AI

AI

AI

AI

AI

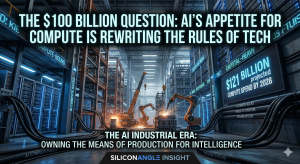

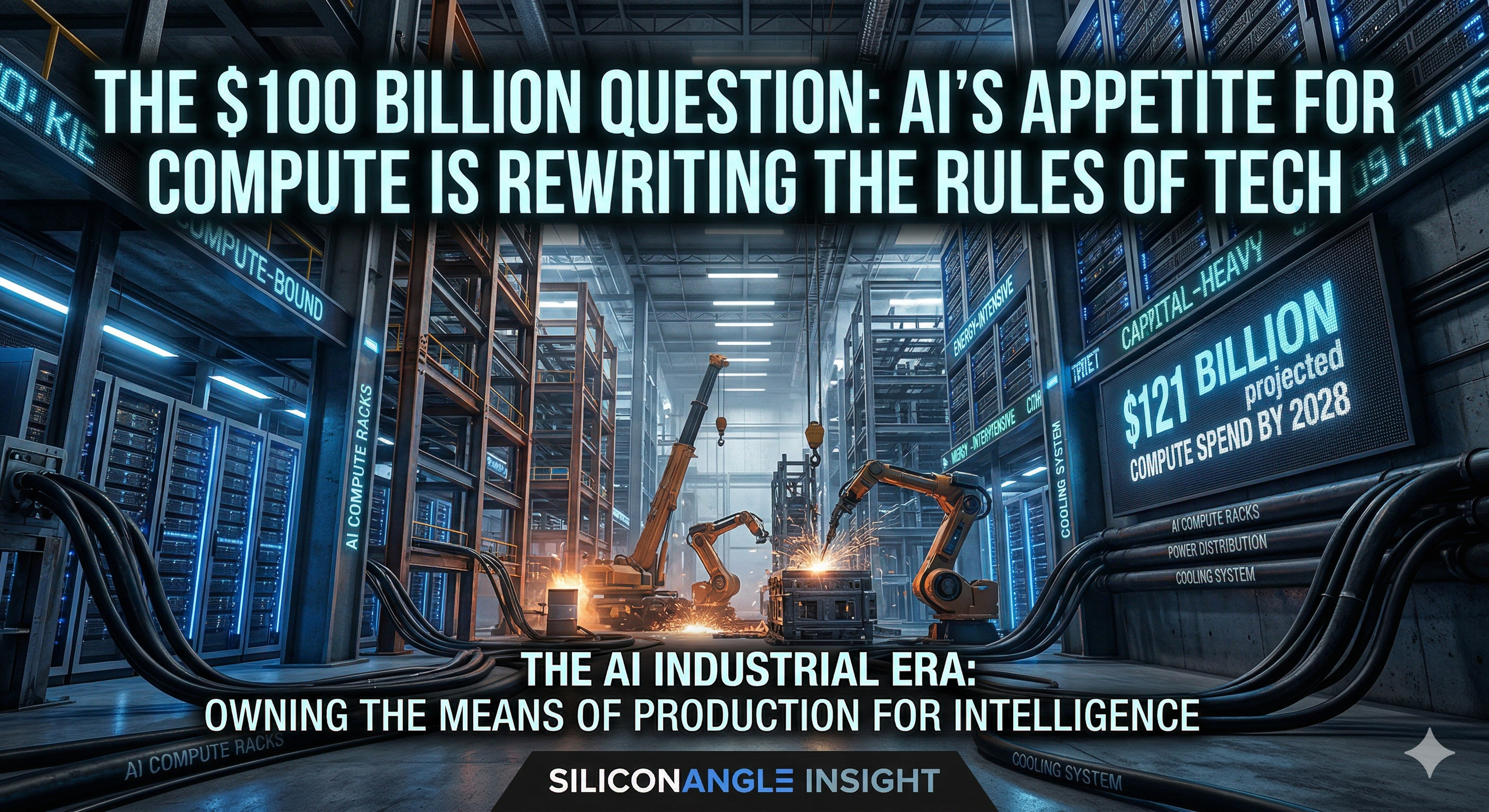

We’re hitting a pivotal moment in artificial intelligence right now. The latest financial disclosures from the front lines of the AI arms race — OpenAI Group PBC and Anthropic PBC — don’t just give us a peek under the hood; they expose the core tension shaping the entire industry. The smartest machines ever built are also the most expensive to create and operate in the history of computing.

That model is breaking. AI isn’t pure software; it’s infrastructure-as-a-service with a heavy dose of industrial-era physics. It is compute-bound, energy-intensive and capital-heavy. When OpenAI projects a staggering $121 billion in compute spend by 2028, it isn’t an outlier. It’s a signal that we have entered the era of “Infrastructure Gravity.”

Both OpenAI and Anthropic are now reporting profitability in two distinct ways: with training costs excluded, and with training costs included.

That alone should stop you in your tracks. It reveals that training costs are no longer a “R&D expense” — they are the cost of goods sold. Strip them out, and you have something that looks like software as a service. Put them back in, and you’re staring at one of the most capital-intensive industries ever created.

Annualized revenue: OpenAI ~$13 Billion | Anthropic ~$7 Billion

Valuation: OpenAI ~$300 Billion | Anthropic ~$183 Billion

Compute/training intensity: OpenAI – High (Consumer + Enterprise) | Anthropic – High (Enterprise + API)

By 2026, inference is projected to account for 65% of all AI compute, and over a model’s lifetime, it can represent 80% to 90% of total costs. We’ve seen this with GPT-4: a ~$150 million training cost ballooned into an estimated $2.3 billion in inference costs within two years. This is a 15x multiplier that software-centric VCs aren’t used to seeing.

We are seeing a clear divergence in how these giants chase the “means of production”:

If you zoom out, this starts to look familiar. We’ve seen this with Amazon Web Services Inc., Microsoft Azure and the telecom buildouts of the ’90s. Massive upfront capital, long payoff cycles and inevitable market consolidation.

The difference? Speed. AI is compressing decades of infrastructure buildout into a few years. This is why the “Big Four” hyperscalers are expected to spend more than $650 billion into capital expenditures by 2026 alone.

The game ends in one of two ways. If hardware efficiency (such as Google LLC’s TPUs or Nvidia’s Blackwell) can drop the cost of intelligence faster than demand rises, the model becomes unstoppable. If not, we are looking at massive margin compression and a brutal era of consolidation.

Don’t get distracted by the demos. In this new era, the companies that win won’t just have the best models. They’ll have the best economics. Focus on the stack: compute, cost, distribution, monetization. That’s where the $100 billion question will be answered.

Support our mission to keep content open and free by engaging with theCUBE community. Join theCUBE’s Alumni Trust Network, where technology leaders connect, share intelligence and create opportunities.

Founded by tech visionaries John Furrier and Dave Vellante, SiliconANGLE Media has built a dynamic ecosystem of industry-leading digital media brands that reach 15+ million elite tech professionals. Our new proprietary theCUBE AI Video Cloud is breaking ground in audience interaction, leveraging theCUBEai.com neural network to help technology companies make data-driven decisions and stay at the forefront of industry conversations.