BIG DATA

BIG DATA

BIG DATA

BIG DATA

BIG DATA

The data industry has arrived at a pivotal juncture that echoes the themes we’ve charted in previous Breaking Analysis episodes, from The Sixth Data Platform through The Yellow Brick Road to Agentic AI and Why Jamie Dimon is Sam Altman’s Biggest Competitor all the way to the Faceoff between Benioff and Nadella.

Those analyses have chronicled the steady convergence of analytic data platforms such as Snowflake and Databricks, not only with the hyperscalers’ estates, but increasingly, with the operational applications that run businesses. Our research indicates that this merger is not a side effect of generative artificial intelligence hype; rather, it’s a structural shift in how enterprises will create value from data and software over the next several decades.

In this Breaking Analysis, and ahead of Snowflake Summit next week and the Databricks Data+AI Summit the week after, we frame what in our view is the data industry’s central aim. Specifically, the race to evolve from data platform into a true System of Intelligence. Systems of Intelligence, as we have argued, are differentiated by their capacity to absorb the fragmented business logic scattered across legacy operational estates, harmonize it alongside trusted data, and expose it to agentic frameworks under human supervision.

Only when that Rubicon is crossed can enterprises consistently answer, at scale, the four enduring questions of management – that is, what happened, why it happened, what will likely happen next and, most critically, what action should be taken next?

In our research, we’ve discussed the capabilities that hyperscalers possess and the infrastructure advantage they have captured. Moreover, vendors such as Salesforce Inc., ServiceNow Inc., Palantir Inc., Celonis SE and Blue Yonder Group Inc., are actively traversing this chasm by embedding intelligence directly into workflows. Whether Snowflake Inc., Databricks Inc. and the other analytical leaders choose to do so, or instead opt to solidify their position as the, let’s call it, “neutral analytics layer,” feeding these emerging systems of intelligence is a thread that we examine throughout this research.

As we head into summit season, our premise is that platform strategy, not incremental feature wars, will separate tomorrow’s leaders from yesterday’s best-of-breed specialists. We welcome you to join us as we dissect four examples in this note, including Snowflake, Databricks, Amazon Web Services Inc. and Salesforce in terms of their architecture, how they’re extending their franchises, buoying control points and ultimately addressing board-level mandates to operationalize AI at scale.

Our view is that enterprise analytics is evolving from static, historical dashboards to a dynamic, four-dimensional digital twin that continuously senses, predicts and optimizes business performance. We believe this evolution is unavoidable if organizations expect to deploy autonomous agents with the requisite context and guardrails.

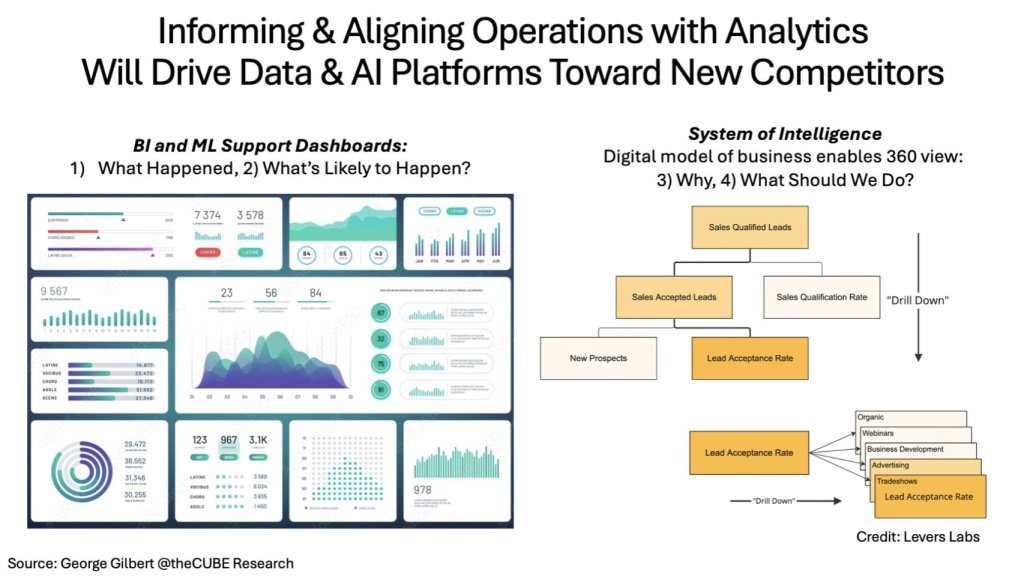

Exhibit 1 below captures the evolution. On the left we show familiar business intelligence and machine learning capabilities that answer what happened and what will likely happen. On the right, we show an interconnected metric tree that exposes causal pathways that explain why results occur and what should be done next. Such a system becomes the operational control plane for a digital business, closing the feedback loop among data, decision and action.

Exhibit 1 above shows: 1) A conventional BI/ML dashboard with color-coded KPIs, trend lines and gauges; and 2) A cascading metric tree that starts at Sales Qualified Leads, drills into acceptance and qualification rates, and ultimately traces down to channel-specific contributors such as webinars or trade shows. The right-hand graphic illustrates how linking metrics in a dependency graph enables real-time root-cause analysis and prescriptive automation.

In our view, the journey from analytics to a full-fledged System of Intelligence reframes the competitive landscape. Specifically, data-native platforms must embed operational semantics, while application vendors race to harden their data layers. The next sections will examine the architectural evolution we see and specifically how each of the four contenders we highlight in this note is positioning for this new era.

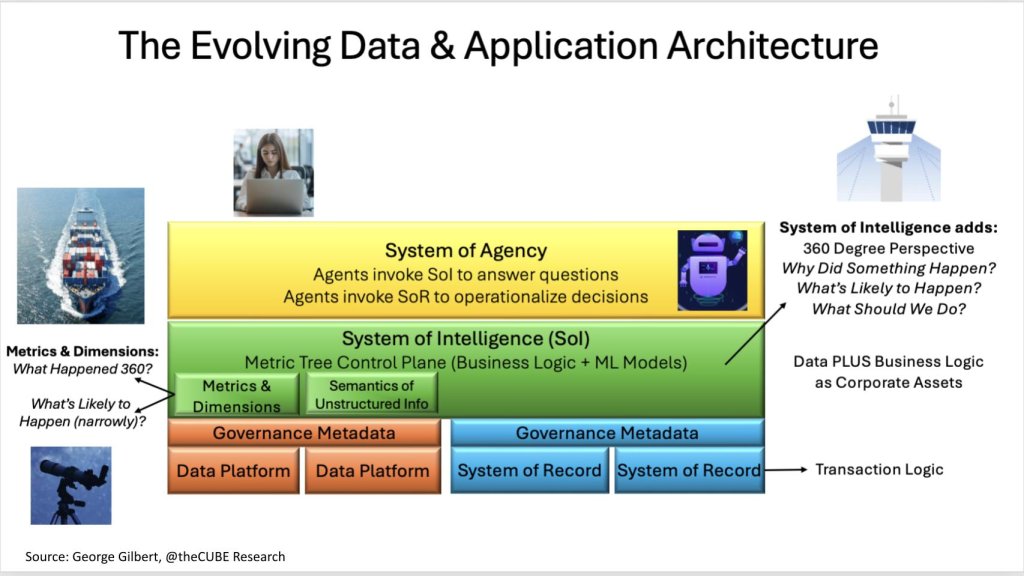

The modern data stack is splitting into three distinct areas (see Exhibit 2 below). At the base sit systems of record, the transactional engines that run finance, supply chain, commerce and customer operations. Above them emerges the system of intelligence, a metric-tree control plane that ingests data and harmonizes, data, metadata and business logic, with requisite machine learning models necessary to diagnose root causes and prescribe interventions. Topping off the picture is the emerging system of agency or SoA, where autonomous or human-assisted agents interact with the SoI for context, then invoke the systems of record to execute decisions at machine speed.

For added context on Exhibit 2, let’s dig into the stack diagram. It depicts three color-coded layers. The bottom tier (orange/blue) houses data platforms and transactional systems, governed by shared metadata. The middle green band, labeled “System of Intelligence,” embeds a metric-tree control plane that stores both metrics/dimensions and the semantics of unstructured information. The top yellow layer, “System of Agency,” shows agents querying the SoI to answer why and what should we do, then invoking systems of record to operationalize decisions.

Call-outs note that the SoI adds a 360-degree perspective and that “data plus business logic” becomes a new type of corporate assets. The small icons depict a cargo ship, a telescope and an air-traffic control tower to reinforce the journey from hindsight to foresight to real-time orchestration.

| Player | Current Position | SoI Ambition & Gaps |

|---|---|---|

| Snowflake | Metric-store hints in Cortex Agents | Needs to elevate beyond analytic artifacts; no native logic engine yet |

| Databricks | Unity Catalog + Mosaic AI | Catalog could evolve into metric tree, but relational bias persists |

| Hyperscalers (AWS, Azure, GCP) | Fabric, Redshift RA, BigQuery Studio layers forming | Deep pockets but must bridge fragmented services into one control plane |

| Application giants (Salesforce, ServiceNow, SAP, Workday) | Embedding metric trees inside SaaS domains | Advantage in domain semantics; risk of narrow scope outside core apps |

| Disruptors (Palantir, Celonis, Blue Yonder) | Already treat logic as first-class asset | Prove scalability beyond early adopter beachheads |

We believe the green layer is one of the most valuable and undeveloped pieces real estate in enterprise software – ripe for appreciation. The ones who control it will be in a stronger position to dictate the cadence at which data, models and business logic evolve and, by extension, the efficacy of every autonomous agent that sits above. Whether Snowflake, Databricks, a hyperscaler or an application incumbent claims that ground will, we believe, define the competitive order of the next decade.

Snowflake’s May print was not only an earnings release but also a line-in-the-sand declaration that the company can accelerate product innovation while maintaining operating discipline. We highlight some of the key metrics in Exhibit 3 below.

The table above summarizes product revenue, RPO, NRR, gross margin, operating margin and FY26 guidance, with Y/Y deltas and commentary (for example, bookings acceleration, AI cost absorption). The red box highlights an impressive $4.325 billion revenue guide, underscoring management’s confidence in durable mid-20s growth.

The following points of emphasis from the earnings call were noteworthy in our view:

Twelve months ago, Snowflake was barely mentioned in AI conversations within our community. Today, the company touts several Cortex wins, including at firms such as Kraft Heinz and Luminate Data. Chief Executive Sridhar Ramaswamy’s mandate to “ship faster” is showing up in release velocity and, as importantly, in customer perception. Wall Street noticed as shares popped ~14% post-print, yet remain ~50% below the euphoric 2021 peak. Snowflake has taken the opportunity to buyback shares at an average price of ~$150, well below today’s value.

We believe Snowflake’s most consequential move is not gen AI per se, rather it is the quiet build-out of a metric store that could mature into the green-layer System of Intelligence. If Cortex agents can read/write against a harmonized metric tree, Snowflake could morph from analytic powerhouse to an operational nerve center, bridging systems of record across clouds. The catch is this demands a logic-aware substrate closer to a graph or semantic model than a traditional relational catalog. Conversations with management suggests that existing primitives will suffice but we are less certain.

In our opinion, Snowflake has re-entered the AI conversation with momentum and a healthier P&L, but the true test is whether it can convert Cortex and a nascent metric store into the decisive System of Intelligence layer. Own that, and the $4 billion run rate could look small in hindsight; miss it, and Databricks, Salesforce or the hyperscalers will try to fill the void.

The market’s initial impression was Snowflake got caught flat-footed by the AI awakening. But good AI starts with quality, clean, governed, trusted data and Snowflake customers have plenty of that. As such, with focus and engineering talent, Snowflake has catapulted itself to a leading position in the AI race.

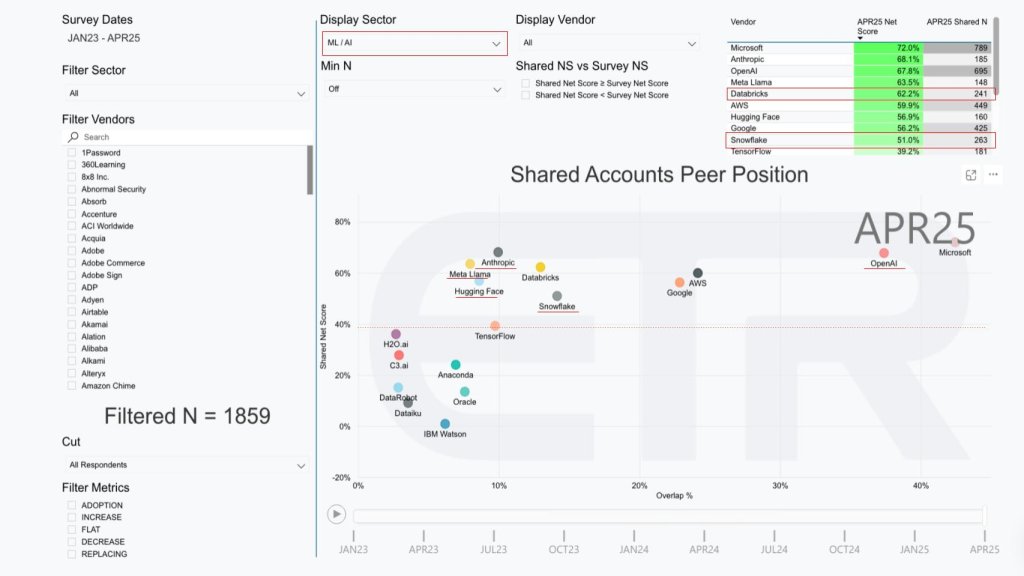

Enterprise Technology Research’s longitudinal survey provides a quarterly pulse on chief information officer spending velocity (Shared Net Score, Y-axis) and vendor footprint (Overlap %, X-axis). The latest April 2025 cut for the ML/AI sector shown in Exhibit 4 below, shows a landscape few would have predicted just 18 months ago.

The scatter plot above shows vendors by Shared Net Score (a measure of spending velocity) versus Overlap % (account penetration). A red dotted horizontal line at 40% indicates highly elevated spending momentum. Microsoft and OpenAI dominate the upper-right quadrant; AWS and Google hover just above the red line. Databricks sits high on velocity but midfield on penetration. Snowflake has climbed above the 50% velocity mark and, importantly, plots slightly farther right than Databricks, signaling broader enterprise reach.

Anthropic, Meta Llama and Hugging Face cluster nearby, evidencing the rapid mainstreaming of open-weight and foundation-model providers. Notably, none of the red underlined vendors, including Snowflake, showed up in this segment in the January 2023 survey.

The ETR data corroborates what Snowflake’s earnings hinted – that is, customers are beginning to view the platform as a credible AI destination, not merely a cloud data warehouse. Penetration gains are tangible, but to close the velocity gap with Databricks — and keep up with fast-moving foundation-model incumbents — Snowflake must industrialize its Cortex roadmap and articulate a convincing path to the System of Intelligence green layer. Moreover, we expect Snowflake to continue to double down on its simplicity ethos and focus on taking the heavy lift out of AI deployments.

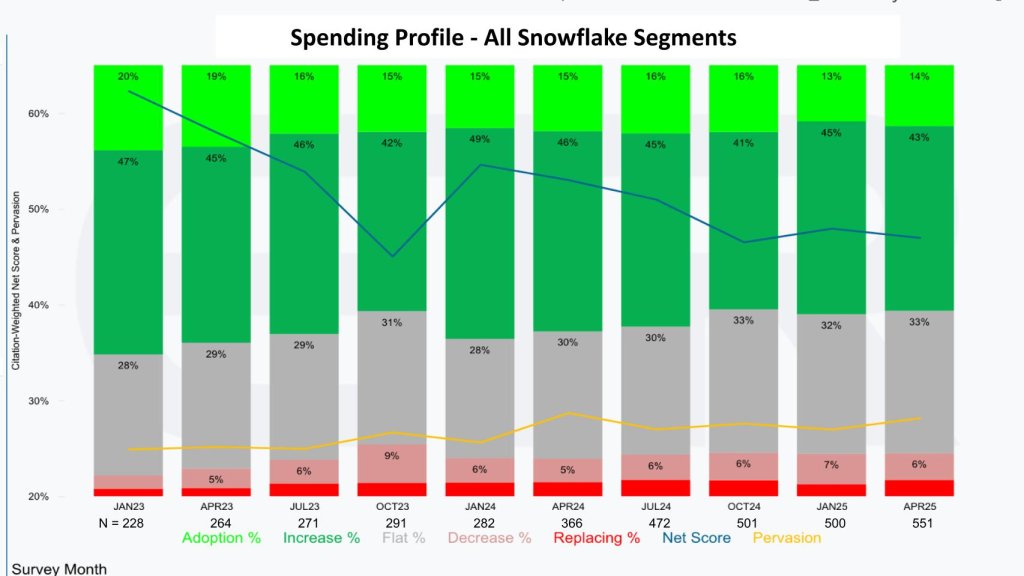

Snowflake’s engineering sprint has been supported by a material reset of its sales motions. Exhibit 5 applies ETR’s net-score-granularity lens across 11 survey snapshots (Jan 2023 to Apr 2025) and shows account spending patterns (not actual revenue but account behavior).

The blue line represents net score and descended from the mid-60s in early 2023 to a trough in Oct 2023 (~47%), then recovered to ~50% and has held comfortably above ETR’s 40% “highly elevated” watermark. The yellow penetration curve climbs steadily, mirroring the rise in N and confirming that Snowflake is touching an ever-wider slice of the enterprise universe.

Note: We believe the emphasis on new logos represented a significant change in Snowflake’s compensation model that took quite some time to materialize. Perhaps the AI awakening distracted from the effort but as shown in the following section the ETR data confirms Snowflake’s assertions about its new logo trajectory.

We believe Snowflake’s go-to-market recalibration is more than cosmetic. A maturing product portfolio, paired with compensation that rewards new logos, bookings and consumption, positions the company to sustain mid-20s growth even if macro headwinds persist. The next test will be converting those incremental logos into Cortex-driven AI consumption dollars and funneling their operational data into the still-forming System of Intelligence. If Snowflake executes on that progression, the widening yellow line could prove to be the most important curve on the chart.

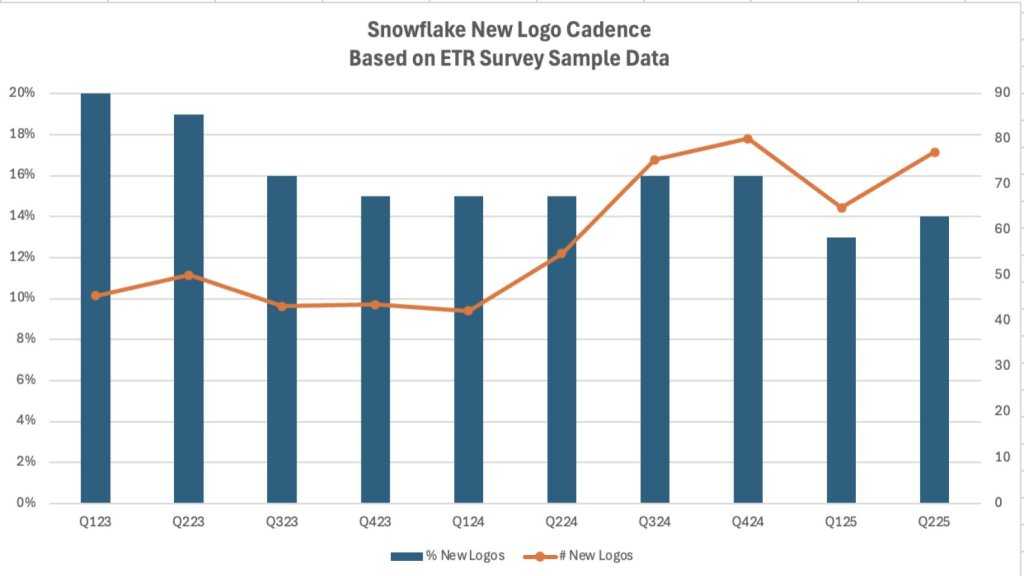

A quick but telling datapoint, Exhibit 6 below tracks Snowflake’s new-logo momentum across ten survey quarters. The blue bars represent the percentage of respondents citing Snowflake for the first time (from the Exhibit 5); the figure has held in the mid-teens. The orange line, however, calculated from absolute citation counts, shows the number of fresh logos rising sharply since Q2 2024, mirroring the rough trajectory of Snowflake’s claims.

In sum, the data corroborate Snowflake’s assertion that its revamped go-to-market engine is landing meaningful net-new accounts. We see this as an important precursor to scaling Cortex and staking a claim to the System of Intelligence layer.

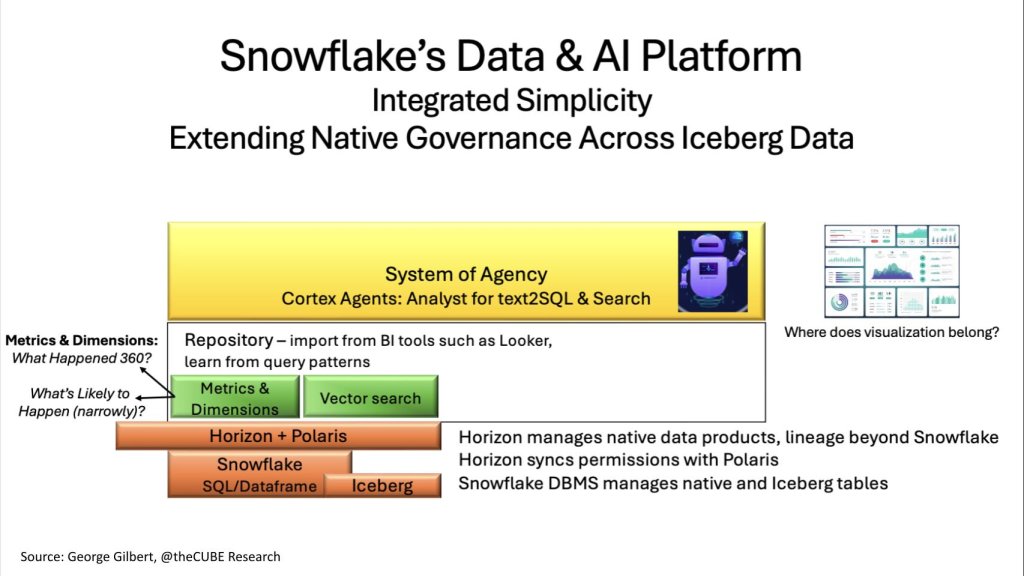

Let’s now examine Snowflake’s architectural approach in the context of the SoI/ “green-layer” challenge we put forth. Specifically its ability to weld its original cloud-native warehouse to three new pillars – that is, open-format data access, first-class governance and agentic query – all while preserving the company’s hallmark of operational simplicity (see Exhibit 7 below).

Exhibit 7: Snowflake’s Data + AI Platform Architecture

The diagram above stacks Snowflake’s layers, including Snowflake SQL/Dataframe + Iceberg at the base; a Horizon + Polaris governance bar; a white Repository box housing Metrics & Dimensions alongside Vector Search; and a yellow System of Agency band where Cortex Agents reside. Our call-outs note that Horizon syncs Iceberg permissions, Cortex supports text-to-SQL and retrieval-augmented generation, and a question mark hovers over “Where does visualization belong?”

| Architectural Element | What It Does | Why It Matters in the SoI Context |

|---|---|---|

| Horizon + Polaris Catalogs | Horizon (native) stores rich semantic, lineage, and permissions metadata; Polaris (open-source) syncs Iceberg schema & access control lists. | Source-of-truth (and control) shifts from the DBMS to the catalog. Unified governance lets Cortex agents traverse Snowflake and external Iceberg assets without security gaps or duplicate policy trees. |

| Snowflake SQL / Dataframe + Iceberg Tables | Core DBMS now manages both proprietary tables and open Iceberg partitions. | Beyond separating compute from storage. Any compute detaches from any data. Customers gain freedom to run Spark, or other transforms on Iceberg while keeping a single policy domain. |

| Metrics and Dimensions Repository | Imports Looker/BI semantic layers; enriches definitions from live query patterns. | Becomes the metric store. Structured substrate agents need to translate natural-language questions into deterministic SQL. |

| Vector Search (green block) | Stores embeddings side-by-side with rows and columns. | Enables hybrid queries that mix structured filters with semantic similarity to marry enterprise text to transactional facts. |

| Cortex Agents (System of Agency) | Cortex Analyst enables text-to-SQL on structured data. Cortex Search enables RAG on unstructured docs. | Delivers a “talk to the data” experience, but—equally important—lays the groundwork for agents that can write back actions once the SoI is in place. |

Snowflake’s architecture bets on “integrated simplicity” – that is, one policy domain, one storage fabric (proprietary + Iceberg) and one agentic interface. If the company can industrialize Horizon into a full metric tree and embed lightweight operational hooks, it will have a credible claim to the System of Intelligence, without forfeiting its performance pedigree. The alternative is ceding that green layer to Databricks, a hyperscaler or an application vendor, and watching agents treat Snowflake as just another data substrate.

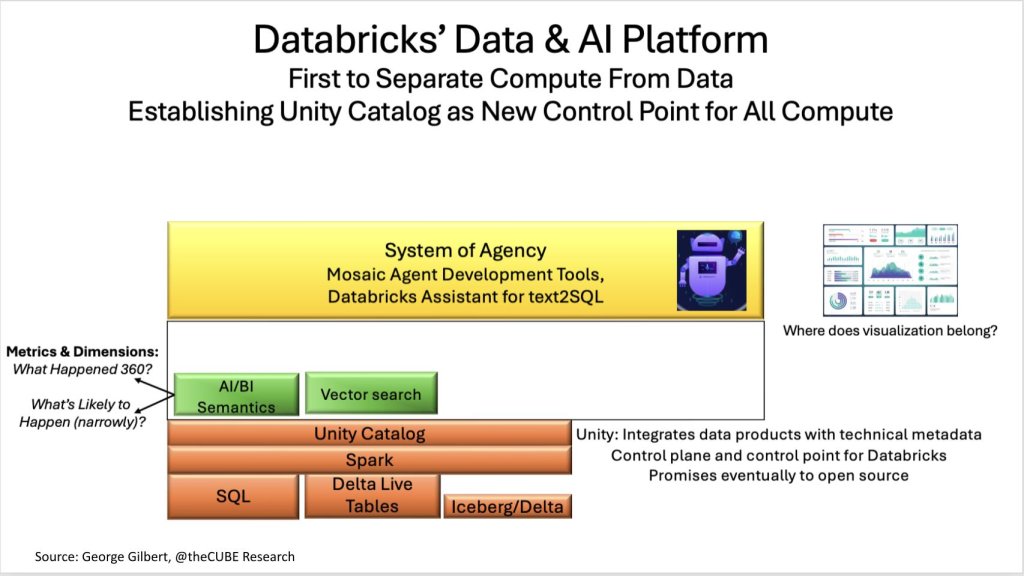

If Snowflake’s core innovation was separating compute from storage, Databricks’ contribution was to decouple any compute engine from any data format. Exhibit 8 below shows how that principle now extends further up the stack, with Unity Catalog positioned as the authoritative control point for data, models and business semantics across Spark, SQL warehouses, Delta Live Tables and external Iceberg/Delta stores.

The diagram above shows orange layers with Iceberg/Delta tables at the base, with Delta Live Tables, Spark and SQL Warehouse, with Unity Catalog bar spanning the full width. Unity being the integration point for data products and a key control point with the allure of open source. Above sits a white box for AI/BI Semantics and Vector Search (both in green), capped by a yellow System of Agency containing Mosaic Agent Tools and Databricks Assistant. Our call-out again asks, “Where does visualization belong?”

| Architectural Element | What It Does | Competitive Contrast & SoI Implications |

|---|---|---|

| Unity Catalog (standalone) | Governs schemas, lineage, permissions, and AI/BI metric definitions; promised to open-source. | Unlike Snowflake’s Horizon (nested in the DBMS), Unity is an independent service, which makes it easier to register data that never lands in a Databricks cluster. Control-plane neutrality will appeal to enterprises standardizing on Iceberg. |

| Spark + SQL Warehouse + Photon | “Any engine wins” ethos — batch, streaming, SQL, Python/Rust UDFs. | Flexibility attracts developers, but raises the bar for performance parity across engines. |

| Delta & Iceberg Tables | Databricks can now read and write Iceberg after acquiring Tabular (Ryan Blue‘s firm). | Native dual-format support removes a barrier for customers standardizing on Iceberg while preserving Delta optimizations. |

| AI/BI Semantics Layer | Combines top-down metric definitions with bottom-up learning from query patterns. | Similar goal of Snowflake’s metric store, but fully embedded in Unity and automatically version-controlled. |

| Vector Search (green) | Embeddings stored and indexed alongside structured data. | Enables hybrid queries and RAG from a single catalog. |

| System of Agency (yellow) | Databricks Assistant text-to-SQL across lakehouse; Mosaic Agent Tools – SDK + orchestrator for custom agents. | We believe Mosaic’s low-level tooling may be the most sophisticated among platform vendors, but still needs a 4-D business model to supply outcome feedback loops. |

As a private company, Databricks is more difficult to track, but the firm continues to impress in the ETR data set and in our customer conversations. Very clearly the company has a winning posture in the market with a differentiated approach from Snowflake. It continues to press the “open compute, open data” advantage, which resonates with the market.

Unity Catalog plus Tabular gives the company a credible route to becoming the enterprise’s de-facto data and model registry, irrespective of where the data lives. If Databricks can elevate Unity into a full-function metric tree and couple Mosaic agents to real-time business feedback loops, it could seize the System of Intelligence mantle. Fail to do so, and the green layer will be contested territory ripe for Salesforce, ServiceNow or an ambitious hyperscaler to occupy.

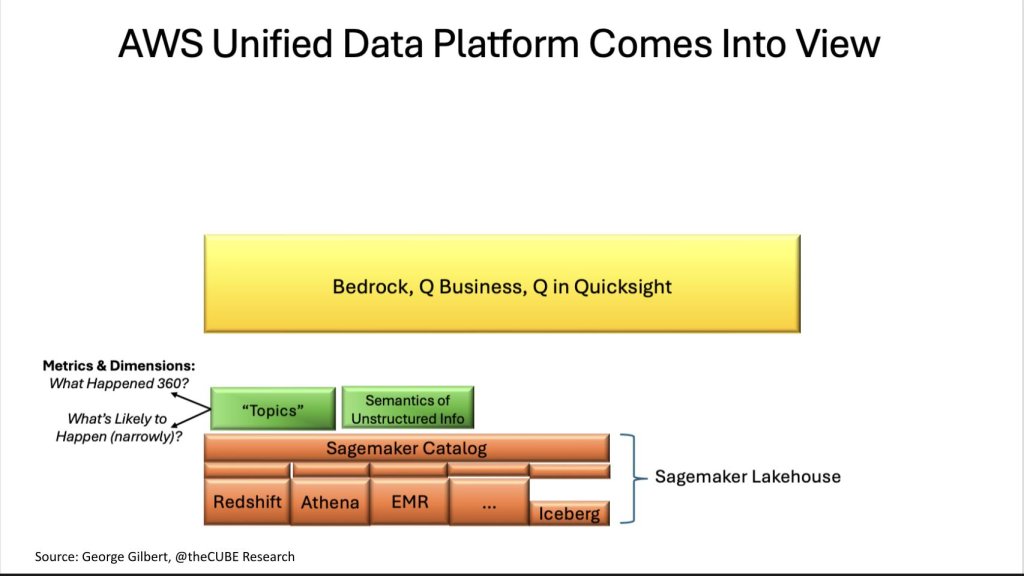

Re:Invent 2024 marked a philosophical portfolio extension for AWS in our view. After years of telling builders to assemble their own LEGO sets using primitives, the company has also integrated what were relatively independent primitives into a more integrated and accessible framework.

All the analytic data management and storage engines and governance are now all part of SageMaker. AWS integrated Redshift, Athena, EMR (Spark) and Iceberg into a cohesive framework governed by a SageMaker Catalog, based on the DataZone metadata manager, then crowned the stack with Bedrock for building agent-based applications and the Q family of LLM and agent-based services (see Exhibit 9 below).

The diagram above shows the base layers in orange with Redshift, Athena, EMR and other tooling, and Iceberg bricks under a broad SageMaker Catalog bar that serves as a unifying layer. Above that, two green blocks—Topics (metrics/dimensions) and Semantics of Unstructured Info feed a large yellow System of Agency rectangle labeled Bedrock, Q Business, Q in QuickSight. The arrows at the left annotate What happened? vs. What’s likely to happen? questions; a brace at right indicates the whole stack is an integrated “SageMaker Lakehouse,” simplifying the customer experience.

There’s more coherence even than with AWS’ first-party data management and processing engines. SageMaker has fully embraced the lakehouse architecture of open compute engines. It can join data or federate queries, not just to its own analytic engines and storage engines such as S3 Tables and Iceberg, but also to its operational database, DynamoDB, third-party analytic databases, Snowflake and BigQuery, and enterprise applications such as Salesforce and SAP.

The glue that makes these disparate data sources appear as coherent data sources is SageMaker Catalog. The catalog is where data producers and consumers meet in order to enable collaboration. Generative AI enriches the metadata in the catalog to make it easier to find, understand, and consume data. Similar to Databricks and Unity catalogs, SageMaker Catalog manages full data products such as AI models, prompts and generative AI assets. Most importantly, the catalog learns which data products are related and recommends how to use relevant ones together to accomplish tasks such as building queries or designing models.

| Architectural Element | Role in the Lakehouse | Why It Matters for a System of Intelligence |

|---|---|---|

| SageMaker Catalog (built on DataZone) | Unifies technical metadata, data-product lineage, and business “Topics” (metrics and dimensions) across all AWS analytic engines. | Becomes the control plane that insulates users from engine/file-format sprawl while inheriting AWS IAM, KMS and Lake Formation policies. |

| Redshift * Athena * EMR * Iceberg | Multiple compute engines and table formats under one roof; catalog orchestrates cross-engine joins transparently. | Marries the flexibility of primitives with a framework’s simplicity, letting agents query without knowing where, or in what format, the data resides. |

| “Topics” + Semantic Index | Business-language layer that Q services reference when translating natural language questions into SQL/Athena queries. | Topics are similar to a metric store; organizes data essential for deterministic answers to gen AI queries. Semantic index organizes vector embeddings for agent-based RAG. |

| Bedrock + Q Business/Developer + Q in QuickSight | Yellow “System of Agency” band. Bedrock is a managed service for models and supports agent development. Q chats with data; QuickSight renders rich visuals. Q is like an in-house ChatGPT. Q in Quicksight marries text2SQL with BI visualization. Q Developer is AWS’ AI engineer. | Tight coupling of ask-answer-visualize in a single console could blunt the “where does viz belong?” gap plaguing Snowflake and Databricks. |

AWS has quietly constructed a vertically integrated data-and-AI platform that rivals anything the pure-plays offer, yet with the financial, geographic and service breadth only a hyperscaler can muster. Whether SageMaker Catalog can someday matures to support a shared, causal metric tree – or remains an AWS-only operational and business catalog will determine if Amazon simply hosts the next wave of Systems of Intelligence or owns them outright. Either way, the bar for Snowflake, Databricks and SaaS incumbents just went up based on what we saw at re:Invent 2024.

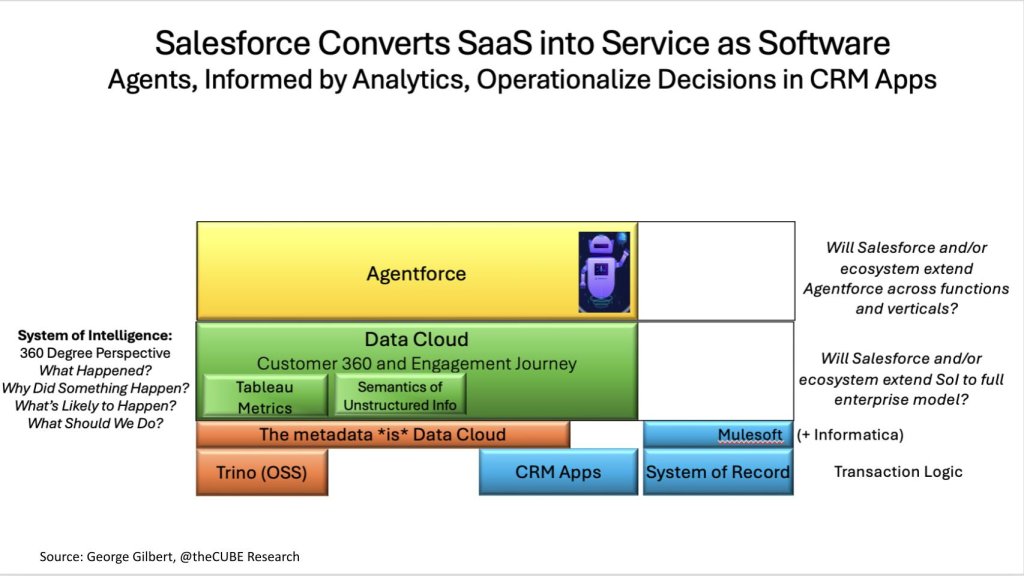

In our opinion, Marc Benioff’s end game is no longer selling cloud seats; it is monetizing the feedback loop that turns raw customer events into autonomous actions. Exhibit 10 below shows how Salesforce has inverted the classic SaaS stack – that is, Data Cloud sits in the green “System of Intelligence” band, abstracting away where data lives, while Agentforce occupies the yellow “System of Agency” layer, driving workflow back into CRM, MuleSoft APIs and third-party systems.

The base layer above shows CRM Apps (blue) next to System of Record bricks, connected via MuleSoft (+ Informatica). Above, the orange areas start with Trino, the open source query engine. That is not Salesforce’s value-add. Above Trino, the bar reads, “The metadata is Data Cloud,” meaning schema-as-code. The green Data Cloud block hosts Customer 360 and Engagement Journey plus two smaller green tiles—Tableau Metrics and Semantics of Unstructured Info. A yellow Agentforce band crowns the diagram. Right-hand call-outs pose two questions: “Will Salesforce and/or ecosystem extend Agentforce across functions and verticals?” and “Will Salesforce and/or ecosystem extend SoI to full enterprise model?”

| Architectural Element | Function | Competitive & Monetization Angle |

|---|---|---|

| Data Cloud (Customer 360 + Engagement Journey) | Harmonized 4-D model of every customer interaction, enriched by Tableau Metrics and unstructured-data semantics. | Salesforce treats metadata — not tables — as the corporate asset. Zero-copy federation queries Snowflake, Databricks and on-prem stores, lowering data-gravity friction and heading off “warehouse wars.” |

| Trino Fabric (open-source) | Executes distributed queries across remote sources. | Addresses lock-in criticism; keeps infra costs off Salesforce’s P&L while preserving governance control. |

| Agentforce | LLM-powered agents that read Data Cloud context and write back to Sales, Service, Marketing, etc. | Converts SaaS features into pay-per-outcome “Service-as-Software.” Raises the question: will pricing shift from seat licenses to usage- or KPI-based metrics? This is the new value-add layer for Salesforce. |

| MuleSoft + Informatica | MuleSoft exposes external APIs; Informatica excavates hidden logic and lineage from legacy apps/data. | Extends Data Cloud’s model beyond CRM, enabling agents to trigger actions in ERP, supply-chain or vertical stacks. Important for enterprise-wide SoI. |

We believe Salesforce is furthest along in productizing the System of Intelligence as a revenue line. By decoupling models from storage and embedding agents natively in transaction flows, the company moves from selling software to selling outcomes. We see this as a disruptive shift that could reset valuation frameworks across the SaaS sector.

The open questions are scale and scope. In other words, can the ecosystem enrich Data Cloud beyond customer-facing domains, and will enterprises stomach a usage- or value-based pricing pivot? Those answers will determine whether Salesforce merely defends its CRM beachhead or commands the green layer across the full enterprise stack.

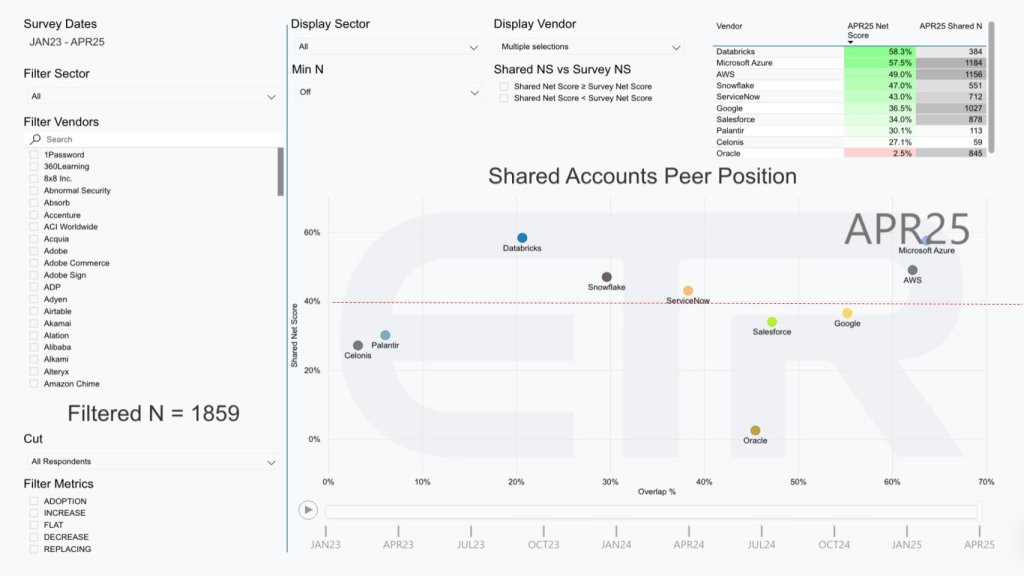

The April 2025 ETR “Shared-Accounts Peer Position” heat-map (Exhibit 11 below) lays bare the competitive board. The scatter plot below maps vendors by Shared Net Score (spending velocity Y-axis) versus Overlap % (account penetration X-axis). A red horizontal line at 40% denotes a “highly elevated” velocity. Azure and AWS cluster top-right; Databricks posts the single highest velocity among independents; Snowflake, ServiceNow, Salesforce and Google line up just above the red line; Palantir, Celonis and Oracle appear lower, signaling either niche focus or maturity.

Our research indicates enterprise data platforms are no longer defined by how, how well or how easily they store information, rather by how quickly they can convert data plus business logic into automated actions:

The journey to a full 4-D business model will take years and multiple architectural rewrites. Yet in our model, the direction is to own the metric tree, orchestrate the agents and control the enterprise operating rhythm. The next test arrives this coming week at Snowflake Summit, followed by Databricks Data+AI Summit, where each vendor will undoubtedly show – not just tell – how its green-layer ambitions translate into tangible roadmap milestones.

We’ll be on the ground on theCUBE at both events to separate aspiration from execution and will report back both live and after the dust is settles.

Support our mission to keep content open and free by engaging with theCUBE community. Join theCUBE’s Alumni Trust Network, where technology leaders connect, share intelligence and create opportunities.

Founded by tech visionaries John Furrier and Dave Vellante, SiliconANGLE Media has built a dynamic ecosystem of industry-leading digital media brands that reach 15+ million elite tech professionals. Our new proprietary theCUBE AI Video Cloud is breaking ground in audience interaction, leveraging theCUBEai.com neural network to help technology companies make data-driven decisions and stay at the forefront of industry conversations.