CLOUD

CLOUD

CLOUD

CLOUD

CLOUD

The unraveling of market enthusiasm continued in the fourth quarter of 2022 with the earnings reports from the U.S. hyperscaler cloud providers now all in.

As we said earlier this year, even the cloud is not immune from the macro headwinds and the cracks in the armor we saw from the data we shared last summer are playing out into 2023. For the most part, actual results are disappointing beyond expectations, including our own. It turns out that our estimates for the big three hyperscaler revenue missed by $1.2 billion or 2.7% lower than we had forecast from our most recent November estimates. We expect decelerating growth rates for the hyperscalers will continue through the summer of 2023 and won’t abate until comparisons get easier.

In this Breaking Analysis, we share our view of what’s happening in cloud markets – not just for the hyperscalers but other firms that have hitched a ride on the cloud. And we’ll share new Enterprise Technology Research data that shows why these trends are playing out, tactics customers are employing to deal with their cost challenges, and how long the pain is likely to last.

The cloud has been a significant catalyst for companies such as Snowflake Inc., Databricks Inc., Workday Inc., Salesforce Inc., MongoDB Inc. with Atlas, and IBM Corp.’s Red Hat with OpenShift. However, the elasticity of cloud technology also means that what goes up can come down quickly.

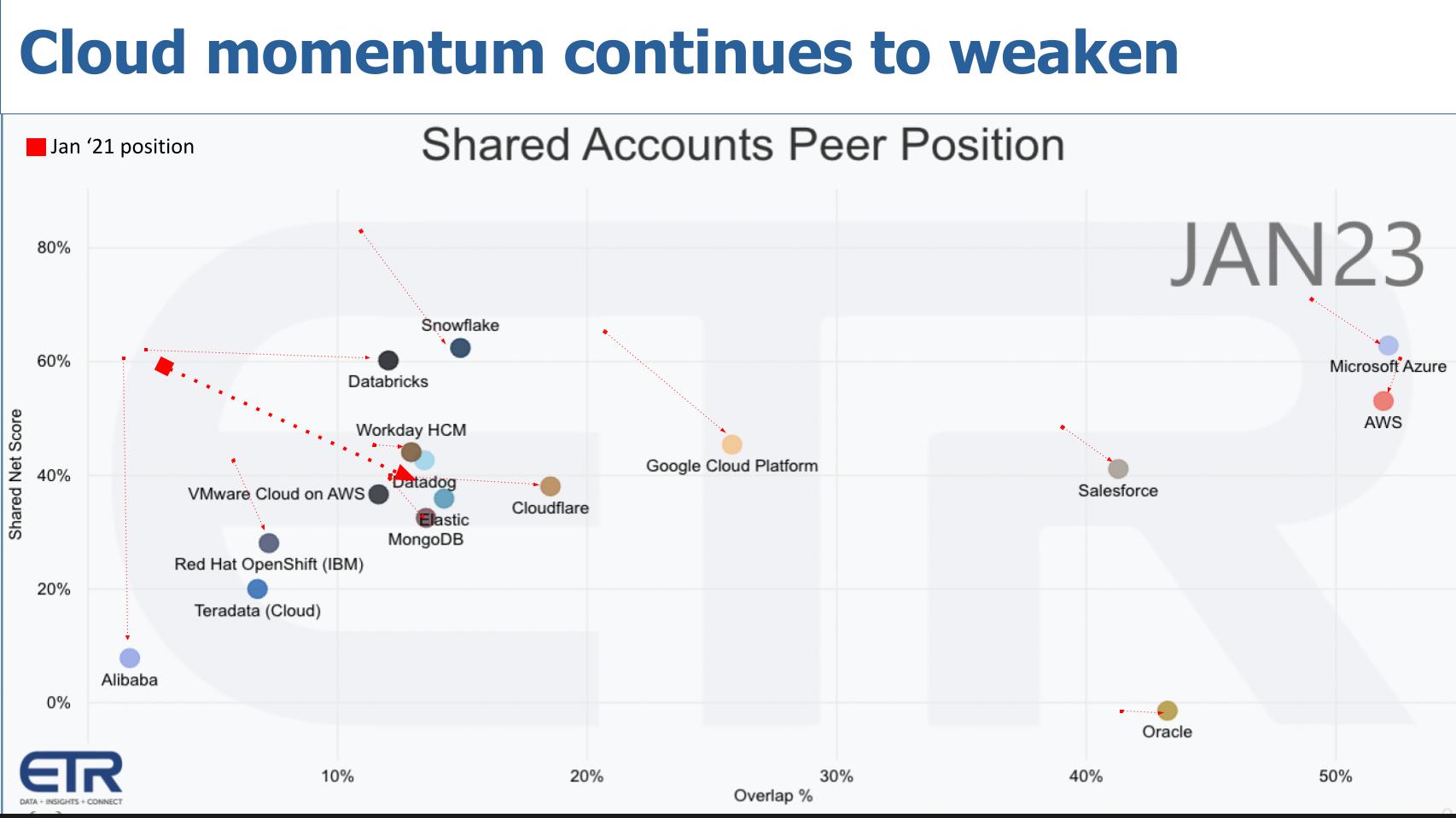

Above is an XY chart from the latest ETR survey of information technology decision makers or ITDMs. N=1,525.

The graphic shows the spending momentum (Net Score) on the vertical axis and market presence (Pervasion) on the horizontal plane. This data shows several companies from the January 2023 survey. The red dotted lines indicate the positions of these companies and the subsequent directional movement from back in January 2021.

The data reveals that Amazon Web Services Inc. and Microsoft Corp.’s Azure continue to widen their lead over Google Cloud Platform, with their infrastructure-as-a-service revenues five to six times higher than GCP. Despite GCP’s efforts to gain ground, its Net Score has fallen below that of AWS and Azure. Google Cloud’s losses continue and came in flat at around $3 billion last year– although they were cut to a $2 billion run rate in the fourth quarter.

AWS has held its position and continues to perform well, along with Microsoft, which benefits from the inclusion of software as a service in its cloud numbers. However, most of the companies on the chart have seen a decrease in spending momentum.

Snowflake and Databricks are worth calling out. While Snowflake’s market presence has continued to grow, its customers have the option to dial down consumption, similar to other cloud companies. On the other hand, Databricks, a private company, has gained significant market presence and has maintained the Net Score it had back in 2021.

Workday and Salesforce have performed relatively well. We’re showing Workday’s flagship human capital management offering, which has held ground. Salesforce has lost spending momentum, but its presence on the X axis continues to grow, underscoring the sticky nature of both platforms.

MongoDB at one point conveyed to investors that it was less exposed to discretionary spending than analytics platforms such as Snowflake. Generally both platforms have held up fairly well, with Snowflake showing greater spending velocity in the survey and a larger market presence.

Datadog Inc. has made significant progress on the X axis, but its Net Score has declined dramatically.

Red Hat OpenShift momentum in the survey has dropped, but IBM’s recent announcement that OpenShift hit $1 billion annual recurring revenue suggests that it is being bundled into IBM consulting’s modernization projects.

Cloudflare Inc.’s Net Score has remained strong since 2021, and it has gained significant market presence.

Oracle Corp., despite having a lower Net Score, continues to grow in the market and clearly has thrived from a profit perspective.

The bottom line is, overall, the data suggests a downward trend in the market that will likely continue through the summer.

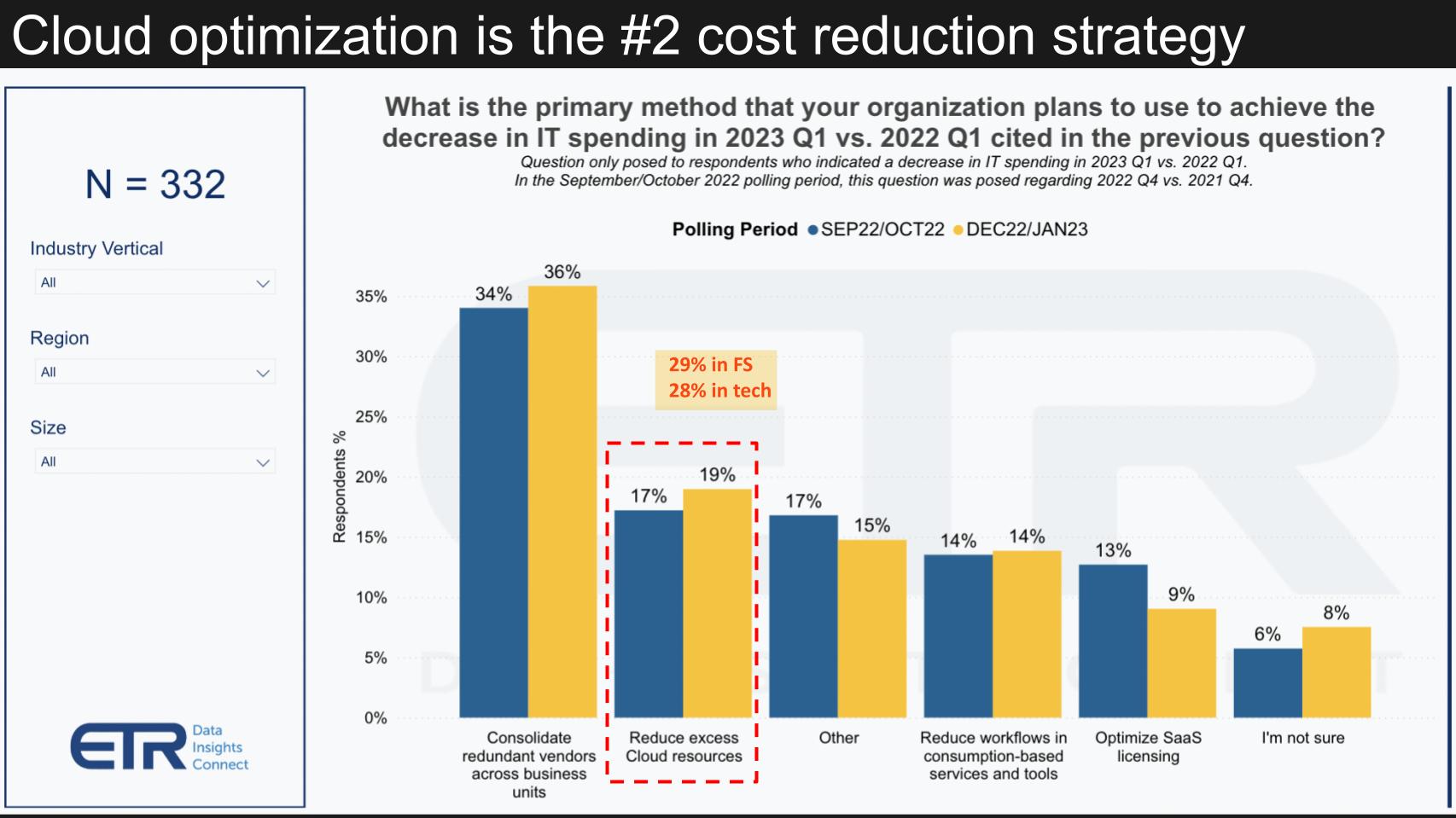

Above is a graphic from the most recent ETR drill-down asking customers that said they’re cutting spending what technique they’re using to do so. As we’ve reported, consolidating redundant vendors is by far the most cited approach. But two key points we want to make: 1) Reducing excess cloud resources is the second most cited technique; and 2) Reducing cloud costs jumps to 29% and 28% in financial services and tech/telco, respectively. In these two sectors, optimizing cloud costs is a much closer second in those two bellwether industries.

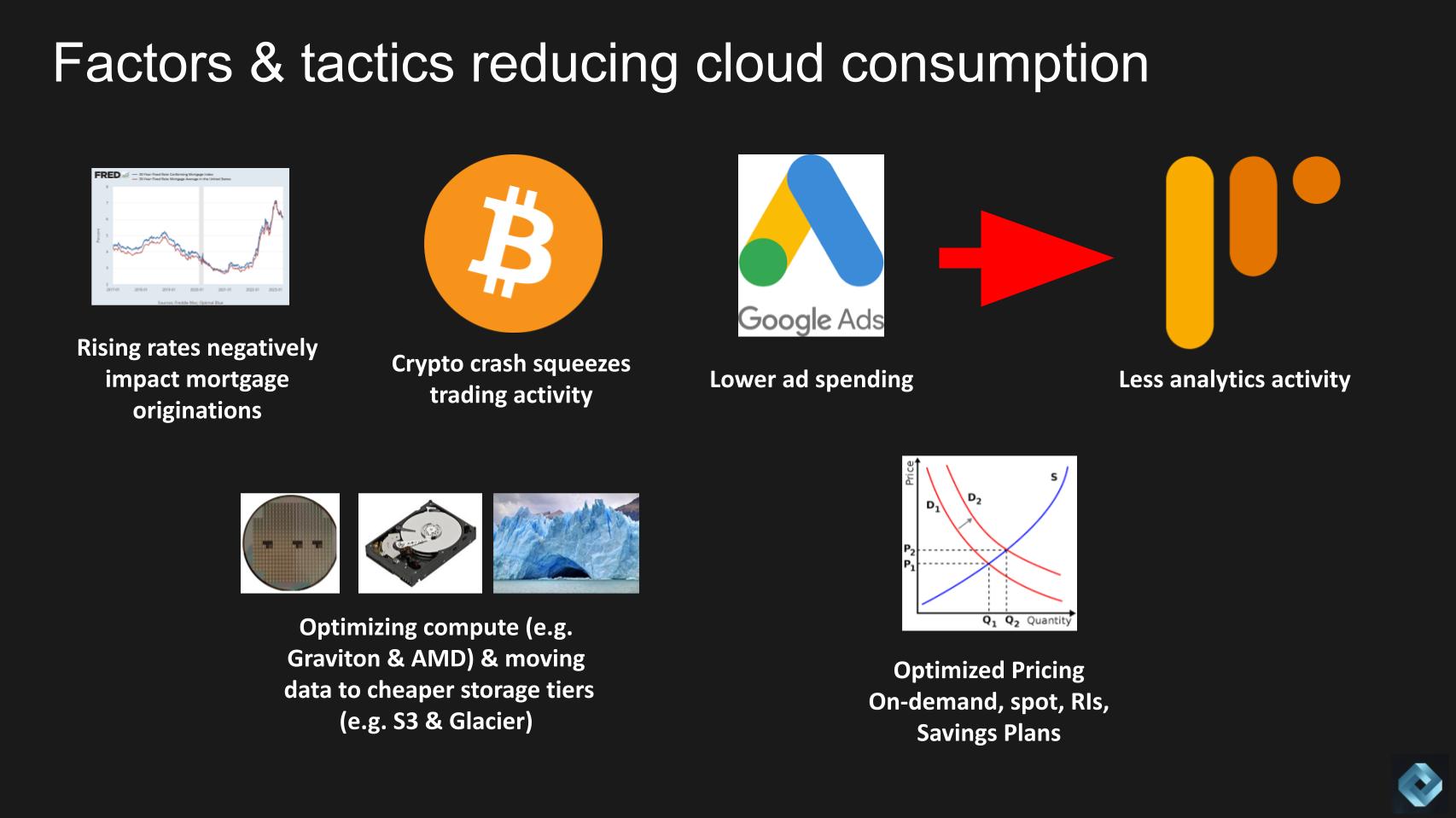

Cloud is great because you can dial it up quickly. But it’s also easy to spin down resources to cut costs. We’ve identified six factors that customers tell us are affecting their cloud consumption. There may be more, and we’d love to hear others, but these are all fairly prominent based on our research.

All of this means less cloud resource consumption. In the days when everything was on-premises, chief financial officers would freeze capital spending and IT pros would have to try and do more with less, and often that meant a lot of manual tasks that took a longer period of time to hit the bottom line. With the cloud it’s much easier to move things around – it still takes some effort but it’s dramatically simpler to do so.

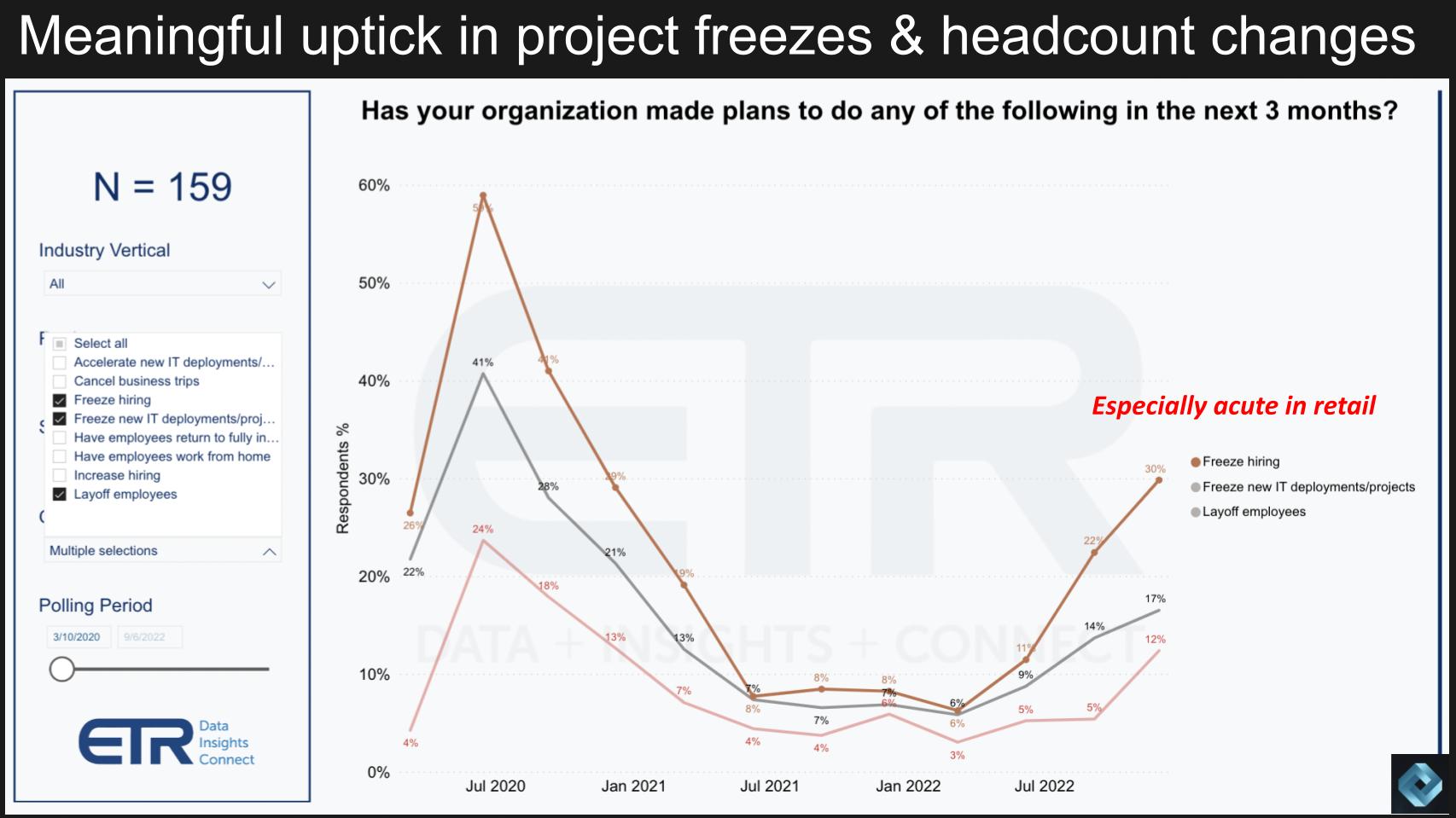

The graphic below shows data from a recent ETR survey with 159 respondents and you can see the meaningful uptick in hiring freezes, freezing new IT deployments and layoffs. As we’ve reported, this has been trending up since earlier this year.

Note the callout. This trend is especially prominent in retail sectors. That’s a bit of a concern because oftentimes consumer spending helps the economy make a softer landing out of a pullback, so this is a potential canary in the coal mine. If retail firms are pulling back, it’s because consumers aren’t spending as much and that could trigger a negative cycle.

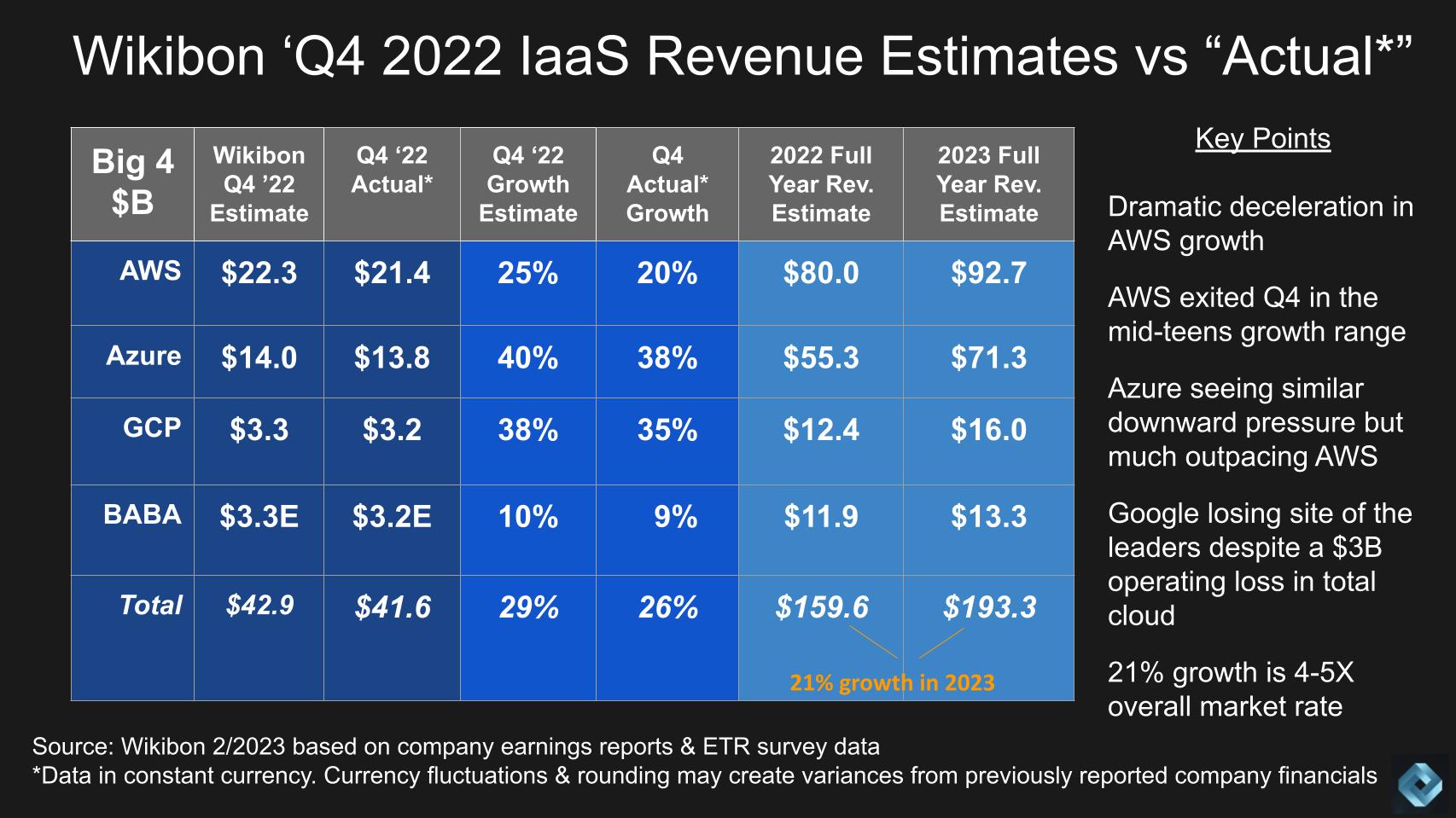

Let’s boil this down to the market data. In the graphic below, we show our estimates for Q4 IaaS revenue compared with the “actuals.” We put actuals in quotes because Microsoft doesn’t report Azure revenue and Alphabet doesn’t share GCP revenue. Rather, each firm buries the figures in its overall cloud numbers, which include SaaS. Microsoft and Alphabet make general statements and provide a few crumbs on Azure and GCP, respectively, and leave it to us to triangulate.

Wikibon started modeling quarterly AWS revenues in the first quarter 2013, two years before Amazon formally began to report AWS revenues. We’ve added Azure, GCP and Alibaba Cloud over time and in 2019 began partnering with ETR to refine our estimates.

Looking at the data above, we had AWS growing 25% year-over-year in Q4 2022 ($22.3 billion) and AWS came in at 20% growth ($21.4 billion), a significant delta relative to our expectations. Azure was two points off our forecast, coming in at 38% growth, GCP three points off, coming in at 35%, and Alibaba has yet to report but we’ve shaved a bit off that forecast based on some survey data.

For the year, the big four hyperscalers generated almost $160 billion in revenue… $7 billion lower (about 5%) than what we expected coming into 2022.

For 2023 we’re expecting 21% growth for the market for a worldwide revenue total of $193.3 billion. Though lower than our previous outlooks, that’s still four to five times the overall spending forecast for the market, which we reported last week at 4% to 5% growth.

We expect AWS to come in at about $93 billion this year with Azure closing in at more than $71 billion. Despite Amazon focusing investors on the fact that AWS’ absolute dollar growth is still larger than its competitors, by our estimates Azure will come in at more than 75% of AWS’ forecasted revenue. We feel that is a significant milestone especially because by our estimates, Azure is growing at a rate double that of AWS.

Notably, AWS’ operating margin declined significantly this past quarter, dropping from 30% of revenue to 24%. Although this is still extremely healthy and we’ve seen fluctuations like that before, Microsoft we think has the upper hand when it comes to profitability. Specifically, Microsoft has a marginal cost advantage because: 1) It has a captive cloud on which to run its massive software estate; and 2) Software marginal economics, despite AWS’ awesomeness and high degrees of automation, are just better.

The upshot for AWS is the ecosystem. AWS is positioning very smartly as a platform for data partners such as Snowflake and Databricks, security partners such as CrowdStrike Holdings Inc., Okta Inc., Palo Alto Networks Inc. and others, as well as SaaS companies that may be more competitive with Microsoft. Even though AWS has competitive products in database, for example, AWS appears more happy to “spin the meter ” with partners — more so in our view than the other cloud players.

From a profitability standpoint, AWS is willing to share margin with partners, which we think will lead to a larger market for IaaS, and that underscores is the long game AWS is playing.

The major hyperscalers all have strong stories in machine learning and artificial intelligence. Microsoft, of course, is hyping its OpenAI LLC investment and ChatGPT and people are moving to Azure to get it. Amazon has to have a response in our view. AWS has a strong AI story, and it’s going to have to make some moves there. Meanwhile, Google is emphasizing itself as an AI-first company. In fact, Google spent at least five minutes of continuous dialog on its last earnings call, pitching its AI chops to analysts.

This is an area we’re watching closely as the buzz around large language models and conversational AI continues.

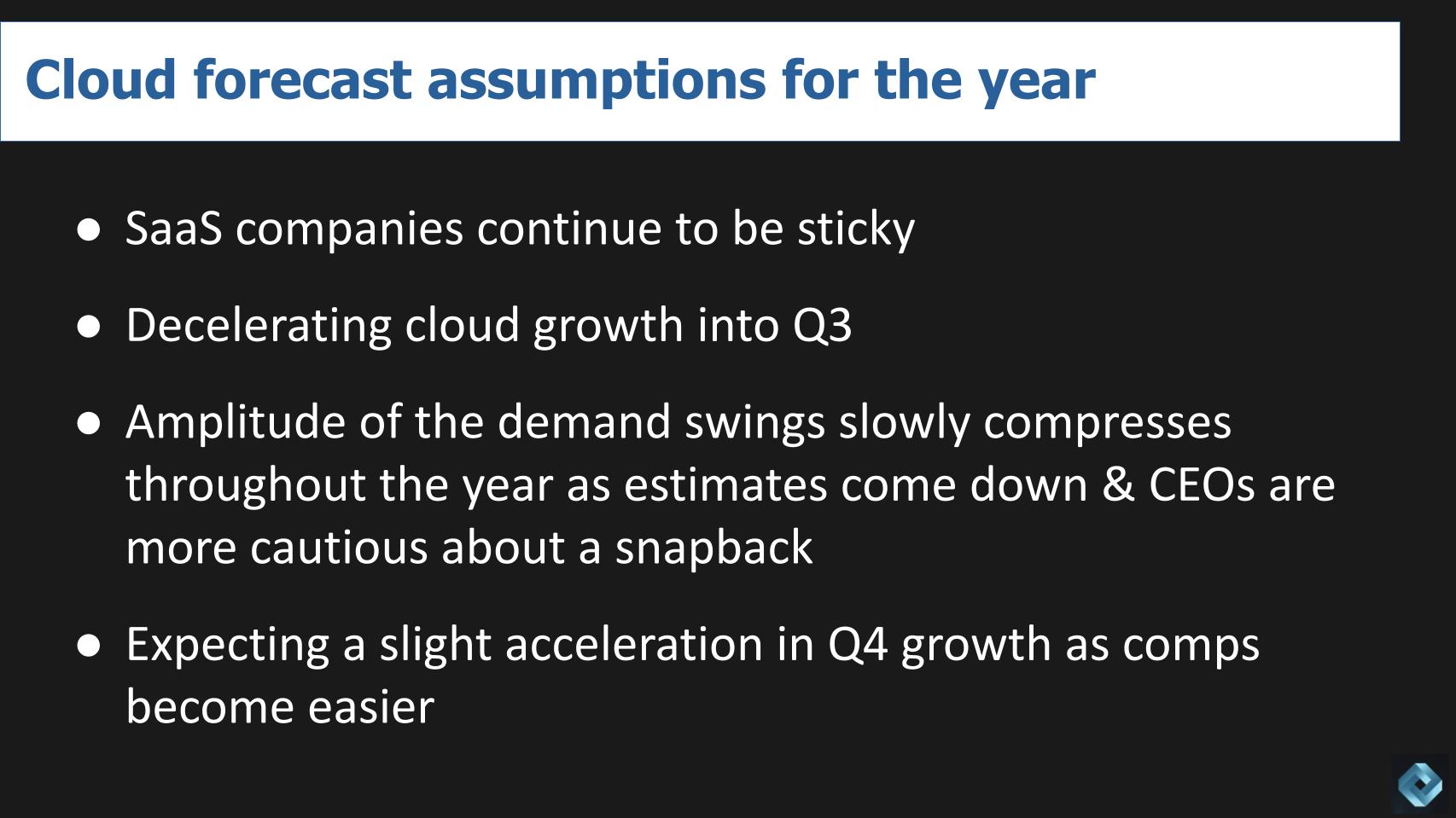

According to our research, the SaaS segment is likely to remain resilient despite the market downturn, owing to the high stickiness of these services. But we believe customers will be more cautious about new additions. As well, over time we believe the onerous pricing models of many legacy SaaS offerings may cause a gradual decline in demand as customer backlash forces firms to evaluate alternative models that are more consumption-based.

Cloud technology and the hyperscalers in particular are expected to experience slowing growth rates into the third quarter. The fluctuations in demand for cloud services are projected to become more stable and predictable throughout the year, as estimates have been gradually lowered and guidance has become more cautious. In addition, we anticipate that CEOs will adopt a more careful hiring and spending approach as the market starts to recover, contributing to better visibility by year-end.

Despite the projection of an orderly return to growth in the fourth quarter, a number of economic factors, including the actions of the Federal Reserve, consumer spending, inflation, supply chain disruptions, energy prices, geopolitical tensions and China relations, pose a significant risk to this outlook.

Along with our partners at ETR, we’ll continue to monitor trends and provide insights and data as the market evolves. As always, we remain dedicated to providing our community with the most up-to-date information to help you make informed business decisions.

Many thanks to Alex Myerson and Ken Shifman on production, podcasts and media workflows for Breaking Analysis. Special thanks to Kristen Martin and Cheryl Knight, who help us keep our community informed and get the word out, and to Rob Hof, our editor in chief at SiliconANGLE.

Remember we publish each week on Wikibon and SiliconANGLE. These episodes are all available as podcasts wherever you listen.

Email david.vellante@siliconangle.com, DM @dvellante on Twitter and comment on our LinkedIn posts.

Also, check out this ETR Tutorial we created, which explains the spending methodology in more detail. Note: ETR is a separate company from Wikibon and SiliconANGLE. If you would like to cite or republish any of the company’s data, or inquire about its services, please contact ETR at legal@etr.ai.

Here’s the full video analysis:

All statements made regarding companies or securities are strictly beliefs, points of view and opinions held by SiliconANGLE Media, Enterprise Technology Research, other guests on theCUBE and guest writers. Such statements are not recommendations by these individuals to buy, sell or hold any security. The content presented does not constitute investment advice and should not be used as the basis for any investment decision. You and only you are responsible for your investment decisions.

Disclosure: Many of the companies cited in Breaking Analysis are sponsors of theCUBE and/or clients of Wikibon. None of these firms or other companies have any editorial control over or advanced viewing of what’s published in Breaking Analysis.

Support our mission to keep content open and free by engaging with theCUBE community. Join theCUBE’s Alumni Trust Network, where technology leaders connect, share intelligence and create opportunities.

Founded by tech visionaries John Furrier and Dave Vellante, SiliconANGLE Media has built a dynamic ecosystem of industry-leading digital media brands that reach 15+ million elite tech professionals. Our new proprietary theCUBE AI Video Cloud is breaking ground in audience interaction, leveraging theCUBEai.com neural network to help technology companies make data-driven decisions and stay at the forefront of industry conversations.