Generative artificial intelligence has created a new mandate in enterprise tech with significant implications for all companies generally and Amazon Web Services Inc. specifically. Amazon’s powerful playbook based on agility, developer choice, power, scale, reliability and security must now evolve to accommodate simplicity and coherence for mainstream customers.

This imperative came into clear focus at AWS re:Invent 2023 this past week. AWS continues to innovate at a fast pace, but it must now do so in a changing customer environment that increasingly values direct user productivity gains through software.

In this Breaking Analysis, we share our take on how AWS is navigating this challenge. We’ll review Amazon’s strategy to compete in the nascent gen AI era and we’ll provide commentary on the chess moves it’s making with Anthropic PBC, Nvidia Corp. and other partners to maintain its leadership position. We’ll also discuss the challenges of doing so as a $90 billion-plus giant in a fast-moving market.

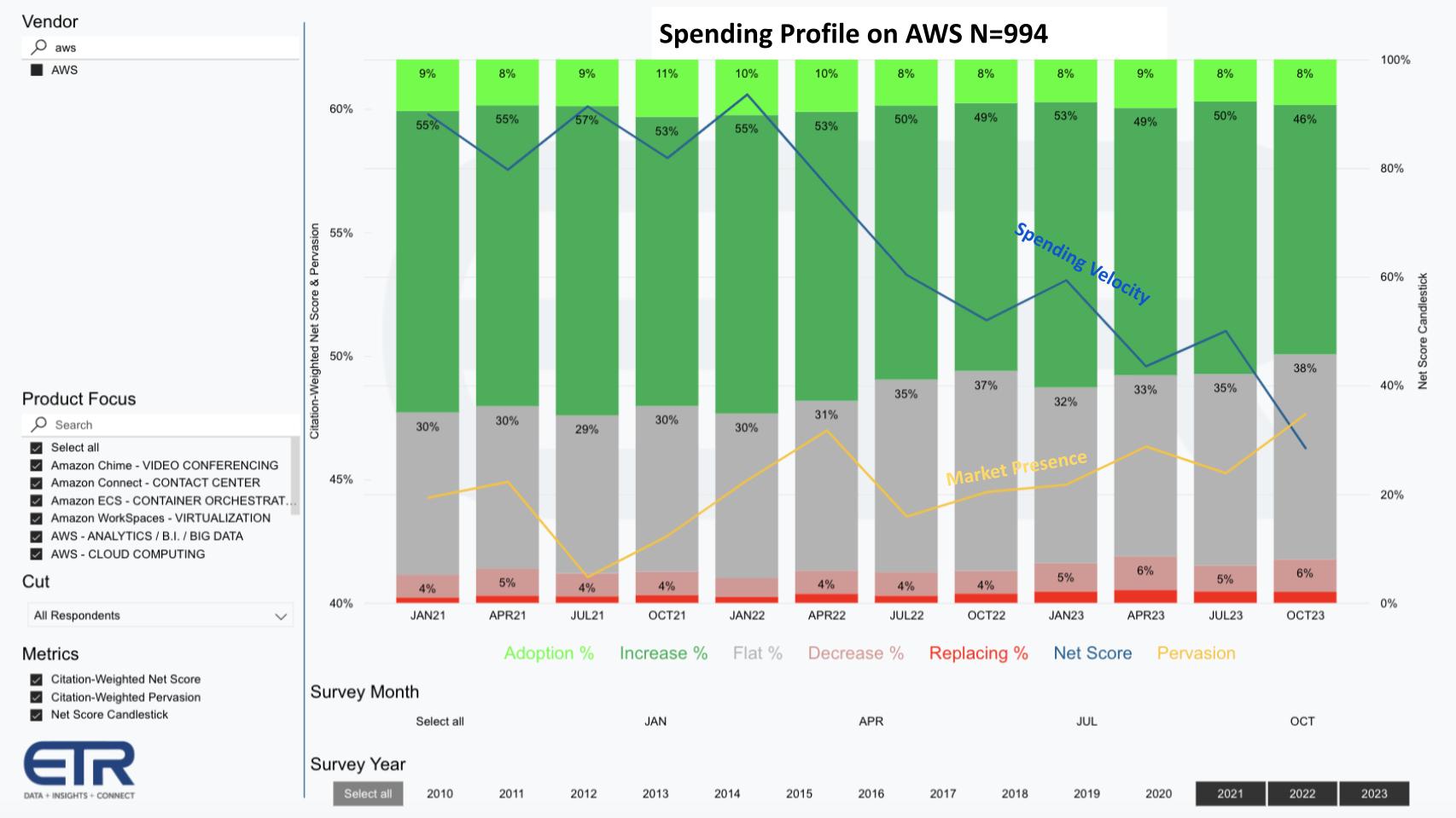

AWS is not immune to macro headwinds

This chart above from Enterprise Technology Research shows the Net Score granularity for AWS across nearly 1,000 customers in ETR’s quarterly surveys. Net Score is a measure of spending momentum that essentially tracks the net percentage of customers spending more (i.e. the green bars) netting out those spending less (the red). The blue line shows that calculated metric indicating AWS, like most well-positioned tech firms, had a strong 2021 and met an increasingly challenging macro environment in 2023.

Microsoft Corp. and Nvidia are two rare exceptions to this trend.

The yellow line above shows relative market presence in the data set, measured by the N responses for AWS (994) divided by the total N of the survey (~1,700). AWS’ presence in the data set continues to trend in a positive direction. However, like most companies, the combination of macro spending headwinds and cost optimization have downshifted shifted spending momentum. Nonetheless, as our earlier research shows, AWS growth rates held up sequentially last quarter and we expect reaccelerating growth in the fourth quarter.

The following four points summarize our assessment of the current market and add additional context for this research:

Spending: Spending is also being affected by budgets being reallocated to generative AI projects. Because the demand for expensive GPUs is so high, the business of tech is becoming much more capital-intensive. As such, we’re seeing a huge shift in data center spend toward Nvidia and Nvidia-enabled solutions. This is being driven not just by GPUs, but entire supercomputing-class clusters.

AWS focus: AWS reemphasized infrastructure more intensely than it has in years because AWS can “compose” hardware to support specific workloads much better than Azure. Amazon is reminding customers that software runs better on its infrastructure.

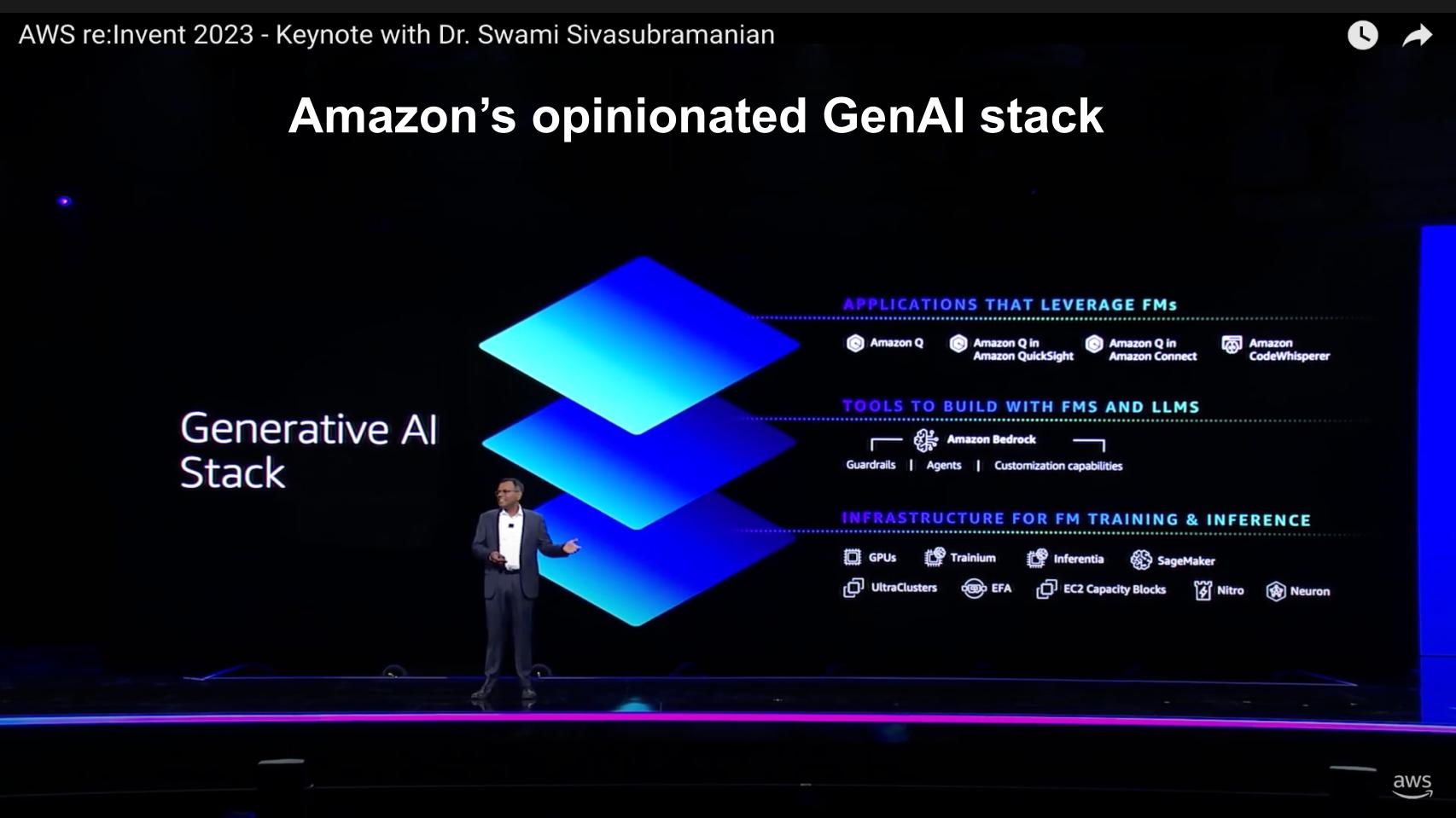

Gen AI stack: AWS focuses on three layers starting with AI infrastructure, Bedrock (the abstraction layer for large language model optionality) and Q at the application layer (its copilots).

Hardware versus software mindset: AWS’s mindset is to design a coherent hardware architecture that software would “light up.” Microsoft designed coherent, composable software building blocks and some hardware to run it. Microsoft’s Ignite conference unveiled its “iPhone moment” for corporate developers, with a message of copilots everywhere.

Topics for today

It is impossible to cover in one Breaking Analysis the hundreds of announcements made at a re:Invent. So we’ll focus today on the areas we feel are most impactful for customers and the competitive environment going forward, summarized below.

AWS went back to the basics of infrastructure this year. There was even a big focus in Peter DeSantis’ talk on Monday night about synchronizing clocks across systems down to microseconds. AWS emphasized its silicon lead with Graviton 4 and Trainium 2, its long history in compute, a new high-performance S3 object store, networking, security and a lot of discussion on database, especially zero ETL, or extract/transform/load data preparation.

We’re going to talk about the AWS gen AI stack and give you our take on how it came about and our hypothesis about the relationship with Nvidia. As indicated above, AWS’ gen AI stack has three layers: 1) Infrastructure for AI; 2) Tools to build with foundation models and LLMs such as Bedrock, an abstraction layer to enable LLM optionality; and 3) Intelligent applications that leverage foundation models such as Q, which AWS showcased and which represents its version of copilots.

We’ll also discuss the data imperative for customers and what AWS in our view must do beyond the innovations announced at re:Invent 2023.

Finally, we’ll net out our view of where AWS needs to focus going forward.

AWS emphasized its infrastructure roots

In AWS Chief Executive Adam Selipsky’s keynote on Tuesday (pictured), he doubled down on core infrastructure. Here’s our assessment of why:

Analysis of AWS’ infrastructure and software strategy

Quick takes on Selipsky’s keynote:

In recent years, Selipsky has not emphasized infrastructure in keynotes as significantly as he did at re:Invent 2023.

AWS’ strategy highlighted its robust hardware platform origins and unique composable architecture.

This architecture allows for dynamic assembly of complex systems, such as: Compose a storage area network for SAP or Oracle workloads, or spin me up some on-demand supercomputers.

AWS’ approach contrasts sharply with Microsoft’s and challenges the infrastructure capabilities of Azure, which are not as robust as those of AWS.

Software design philosophy:

AWS’ software was crafted for choice, power, flexibility and granularity… but not necessarily for composability.

The shifting market trend, accelerated by generative AI, now prioritizes software development productivity, where composability is a key attribute of the software.

Composability entails designing software components to integrate software functionality seamlessly across cloud services, a dynamic for which the AWS cloud is not optimized.

Comparative analysis of Amazon and Microsoft:

In our assessment, Amazon’s software development has historically focused on maximizing hardware potential, not on creating composable solutions for end-users.

Amazon’s mindset is more hardware-centric in our assessment, prioritizing great hardware that is enhanced through software, without a strong emphasis on software integration.

In contrast, Microsoft, primarily a software company, embraces software composability as a design principle. Though it often takes Microsoft several iterations to get it “right,” eventually it gets there.

Microsoft’s recent showcase at Ignite, featuring Copilot Studio and numerous connectors, highlighted its advanced, integrated software aspirations and design principles.

In our view, Microsoft views hardware merely as a platform for its software. Although Microsoft’s hardware is inferior to that of AWS’ in our view, its software is much more facile for customers to consume. This is a critical factor for generative AI adoption, in our opinion, which AWS will have to replicate via its developer ecosystem.

Strategic implications for customers:

AWS’ “best infrastructure” cloud advantage has been effective, but the evolving market necessitates a shift toward more integrated and composable software solutions.

The current market trajectory favors companies with a strong foundation in software composability and integration.

Customers should monitor AWS’ response to this shift and its potential adjustments in software strategy to stay competitive as the customer priority shifts to simplicity and developer productivity.

Proof points on the world’s best cloud infrastructure

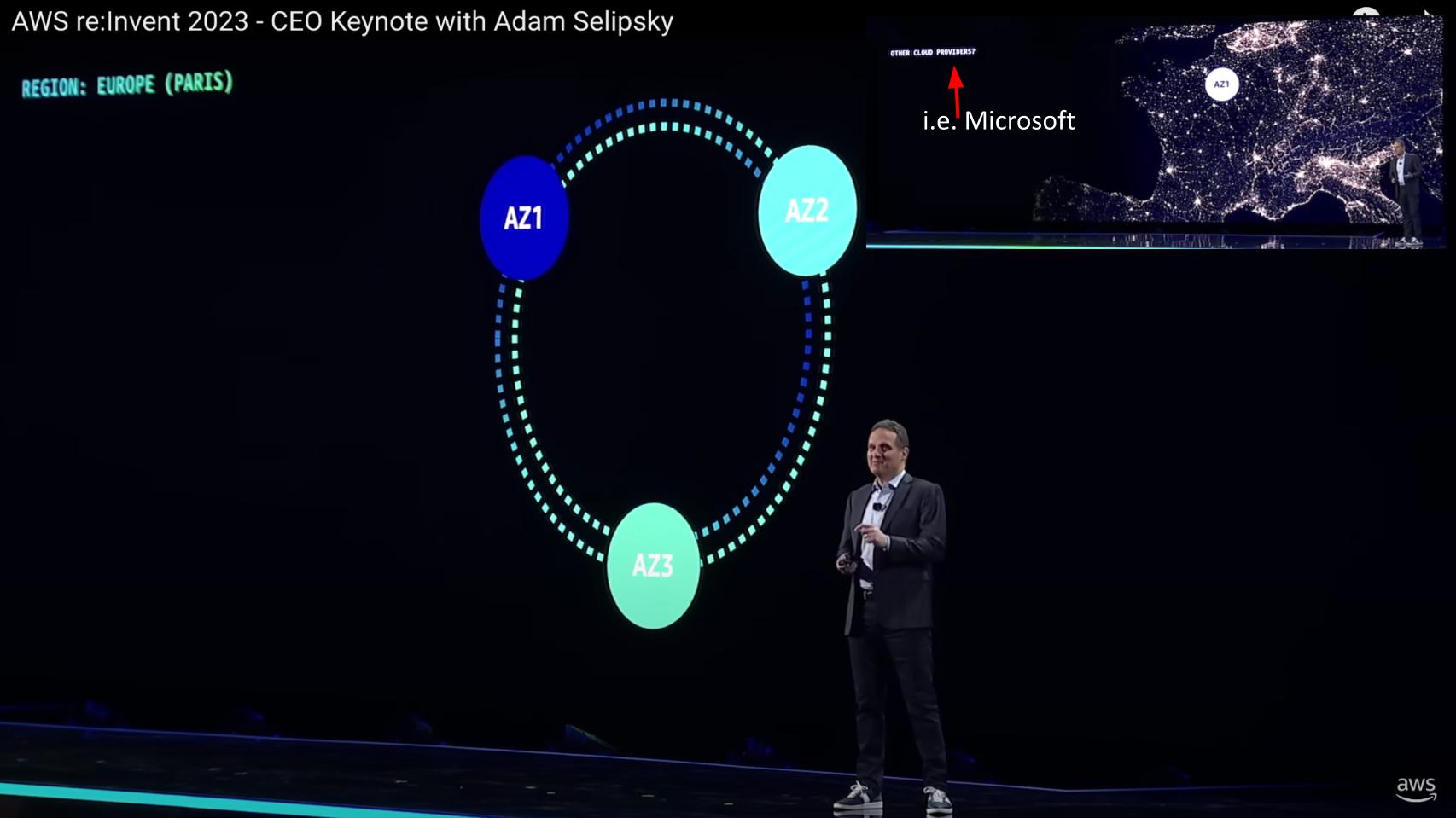

At Ignite, Microsoft CEO Satya Nadella bragged about the number of data centers around the world, citing Microsoft’s leadership in that category. Selipsky’s counterpunch to that claim is shown on the screenshot below (with our red arrow annotation).

He is showing that an AWS region contains three availability zones that are a hundred kilometers apart. They’re essentially running at synchronous speeds. So if there’s a fire or flood in one AZ, it can fail over to another one.

And you can see in the upper right of this graphic that it shows the “other cloud providers” (i.e. Microsoft). Basically it’s one data center in an AZ zone. So if you lose that one, you’re in trouble. Of course, you can fail over to another data center, but it’s probably done at asynchronous distances and the likelihood of data loss increases as a function of a customer’s recovery point objective, or RPO.

The point Selipsky is making is Amazon has a far superior infrastructure and he’s reminding customers that our hardware is great and even if you’re running third-party software, it runs better on our infrastructure.

AWS goes back to its S3 roots (where it all began)

In Selipsky’s keynote he began by emphasizing the deep adoption of cloud computing across financial services, healthcare, manufacturing, automotive and, eventually, telecommunications and other industry examples. But the first news announcement AWS shared at his re:Invent keynote was a new high-performance object store, Express One Zone.

S3 revolutionized cloud storage. High-performance object storage has been around for a while, but AWS has it now and is lowering costs for customers. It goes back to our core takeaway on AWS’ message this year: You can’t divorce the infrastructure from the software because if you have a better hardware architecture, you can build better software.

An example is that Snowflake Inc. was able to build a great product because it was built on AWS and it could separate compute from storage. At the time, Teradata and Oracle couldn’t. So what AWS is saying, in our view, is that now, with fast object storage, you don’t have to rig up complicated caching to get high performance.

The nuanced relationship between AWS and Nvidia

Amazon made a strong case showing the timelines of its firsts with Nvidia deployments over time. Nvidia CEO Jensen Huang is like a brilliant chameleon at these tech shows. At Dell Technologies World, for example, he emphasized the potential of graphics processing units in laptops. At Snowflake Summit he talked about how Nvidia would supercharge data in Snowflake. At re:Invent 2023 he shared AWS has deployed 3,000 Nvidia supercomputers.

And in an apparent change of heart, the big news at re:Invent 2023 was AWS announced support for the Nvidia DGX cloud, support that Microsoft had just announced the week before, and a move that reportedly AWS initially resisted. In June of this year, Reuters broke a story citing AWS Vice President Dave Brown as saying the company passed on DGX cloud and preferred to buy Nvidia chips piecemeal.

The turnaround underscores the power Nvidia wields in today’s market. What follows is our summary analysis on this situation and how and why it came to fruition:

Analysis of the complex relationship among Huang, Nvidia and AWS

The AWS-Nvidia partnership dynamics:

AWS needs Nvidia’s GPUs, but Nvidia prefers selling its DGX data center clusters, leading to a complicated relationship with cloud vendors generally and AWS specifically.

AWS has historically been a pioneer in deploying Nvidia’s technology, including being the first to use GPUs.

Huang is a pivotal figure in this dynamic – we liken him to a “power broker” in the tech industry.

Strategic moves and challenges:

AWS announced support for Nvidia’s DGX cloud, countering Microsoft’s recent announcement at Ignite and changing course from its initially reported stance on the move.

The initial resistance from AWS to adopt Nvidia’s DGX Cloud, possibly impacted its access to high-performance GPUs. [Note: Senior AWS sources have flatly denied that they are somehow being penalized by Nvidia with respect to GPU access, citing that it’s a leading consumer of H100 GPUs in the world.]

Nvidia’s preferred strategy, however, involves selling complete data center size clusters optimized for training large language models, in contrast to AWS’ most common multitenant virtualized architecture.

[We note, however, that AWS has successful partnerships that have relied on alternative architectures. For example, VMware Cloud on AWS runs on a special bare-metal instance created by AWS.]

Market position and revenue implications:

Microsoft, lagging in hardware, outsourced its accelerated infrastructure needs to Nvidia, accounting for a significant portion of Nvidia’s revenue.

Nvidia is not just selling GPUs, but a bundle of functions, including data center clusters.

We believed AWS’ initial reluctance to adopt Nvidia’s full cluster solution resulted in a limited GPU allocation, which sources at AWS have denied.

Regardless of the speculation, both companies need each other. AWS needs to offer Nvidia’s technology, including DGX clusters, even if in limited capacity, to maintain market competitiveness.

Nvidia needs AWS, the cloud leader to distribute its DGX clusters and GPUs, especially considering competition from companies like Microsoft who is adopting DGX, Google with their own chips and clusters, and specialized cloud providers such as CoreWeave Inc.

Operational and financial considerations:

In our view, a big part of these Nvidia announcements is as much about optics and market positioning as it is a full embrace of each other’s technologies. The entire industry is griping about Nvidia’s price gouging and is eagerly anticipating Advanced Micro Devices Inc. expanding production of GPUs.

The reality is that Nvidia has a substantial lead because of its investments in its CUDA software architecture, its Mellanox acquisition and years of experience in the space.

AWS’ capacity to integrate Nvidia’s technology, similar to its approach with VMware cloud, showcases its adaptability and customer focus.

The Nvidia clusters are complex and expensive, which involve significant investment and operational challenges for competitors. AWS and the big cloud companies are well-positioned to deliver.

Allocation and supply chain insights: implications for customers:

There is uncertainty across the industry regarding the allocation of Nvidia’s technology and whether any agreements or quid pro quo arrangements exist in exchange for AWS leaning into the DGX cloud.

Customer should consider these supply challenges as they make investments. Spreading bets around may make sense especially based on workloads. Concerns over the OpenAI governance challenges can and will have an impact on customer decisions about which workloads to deploy where (i.e. which clouds and on-premises deployments) based on privacy, legal and governance considerations.

Industry watchers who have deep insights into the supply chain dynamics will offer an ongoing glimpse into the allocations and partnerships between these tech giants, and we’ll continue to collaborate with them to get the best information possible.

Investor and customer perspective:

From an investment standpoint, this relationship presents both challenges and opportunities.

The interdependency between AWS and Nvidia creates a delicate balance in their operations and market offerings.

Investors should closely monitor how this partnership evolves, particularly in terms of technology integration, market strategy and financial implications.

We expect generative AI tailwinds to accelerate cloud growth. The combination of the recent general availability of Bedrock, momentum from re:Invent 2023 and Microsoft Ignite, our cloud forecasts call for an acceleration in sequential growth in the fourth calendar quarter for both AWS and Microsoft.

Assessing AWS’ three-layered gen AI stack

The AWS gen AIsStack is shown above. At the infrastructure layer, Nitro enables composable supercomputers for training along with other custom silicon like Trainium and Inferentia. At the tool layer there is SageMaker and Bedrock, which abstracts a single interface to LLMs. At the application level there are tools such as Q copilots to leverage foundation models.

Summary of AWS’ three-layered technology stack and its strategic focus

Overview of AWS’ technology stack:

AWS’ technology stack comprises three layers: core infrastructure, a middle layer focusing on LLMs, and the application layer.

The core infrastructure layer is enabled by Nitro, a lightweight virtualization engine that supports diverse silicon, including GPUs from various manufacturers.

This layer includes machine learning tools such as AWS’ SageMaker and its infrastructure stack, repurposed for generative AI applications.

Nitro’s role and hardware composability:

Nitro revolutionized AWS’ approach four years ago, providing hardware composability, an essential aspect for accommodating different types of processors and GPUs.

However, this level of composability wasn’t mirrored in AWS’ software approach, underscoring what in our view is a critical and necessary area for development.

Middle layer: Bedrock and LLMs:

The middle layer, Bedrock, is crucial for AWS in offering a range of LLMs, including Anthropic and its own Titan models.

AWS’ response to the LLM wave emphasized offering choice, reflecting its hardware-first mindset. In other words: “Our hardware is so good that software runs better on our infrastructure.”

The inclusion of Anthropic is strategic, not just to provide customers with a leading-edge LLM, but also to aid in the development of AWS’ own developer products. AWS’ investment of up to $4 billion in Anthropic is critical to counter Microsoft’s exclusive with OpenAI and Google’s internal AI expertise (and Google’s own deal with Anthropic). Although Amazon has been a leader in AI for years with tools such as SageMaker, its Titan LLMs alone won’t satisfy customer demands.

Application layer and competitive landscape:

The top layer focuses on applications, exemplified by products like Code Whisperer, which was showcased recently.

AWS’s stack is coherent and compelling, with Bedrock playing a pivotal role.

The top layer of the stack is the traditional domain of AWS’ partners and customers and is increasingly pivotal for developers to drive productivity deep into organizations. This is where AWS accelerated resources over the past six months to get a credible Q demo working for re:Invent – but much work is needed in this area, in our view.

Strategic need for Anthropic in AWS’ services:

AWS’s integration of Anthropic is crucial to remain competitive, especially considering Microsoft’s and Google’s advancements in state-of-the-art developer services, partly thanks to their early investments in advanced LLMs.

AWS’ approach to LLMs, including its partnership and usage of Nvidia infrastructure, although largely reliant on partnerships, is a significant part of its strategy.

Implications for customers, investors and the market:

This three-layered approach by AWS is coherent and indicates a strong focus on keeping pace in the generative AI race.

The balance between LLM diversity and a deep partnership with an advanced LLM player such as Anthropic is key to AWS’ strategy.

The limitations of its own LLM in the form of Titan require AWS in our view to have the closest relationship with Anthropic and be the most attractive partner-obsessed firm in the battle for AI supremacy.

Customers and investors should monitor how AWS continues to integrate and develop these technologies, especially in relation to its competitors such as Microsoft and Google.

Pay attention to the degree that AWS can maintain its lead in custom silicon and leverage Anthropic’s domain knowledge to stay ahead.

The integration into Q of Anthropic and other LLMs available in Bedrock are critical to success and a key barometer of leadership in our view.

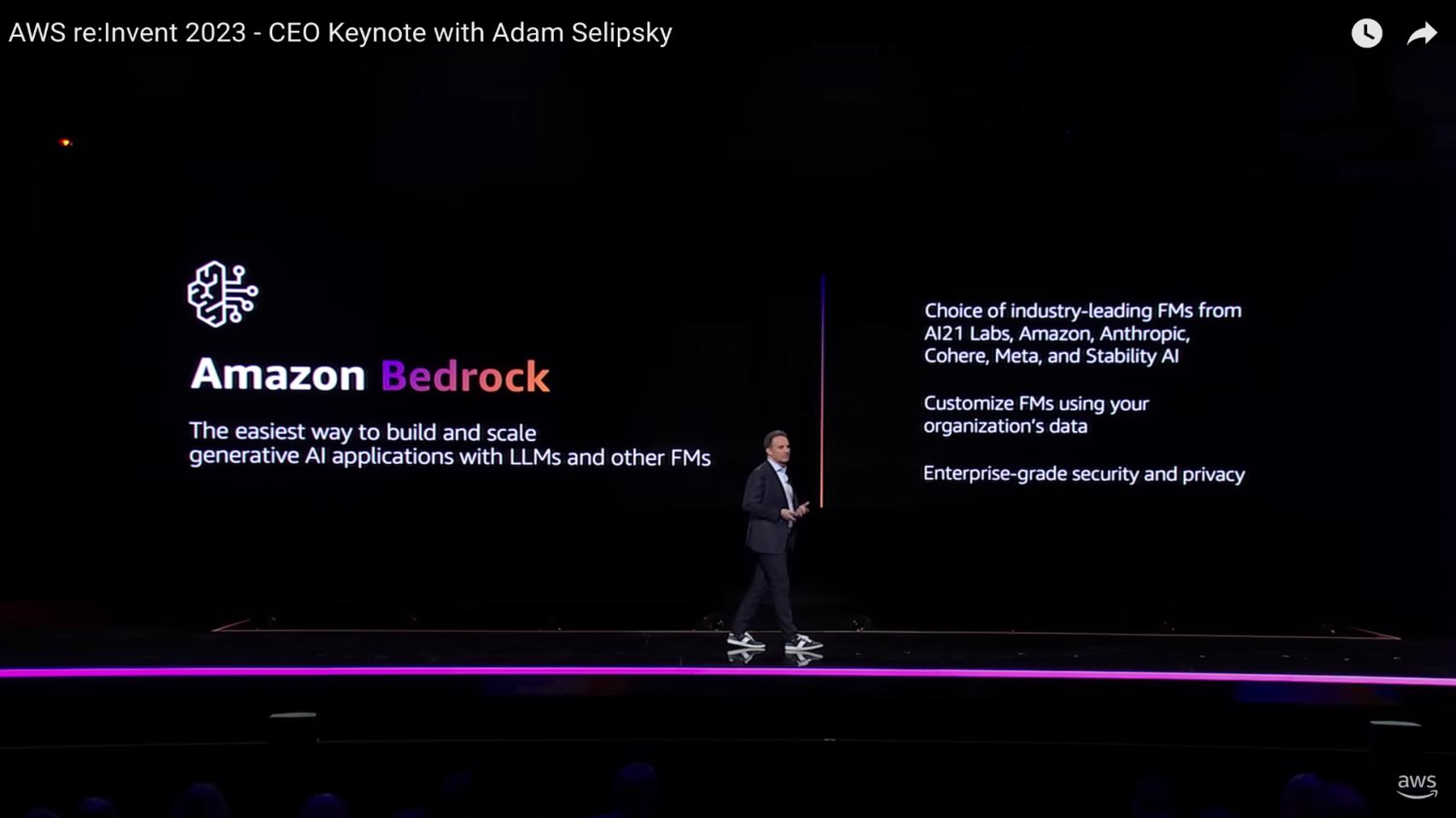

Let’s double-click into Bedrock

Simply put, Bedrock is AWS’ fully managed service that offers access to several foundation models, as shown in this screenshot above. Model optionality includes LLMs from AI21 Labs, Amazon’s own Titan, Anthropic, Cohere, Meta’s Llama 2 and Stability AI. These are available through an application programming interface along with key developer tools to build gen AI applications.

Analysis of Amazon’s strategy with Bedrock: multiple frontier models for generative AI

Need for optionality for frontier models:

Amazon in our view lacked an in-house frontier model that was as advanced as those from OpenAI and Google. In our assessment we see these competitive models adhering to scaling attributes around compute power, model size, parameters and training data.

Each generation of these models tends to be significantly larger and more capable, an emergent phenomenon seen in AI development.

Comparative market positioning:

Titan, Amazon’s existing model, did not qualify in our opinion as an advanced frontier model under these criteria.

Microsoft foresaw the importance of frontier models to the future of software development and invested in OpenAI as early as 2019.

Our research indicates that Google, despite being ahead in this area, hesitated to apply these models to search because of privacy, legal and governance concerns and potential disruptions in its search cost structures.

Amazon’s response and strategic shift:

Most companies, including Amazon, began paying significant attention to these models only in 2022.

Nonetheless, Amazon’s shift came later in the race given Microsoft’s relationship with OpenAI and Google’s AI capabilities. Our sources indicate Amazon CEO Andy Jassy has made generative AI a personal top priority despite his other duties.

Amazon’s recent step-up in its investment of advanced frontier models is not just for customer benefit but also a crucial part of its internal development, such as for its new product Q.

The complexity of integrating frontier models:

Simply having a frontier model on a platform is insufficient; it requires years to integrate these models into the functionality of existing tools.

We see frontier models as enabling technologies, necessitating deep and complex integration into existing systems and tools.

We call attention to a couple of examples in enterprise software development. SAP’s transition to relational databases is one that underscores the time and effort needed for such integrations. Oracle’s decade-long journey to get Oracle Fusion to a best-in-class status is another good example of the challenges of integrating complex software in mission-critical applications.

AWS has its work cut out to turn software that has been developed with a primary objective of making infrastructure run better to developing software that is composable and ultimately drives user productivity.

Implications of the Bedrock and Anthropic deal:

Amazon’s deal with Anthropic is not only about offering these capabilities to customers but also crucial for enhancing their own software functionalities.

The strategic importance of this deal goes beyond customer-facing benefits, indicating a deeper commitment to advancing Amazon’s own technology stack.

Investor and customer perspective:

Investors and customers should view Amazon’s late but strategic move into frontier models as a significant development.

The company’s efforts to catch up in this field and the potential impact on its product offerings and internal capabilities are critical areas to monitor.

The long-term implications of integrating these advanced AI models into Amazon’s ecosystem could be substantial for its market position and competitiveness.

The effort to do so is nontrivial and and our opinion requires AWS to extend its mindset toward composable software.

AWS’ imperative to secure priority access to advanced foundation models

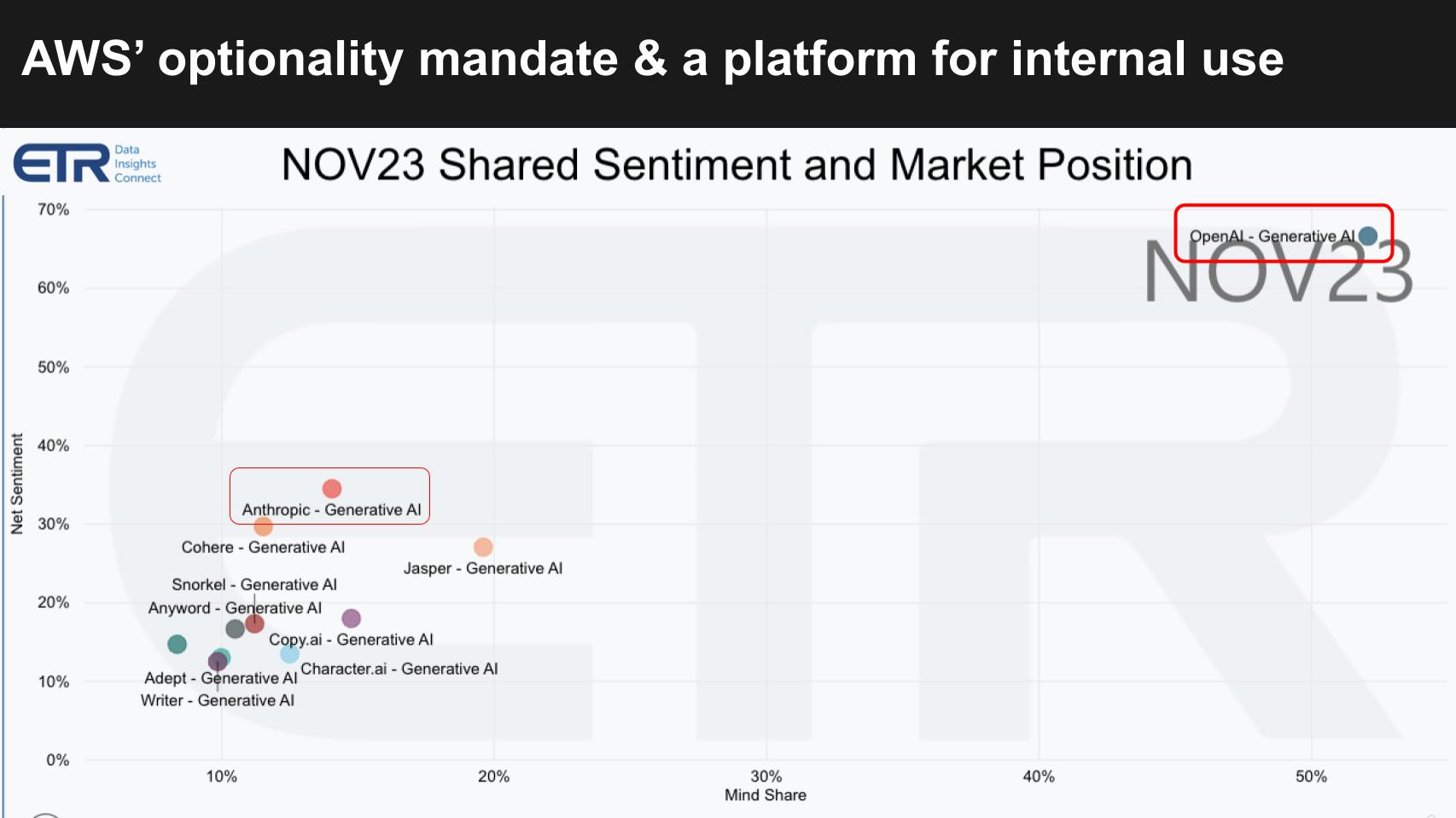

Despite the governance failures of the Microsoft OpenAI partnership, OpenAI and Microsoft have a wide lead in market momentum. To underscore this point let’s look at some ETR engagement/sentiment analysis and mindshare data specific to gen AI models.

The chart above is from ETR’s emerging technology survey of privately held companies. The vertical axis measures Net Sentiment, a metric that tracks the percentage of customers specifically planning to engage with a platform, netting out those that plan not to engage. The horizontal axis is mindshare. Note the position of Open AI relative to the pack. That separation is a reflection of the market momentum.

Because Microsoft had locked up a deal with OpenAI with an exclusive, AWS had to counter with not only LLM optionality in Bedrock, but a tighter relationship with Anthropic. Hence its initial investment of $1.25 billion that could go up to as high as $4 billion over time. As part of the deal, AWS will be the preferred cloud for Anthropic to train its models and also Anthropic will bring its tribal knowledge to help AWS customize silicon for gen AI.

Will it be enough? Yes, in our view, but the question is timing. Because the challenge is primarily in software, there are tradeoffs between how much time you have to anticipate a problem so you can rework your architecture to build in new capabilities, versus taking on technical debt to get to market quickly.

Which brings us to Q – the top layer of AWS’ gen AI stack

Q is meant essentially to accelerate the software development lifecycle. It is AWS’ answer to copilots and workplace assistants. We believe Q was initially trained on Amazon’s Titan, its internal foundation model, but Amazon has some work to do to integrate with Anthropic and other LLMs. At the analyst summit this year, several of us pushed on what exactly is under the covers powering Q and it’s clear AWS intends Bedrock to be the answer.

The fact that AWS was able to show Q at re:Invent with such a compelling demonstration rather than just slideware is quite remarkable and underscores how intensely AWS has been working on this. But in our view, Q is still a demo.

Analysis of Amazon Q and the challenges in developing fully functional copilots

Current status of Amazon Q:

Amazon Q is in our view AWS’ response to developing copilots and workplace assistants in the software development process.

It’s part of the top layer of AWS’ technology stack, initially trained on Amazon’s Titan model according to our sources.

Amazon Q is still in the early stages and requires significant development to become a fully functional copilot, in our view.

The challenge of composability:

A key challenge for Amazon Q, and copilots in general, is the issue of composability.

If the components of an application, such as analytic services, cannot operate on a common data store, it complicates the development process because of the need for data movement and transformation.

This lack of composability hinders the ability of copilots to simplify application building.

The role of frontier large language models:

Frontier LLMs, which benefit from scaling laws, are essential for delivering state-of-the-art services.

AWS needs these advanced LLMs to enhance Amazon Q and other services, with Anthropic being a key component.

The retooling of Q to leverage Anthropic and other LLMs is necessary for it to function as a world-class copilot.

Bedrock’s importance and limitations:

Bedrock, AWS’s AI “middleware” platform, is maturing and becoming competitive with alternatives such as Azure AI.

However, the issue lies not with Bedrock itself but with the underlying LLMs and the duration of their development.

Bedrock’s use in Amazon services involves calling different AWS services that don’t necessarily integrate well, in our opinion, and this will affecting the degree to which it can achieve composability — an attribute we believe is increasingly important.

Development lifecycle and coding assistance:

Q aims to assist through the entire software development lifecycle, which requires seamless integration and ease of use.

The evolution of coding assistance in LLMs is challenging, especially if deep LLM research was not a priority prior to 2022.

Amazon’s late focus on LLMs and hurried development require AWS to take a different strategy emphasizing LLM optionality. Though it’s a potential differentiator, both Google’s and Microsoft’s can also offer alternative LLMs and at the same time lean on their “internal” LLM capabilities (Microsoft via its OpenAI exclusive).

Retooling for Anthropic and future prospects:

We see retooling Q with Anthropic as an important imperative that can be a relatively quick fix, especially for coding assistance and we would expect to see meaningful results by the next re:Invent.

However, the broader application of LLMs in DevOps, such as diagnosing and remediating operations, is a more challenging and lengthy process and in our view will take more time.

The integration of extensive operational data and the necessity to understand context make this a complex task.

Investor and customer implications:

Investors and customers should view Amazon’s efforts in developing Q and its integration with frontier LLMs as a crucial but challenging endeavor.

In our opinion, the potential of Q as a fully functional copilot depends significantly on Amazon’s ability to overcome composability challenges and effectively integrate advanced LLMs like Anthropic.

The progress and effectiveness of Q will be a key factor in AWS’ competitive positioning in the rapidly evolving field of AI-driven software development tools.

AWS’ data opportunities, challenges and imperatives

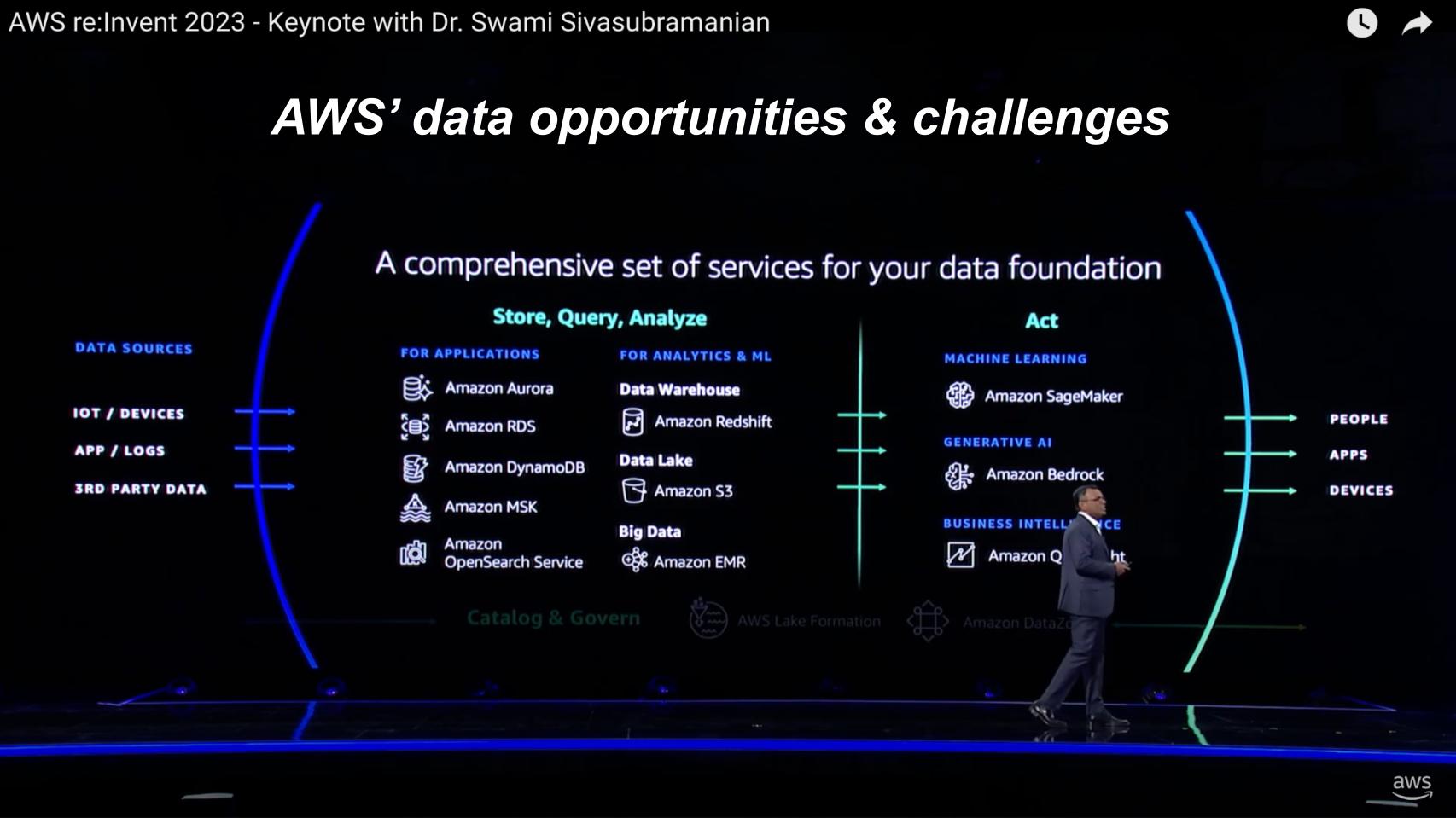

The quality of data is ultimately going to determine the competitive advantage customers can get from generative AI. Amazon has had a strong track record of developing databases and other tools that are fit for purpose aimed at specific use cases and application classes: Aurora for transactions, RedShift for analytics, Kinesis for streaming data, and so forth. AWS has many highly capable data stores. And this has served them well.

The challenge is now in a world where gen AI becomes the productivity driver, how will AWS present a unified front with its disparate data platforms — offering developers coherent data elements and metadata across all services so that builders can quickly develop intelligent apps?

Analysis of AWS’ data foundation and the journey toward unification

Challenges in unifying the AWS data foundation:

AWS faces technical challenges in unifying its core analytics engines, including Redshift, OpenSearch and EMR, which based on our assessment currently cannot share a common data store or metadata manager.

The quality of data is critical for leveraging generative AI, and AWS’ diverse databases have been developed with specific use cases in mind.

Although this has served AWS well, the main challenge lies in integrating these various data platforms to offer coherent data elements and metadata across services for AI-infused app development.

The emergence of vertical data lakes:

Vertical data lakes, particularly in security and supply chain sectors, demonstrate the need and power of unified data for analytics.

AWS has been successful in building vertical-specific data lakes, but struggles to leverage all analytic engines given data store disparities, based on our discussion with customers and internal experiences with our own software development.

Technical and operational hurdles:

The complexity of AWS’ data ecosystem, with multiple operational databases such as Aurora and DynamoDB, makes unification challenging.

Historically, centralized systems of truth have evolved into federated systems, requiring all analytic engines to interface with a coherent data repository.

The vision we believe will best serve customers is to store application logic intelligence with data, transforming it into building blocks for intelligent data apps.

Disparate data and metadata management:

Presently, data and metadata (data about data) are stored in separate locations within AWS’ infrastructure.

Analytic data stores such as Redshift and OpenSearch each have their own data stores, creating additional complexity.

Even though some analytic engines can access common storage like S3, limitations in performance and functions exist.

The need for a unified data foundation:

AWS is constructing specialized data lakes for sectors such as security and supply chain but faces challenges in using all analytic engines efficiently. We’d like to see similar capabilities emerge across AWS’ data platforms.

The goal is to establish a common data foundation similar to a security data lake, but the wide scope of AWS’ services makes this a difficult task.

Ultimately we believe Amazon DataZone will be the unification point for all business, operational and technical metadata with access for apps to a single virtual data store.

Implications for AI and data management:

In the age of AI, programming and training AI models depend heavily on having a coherent and organized data estate.

The unification of AWS’ data foundation is crucial in our view for efficiently developing and deploying AI-driven applications.

Investor and customer implications:

Investors and customers should note that AWS’ journey to unify its data foundation is a critical aspect of its strategy to leverage AI effectively.

The ability to overcome the technical challenges stemming from its disparate data products and successfully integrating its various data services will be key to AWS’ future growth and competitive advantage in the AI and cloud computing markets.

We believe a sixth modern data platform is emerging with a focus on real-time data where copilots can be systems of agency and take action for humans. This will require new thinking around data platforms

Unified governance continues to be a critical challenge for all data platform players and is an ongoing challenge for customers.

No one foundation model to rule the world

Let’s end with some summary thoughts on re:Invent 2023 and where we think AWS must focus in the days months and years ahead.

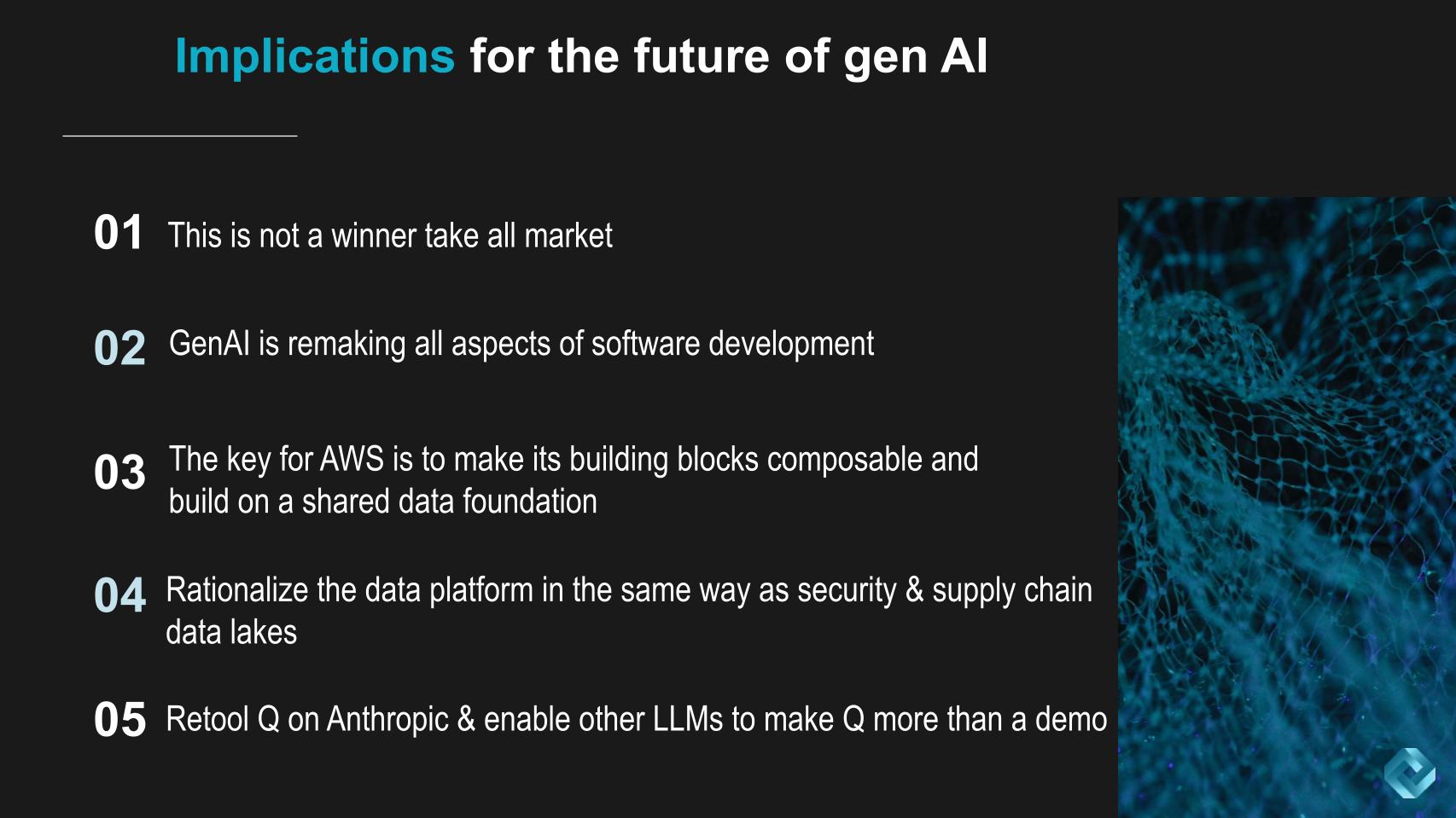

We want to stress that we don’t see this as a winner-takes-all market like so many in tech. AWS, with its best infrastructure, has a winning hand, and Microsoft, with its software prowess, will continue to do well, in our view. Microsoft frankly has a better margin model because it’s software but AWS will thrive with its infrastructure excellence.

But gen AI is changing all aspects of software development – through the entire lifecycle.

Summary and analysis of AWS’ strategic focus in the context of generative AI

Overview of AWS’ and Microsoft’s market position:

AWS’ strength lies in its infrastructure, giving it a significant advantage in the evolving landscape of generative AI.

Microsoft, known for its software prowess, operates with a different ethos, focusing on simplicity akin to the AS/400 for those that remember that far back.

We expect both AWS and Microsoft to continue thriving, each leveraging their unique strengths – AWS in infrastructure and Microsoft in software.

The impact of gen AI on software development:

Gen AI is transforming all aspects of software development, impacting processes throughout the entire lifecycle.

This transformation requires cloud providers to adapt and innovate, supporting new gen AI-driven development paradigms.

AWS’ approach: catering to technically sophisticated users:

AWS created the cloud market by catering to users who valued choice and power, following a Unix-like ethos of offering a wide range of options and flexibility.

However, mainstream customers, now more prominent in the market, prioritize productivity built on convenience and simplicity, accelerating with the advent of gen AI.

Challenges for AWS: simplicity and composability:

AWS faces the challenge of making its building blocks simpler for customers, focusing on composability and ease of use.

Though AWS excels in designing software to optimize hardware performance, it must now also focus on rationalizing its data platform in a coherent and simpler manner, as exemplified by its data lakes in security and supply chain.

Microsoft’s contrasting approach:

Microsoft is retooling its software approach to prioritize simplicity and integration, treating infrastructure as a necessary but not primary focus.

Retooling AWS’ Q on Anthropic and other LLMs:

AWS needs to rapidly advance its Q platform, leveraging Anthropic and other LLMs, to move beyond a demonstration stage and become a functional platform that builds trust in the market.

The ability of AWS to execute these changes effectively and efficiently is a critical factor in its continued success.

Prospects for AWS:

AWS has historically demonstrated strong execution capabilities, facing the challenge of adapting its offerings to meet the demands of a market shifting towards simplicity and integration.

The question for AWS is not about capability but rather about the extent to which it can integrate its components and align with market needs.

Investor and customer perspective:

Investors should recognize AWS’ strong infrastructure as a key asset, but also note the need for adaptation in the face of gen AI and changing market preferences.

The ability of AWS to simplify and make its services more accessible to a broader range of customers will be a crucial factor in maintaining its market position.

We’ll leave you with this thought: The need to trust data, software and the infrastructure supporting applications has never been greater. Compliance, legal issues, governance, security, local laws and fast recovery from failures are critical elements for customers today. AWS’ track record of building trust over nearly two decades has been remarkable.

Translating that trust into the gen AI era will require AWS to serve a broader set of customers that perhaps are not as technically capable as its historical developer base. And serving those new customers will require a new mindset, in our view, that values simplicity.

AWS turned the data center into an API and dramatically simplified IT. Now it’s time to simplify business and take productivity to levels not seen since the 1990s. As always, we’ll be watching, researching and reporting.

Tell us what you think.

Keep in touch

Thanks to theCUBE team at re:Invent 2023 for helping with this episode. Alex Myerson and Ken Shifman are normally on production and handle our podcasts and media workflows for Breaking Analysis. Special thanks to Kristen Martin and Cheryl Knight, who help us keep our community informed and get the word out, and to Rob Hof, our editor in chief at SiliconANGLE.

Also, check out this ETR Tutorial we created, which explains the spending methodology in more detail. Note: ETR is a separate company from Wikibon and SiliconANGLE. If you would like to cite or republish any of the company’s data, or inquire about its services, please contact ETR at legal@etr.ai.

Here’s the full video analysis:

All statements made regarding companies or securities are strictly beliefs, points of view and opinions held by SiliconANGLE Media, Enterprise Technology Research, other guests on theCUBE and guest writers. Such statements are not recommendations by these individuals to buy, sell or hold any security. The content presented does not constitute investment advice and should not be used as the basis for any investment decision. You and only you are responsible for your investment decisions.

Disclosure: Many of the companies cited in Breaking Analysis are sponsors of theCUBE and/or clients of Wikibon. None of these firms or other companies have any editorial control over or advanced viewing of what’s published in Breaking Analysis.

Photos: AWS

A message from John Furrier, co-founder of SiliconANGLE:

Support our mission to keep content open and free by engaging with theCUBE community. Join theCUBE’s Alumni Trust Network, where technology leaders connect, share intelligence and create opportunities.

15M+ viewers of theCUBE videos, powering conversations across AI, cloud, cybersecurity and more

11.4k+ theCUBE alumni — Connect with more than 11,400 tech and business leaders shaping the future through a unique trusted-based network.

About SiliconANGLE Media

SiliconANGLE Media is a recognized leader in digital media innovation, uniting breakthrough technology, strategic insights and real-time audience engagement. As the parent company of SiliconANGLE, theCUBE Network, theCUBE Research, CUBE365, theCUBE AI and theCUBE SuperStudios — with flagship locations in Silicon Valley and the New York Stock Exchange — SiliconANGLE Media operates at the intersection of media, technology and AI.

Founded by tech visionaries John Furrier and Dave Vellante, SiliconANGLE Media has built a dynamic ecosystem of industry-leading digital media brands that reach 15+ million elite tech professionals. Our new proprietary theCUBE AI Video Cloud is breaking ground in audience interaction, leveraging theCUBEai.com neural network to help technology companies make data-driven decisions and stay at the forefront of industry conversations.

AI

AI