn’t mention Snowflake Inc. (or Databricks Inc.), but it did mention Google’s “Open Data Cloud.” Now maybe Google has used that term before but Snowflake has been marketing the data cloud concept for a couple of years now, so that struck me as a shot across the bow to a partner and competitor.

And BigQuery is a centerpiece of Google’s data strategy. Kurian spoke about how they can take any data from any source in any format from any cloud provider with BigQuery Omni, aggregate it and understand it. And with support of Apache Iceberg, Delta and Hudi (coming soon), there’s an initiative called the Data Cloud Alliance. So without specifically mentioning Snowflake or Databricks, Kurian co-opted a lot of messaging from these two leading data players.

Such is life in tech.

Kurian also talked about Google Workspace and how it’s now at 8 million users, up from 6 million just two years ago. There was also a lot of discussion on developer optionality and several details on tools supported and the open mantra of Google.

Finally on security, Google brought out Kevin Mandia, a CUBE alum who is CEO of Mandiant, a leading security services provider and consultancy. Google acquired Mandiant for about $5.3 billion recently. They talked about moving from shared responsibility to shared fate. This appears to be a clear shot across AWS’ bow. It’s unclear that Google will pay the same penalty if a customer doesn’t live up to its shared responsibility, but we can probably assume the customer will bear the brunt of the pain.

Nonetheless, Mandiant is interesting because it is a services play. And Google has stated that it’s not a services company and it’s giving partners and the channel plenty of room to play, so we’ll see what it does with Mandiant. Regardless, Mandiant brings a very strong enterprise capability in the single most important area – security.

Importantly, unlike Microsoft, Google is not competing with leaders such as Okta and CrowdStrike. Rather, it’s partnering aggressively with them and that’s a differentiator from Microsoft. AWS is also heavily leaning into partnering with the security ecosystem.

Let’s get into the survey data and see how Microsoft and Google are positioned in four key markets – IaaS, BI/analytics, database/data platforms and collaboration software.

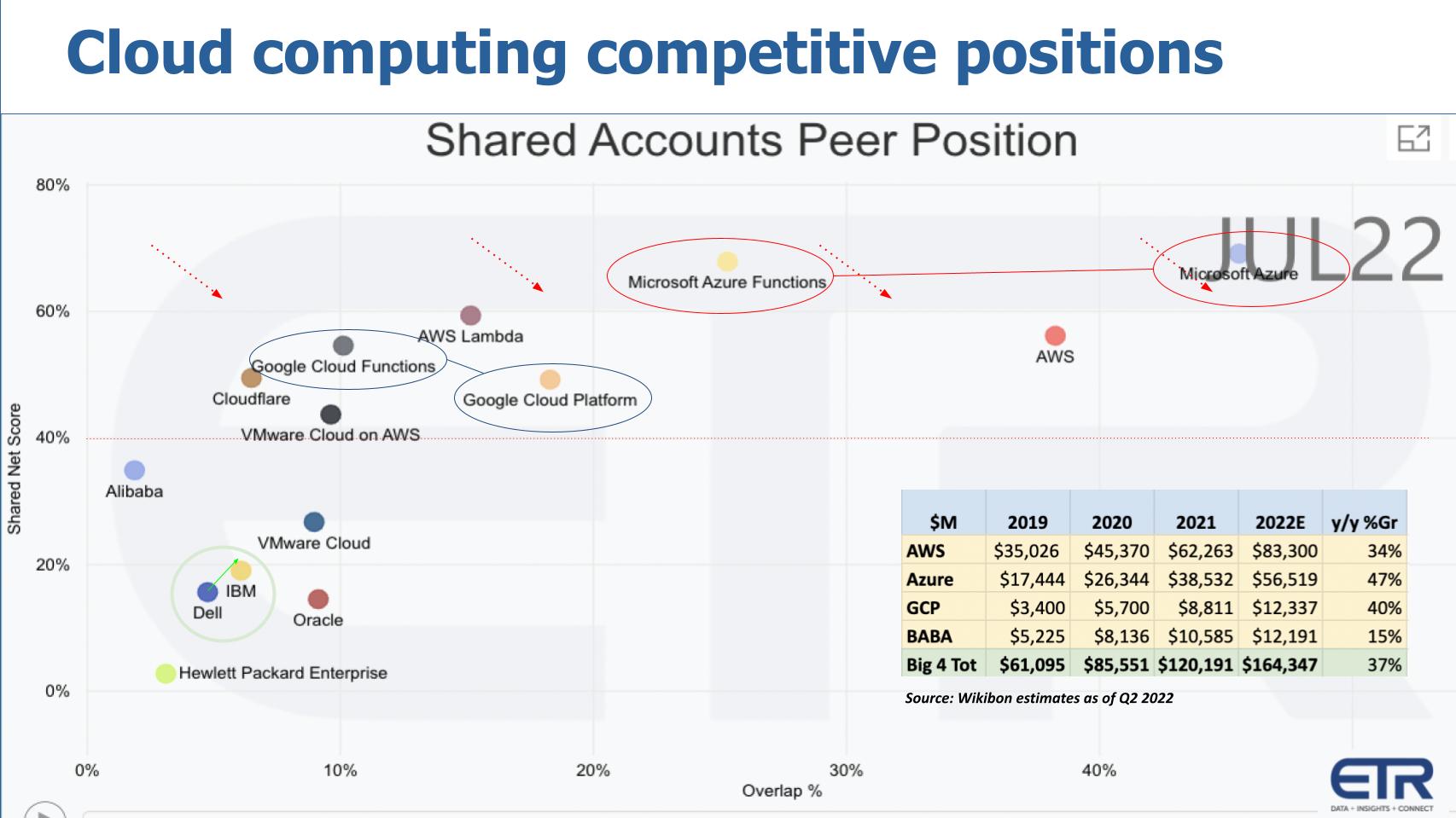

ETR is just about to release its October survey, so we can’t share that data yet. We can only show July data, but we’ve given you some directional hints at what’s coming. The chart above shows Net Score or spending momentum on the vertical axis and Overlap or presence in the data – i.e., how pervasive the platform is – on the horizontal plane. And we’ve inserted the Wikibon estimates of IaaS revenue in the able to the bottom right.

A couple of points to help you navigate this busy data chart.

So the survey data generally confirms what we know – that AWS and Azure have a massive lead and strong momentum in the market. But the untold story is below the line. Unlike Google Cloud, which is on pace to lose well over $3 billion on an operating basis this year, AWS’ operating profit is around $20 billion annually. Microsoft’s Intelligent Cloud generated more than $30 billion in operating income last fiscal year.

Let that sink in for a moment.

Google has traction in the market with key customers. Kurian gave some nice proof points in his keynote presentation… more than enough to convince the skeptics that GCP is real. But the data above underscores the lead Microsoft and AWS have on Google in cloud. And as the data below shows, the two leaders are executing noticeably better on the customer front.

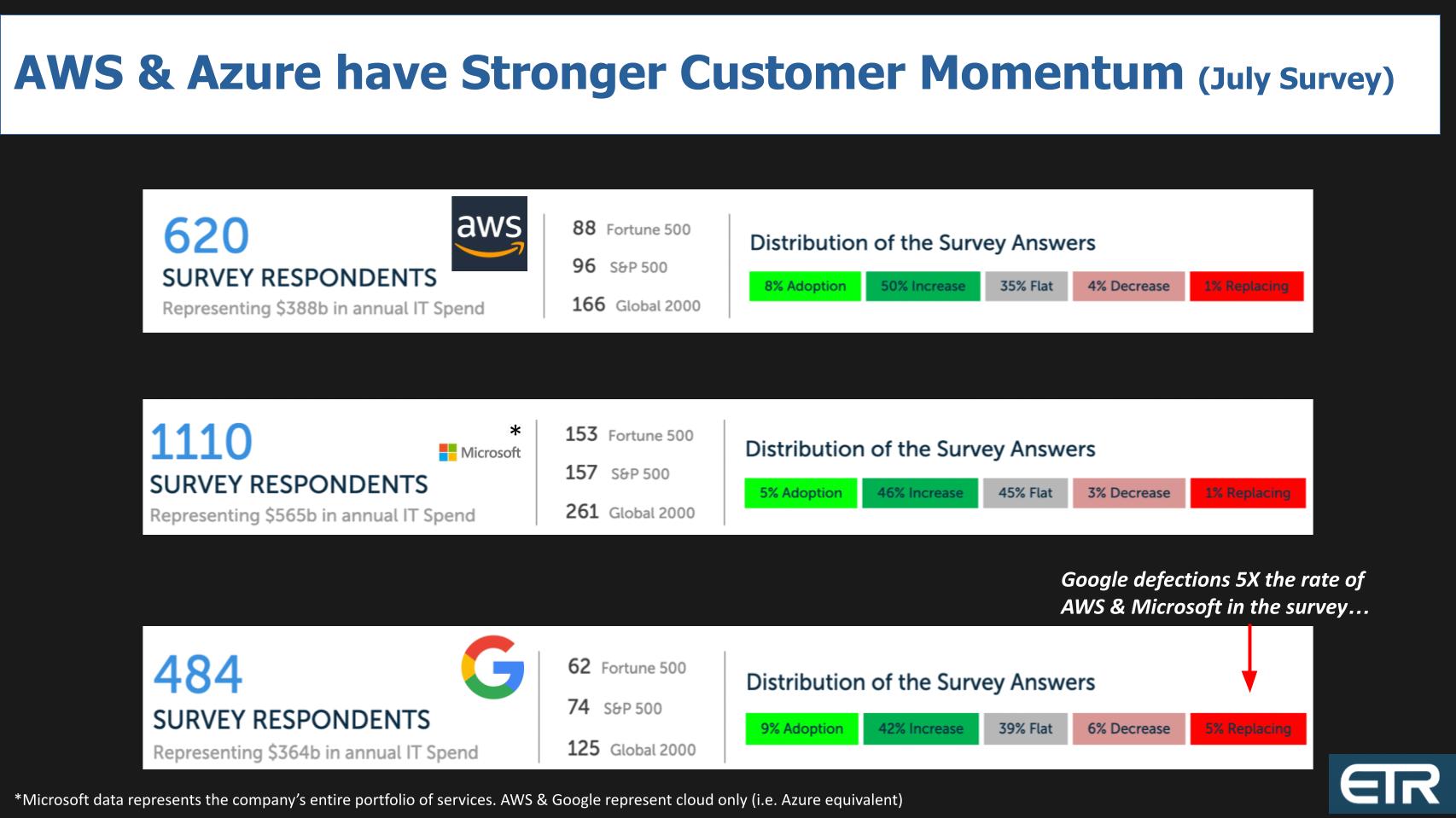

The above graphic shows a breakdown of ETR’s proprietary Net Score methodology. It asks customers if they’re adopting the platform new (lime green), spending more than 6% (forest green), flat spend (gray), spending down 6% or worse (pinkish color) or replacing the platform (bright red). Subtract reds from greens, and you get a Net Score.

One impressive caveat is the Microsoft data reflects its entire Microsoft portfolio, meaning it includes the company’s legacy platforms. The other note is this data is from the July survey – we’ll have an update for you once ETR releases the October results.

But we’re talking meaningful samples of 620 for AWS, more than 1,000 for Microsoft, and more than 450 respondents for Google.

The real tell is replacements. There is virtually no churn for AWS and Microsoft. Google’s churn is five times those two in the survey. Now, 5% churn is not high, but you’d like to see four things for Google given its smaller size: 1) less churn; 2) much, much higher adoption rates; 3) a higher percentage of spending more (the forest green); and 4) a lower percentage of spending less.

None of these four conditions is really in play for Google. GCP is still not growing fast enough and doesn’t have nearly the traction of the two leaders, according to the data.

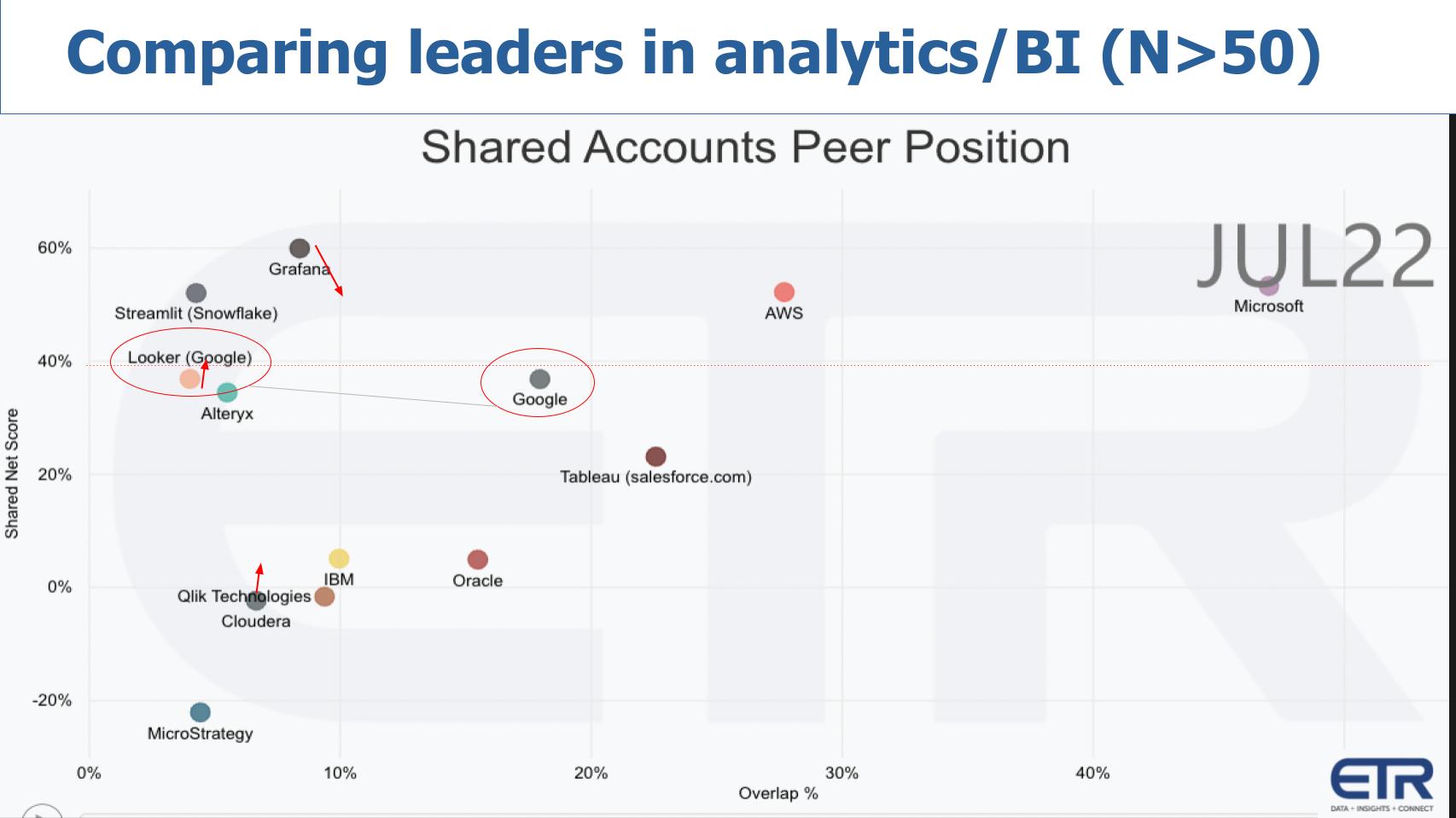

Above we have the same XY dimensions (spending momentum against market presence). Again, Microsoft is dominating the picture, with AWS very strong on both axes. Tableau is popular on the X axis and respectable on the vertical axis. And Google, with Looker and its other platforms, is also respectable. But it has some work to do in this area as well to catch up to the leaders.

Notice Streamlit, the recent Snowflake acquisition, is strong on the vertical axis and will likely move to the right over time. Grafana Labs Inc. is prominent on the Y axis, but a glimpse at the most recent data shows it slightly declining while Looker improves a bit — as does Cloudera Inc., which will move up slightly.

Microsoft’s performance just blows you away, doesn’t it?

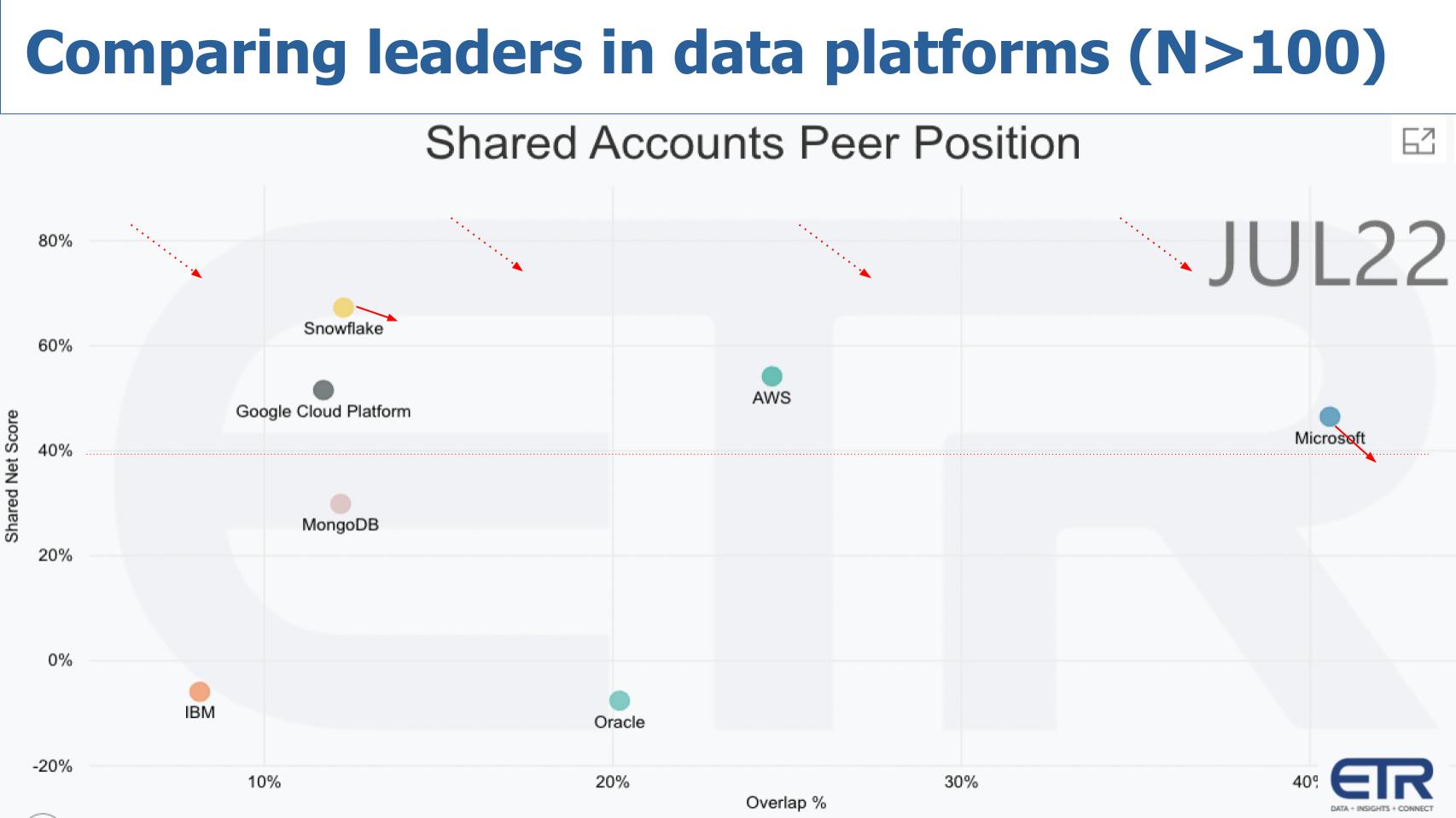

Same dimensions for the above graphic (spending velocity versus market presence) but this time for database and data warehouse. Snowflake as usual takes the top spot on the vertical axis with, again, Microsoft and AWS dominant in the market – as is Oracle albeit with less spending velocity. Google is well behind on the X axis but solidly above the 40% mark on the vertical. Note that virtually all platforms will see pressure in the next survey from the macro environment and Microsoft might even dip below the 40% line for the first time in a while.

Snowflake appears more steady than the pack but will also likely see some macro pressures.

Lastly, let’s look at the collaboration and productivity software market. This is such an important area for both Microsoft and Google.

Same dimensions above (spending velocity versus market presence). Just look at Microsoft with 365 and Teams. The company’s platforms are ubiquitous. And that drives captive IaaS consumption. We’ve highlighted Google. It’s in the pack and certainly has a nice base with 174 N, which we can tell you is rising. But given the investment and the tech behind it and all the AI and Google’s resources, you’d really like to see it above the 40% line given the importance of this space to Google’s success and the degree to which it’s emphasized in its pitches.

And look, this brings up something that we’ve talked about before on Breaking Analysis. Google doesn’t have a tech problem. This is a go-to-market and marketing challenge Google faces. It’s up against two go-to-market champs in Microsoft and AWS and Google doesn’t have an enterprise sales culture. It’s trying. It’s making progress. But it’s like the racehorse that has all the potential in the world but it’s just missing some key ingredient to put it over the top. It’s in the money but hasn’t taken the winner’s purse in any enterprise Grade I races yet.

Customers and partners should be thrilled that both Microsoft and Google along with AWS are spending so much money on capital expenditure innovation and building out global platforms. This is a gift to the industry and we should be thankful frankly because it’s good for business, competitiveness and the future of innovation.

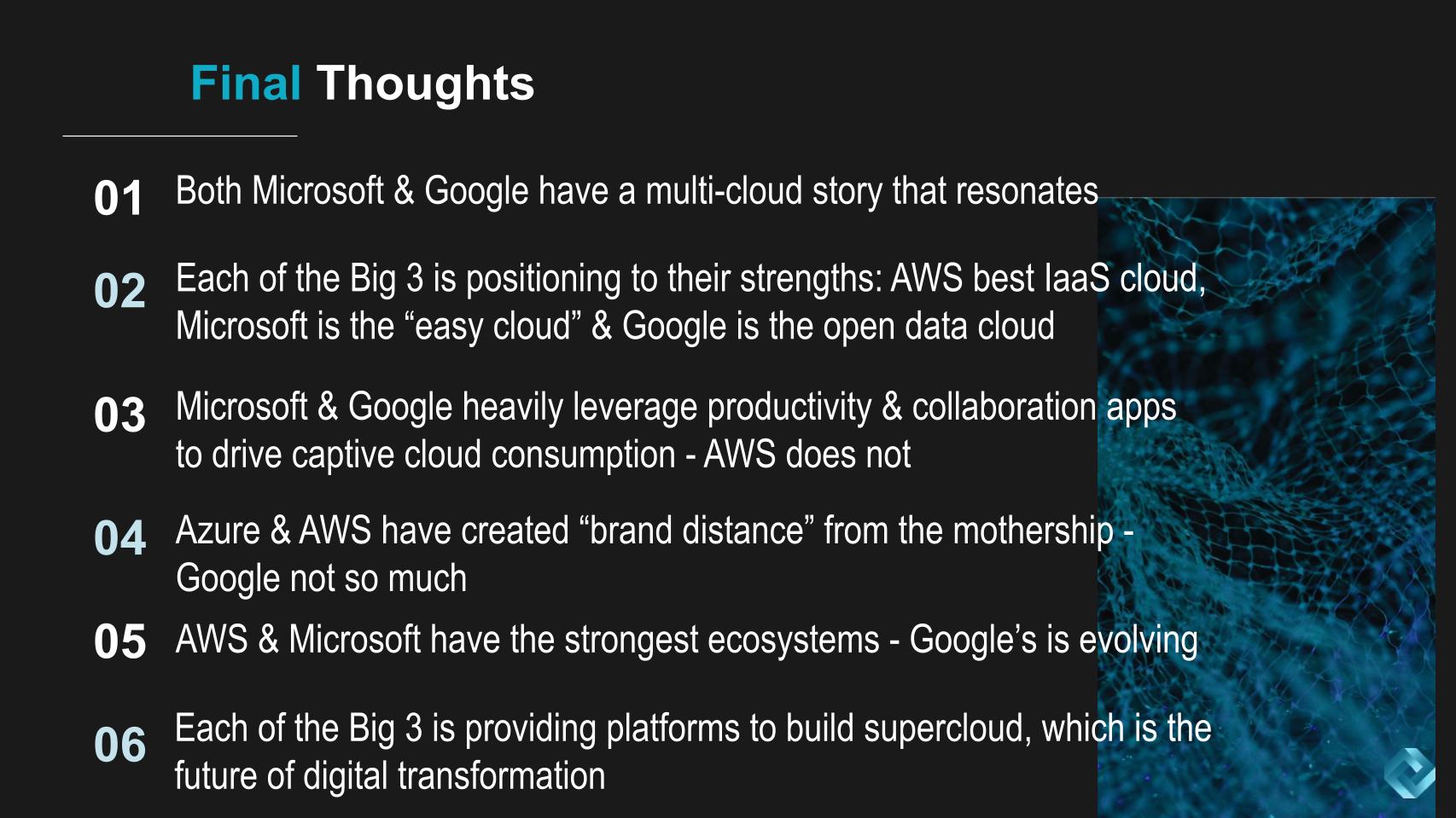

Now we didn’t talk much about multicloud, but both Microsoft and Google have a story that resonates with customers — unlike AWS at this time. But never say never when it comes to AWS – it will surprise you.

One of the other things Sarbjeet Johal and John Furrier discussed is that each of the Big Three is positioning to their respective strengths. AWS is the best IaaS, Microsoft is building out the “We make it easy for you” cloud and Google is trying to be the open data cloud – with its open-source chops and excellent tech. That posture by Google puts added pressure on Snowflake, doesn’t it?

Kurian made some comments according to CRN – something to the effect that we’re the only company that can do the data cloud thing across clouds – which, again, if we’re being honest, is not accurate. We haven’t clarified the statements with Google and often things get misquoted. But there’s little question that, as AWS has done in the past with Redshift, Google is taking a page out of Snowflake. And Databricks as well.

A big difference in the Big Three is AWS doesn’t have this big up-the-stack collaboration software play. Both Microsoft and Google do, and that drives captive IaaS consumption. AWS obviously has it in database, but independent software vendors that compete with Microsoft and Google should have a greater affinity to AWS, one would think, for competitive reasons. Same thing could be said in security.

One other thing Sarbjeet mentioned that we’ll call out here: AWS specifically but also Microsoft with Azure have successfully created brand distance, as he called it — AWS from Amazon retail and Azure with its own identity. It seems Google still struggles to do so. Now maybe that’s by design, but for enterprise customers, there’s still some potential confusion with Google, what its intentions really are, how long it will continue to lose money and invest.

We didn’t talk much about ecosystem, but it’s vital and Google has some work to do relative to the leaders. Which leads us to the supercloud. The ecosystem and end customers are now in a position this decade to digitally transform and build out their own clouds. Not by building data centers and installing racks of servers — rather to build value on top of the hyperscaler gift that’s been presented.

And that is a megatrend that we’re watching closely in theCUBE community. While there’s debate about the supercloud name and so forth, there’s little question in our minds that the next decade of cloud won’t be like the last, and that building value on top of hyperscale infrastructure is fundamental to digital transformations.

Thanks to Alex Myerson and Ken Shiffman, who are on production, podcasts and media workflows for Breaking Analysis. Special thanks to Kristen Martin and Cheryl Knight, who help us keep our community informed and get the word out, and to Rob Hof, our editor in chief at SiliconANGLE.

Remember we publish each week on Wikibon and SiliconANGLE. These episodes are all available as podcasts wherever you listen.

Email david.vellante@siliconangle.com, DM @dvellante on Twitter and comment on our LinkedIn posts.

Also, check out this ETR Tutorial we created, which explains the spending methodology in more detail. Note: ETR is a separate company from Wikibon and SiliconANGLE. If you would like to cite or republish any of the company’s data, or inquire about its services, please contact ETR at legal@etr.ai.

Here’s the full video analysis:

All statements made regarding companies or securities are strictly beliefs, points of view and opinions held by SiliconANGLE Media, Enterprise Technology Research, other guests on theCUBE and guest writers. Such statements are not recommendations by these individuals to buy, sell or hold any security. The content presented does not constitute investment advice and should not be used as the basis for any investment decision. You and only you are responsible for your investment decisions.

Disclosure: Many of the companies cited in Breaking Analysis are sponsors of theCUBE and/or clients of Wikibon. None of these firms or other companies have any editorial control over or advanced viewing of what’s published in Breaking Analysis.

Support our mission to keep content open and free by engaging with theCUBE community. Join theCUBE’s Alumni Trust Network, where technology leaders connect, share intelligence and create opportunities.

Founded by tech visionaries John Furrier and Dave Vellante, SiliconANGLE Media has built a dynamic ecosystem of industry-leading digital media brands that reach 15+ million elite tech professionals. Our new proprietary theCUBE AI Video Cloud is breaking ground in audience interaction, leveraging theCUBEai.com neural network to help technology companies make data-driven decisions and stay at the forefront of industry conversations.