INFRA

INFRA

INFRA

INFRA

INFRA

Chipmaker Nvidia Corp., the world’s most valuable company, crushed earnings expectations once again today, benefiting from massive demand for high-end artificial intelligence chips.

The company reported first-quarter adjusted earnings of $1.87 per share, well ahead of the analyst target of $1.76 per share. Revenue for the period jumped 85% from a year ago, to $81.62 billion, surpassing the analyst’s $78.86 billion consensus estimate.

Nvidia’s results have exceeded the analyst expectations that shape the market’s perceptions ever since its high-end chips emerged as the best building blocks for AI three years ago. The company’s button line has grown massively too. It reported total income of $58.32 billion at the end of the quarter, up from just $18.78 billion a year earlier.

“The buildout of AI factories, the largest infrastructure expansion in human history, is accelerating at extraordinary speed,” said Nvidia Chief Executive Jensen Huang (pictued).

Looking to the current quarter, Nvidia said it’s forecasting revenue of about $91 billion at the midpoint of its guidance range, ahead of Wall Street’s forecast of $87.39 billion.

The chipmaker has notably changed the way it reports its finances, splitting its business numbers into two market buckets: Data center and edge computing. The data center unit is by far the bigger of the two, generating total sales of $75.2 billion during the quarter, up 92% from the previous year.

As for the new edge business, that includes sales of data processing devices for agentic and physical AI, robotics and automotive chips, plus the graphics cards for personal computers and games consoles. The group delivered sales of $6.4 billion in the quarter, up 29% from a year earlier.

Prior to the AI boom, gaming has been the bigger of Nvidia’s two main businesses, accounting for more than half of its total revenue during fiscal 2020, when only 27% came from data center sales. But those numbers have now flipped, with the latter segment accounting for more than 90% of the total, while gaming was less than 8%.

On a conference call with analysts, Huang explained the decision to overhaul the way revenue is reported, saying that it will help analysts and investors to understand the company better. “It’s the simplest way of understanding our business,” Huang said. “Each one of them has different stacks in a lot of ways. They have different operating systems. They operate in a different way, and we go to market very differently in each one of them.”

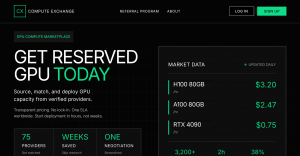

Chief Financial Officer Colette Kress told analysts on the call that the buildout of AI factories has been accelerating, causing the value of its infrastructure to rise significantly over the last few months. The price of renting an H100 graphics processing unit has increased 20% in the year to date, while A100 cloud pricing has risen almost 15% over the same timeframe. She added that customers are continuing to generate profitable revenue streams beyond the depreciable life of their GPUs.

Results from the data center business were broken down into two segments. Hyperscaler cloud providers accounted for more than half of all data center sales at more than $38 billion, Kress said. The other $37 billion is tied to the new AI clouds, industrial and enterprise markets segment, now known as ACIE, and saw revenue triple year over year.

Huang also talked about the early demand for its next-generation rack-scale system for AI, called Vera Rubin, and promised that it will be “even more successful than Grace Blackwell,” which is the company’s existing system for data center installations. He said he’s confident about this because the company is “growing share in inference very, very quickly,” as the number of companies developing frontier models grows. He said Anthropic PBC has become a key customer this year.

The Vera Rubin system is comprised of 1.3 million components, including 72 Rubin GPUs and 36 Vera central processing units. Nvidia says it delivers 10 times more performance per watt than its predecessor.

Meanwhile, Kress said, Nvidia isn’t satisfied with only being the world’s GPU king, and also wants to become the “leading CPU supplier” as well. It’s an area that’s currently dominated by rivals such as Intel Corp. and Advanced Micro Devices Inc.

However, the new Vera CPUs have opened a “brand new $200 billion tab” for the company, she said. “Every major hyperscale and system maker is partnering with us to get it deployed,” she said, adding that she anticipates CPUs will generate about $20 billion in sales this year.

Until now, Nvidia’s domination of the AI market has been exclusively led by sales of its GPUs, which excel at the parallel math required to train large language models. But as agentic AI automation becomes increasingly important, CPUs are enjoying a resurgence.

Nvidia also sells a new, custom Groq language processing unit and an entire data center rack filled with those new chips, called LPX. It’s a kind of application-specific integrated circuit or ASIC, which is a low-powered chip that can be programmed to power specific computing tasks. It’s similar to the custom AI chips sold by Nvidia’s cloud customers and rivals, including Amazon Web Services Inc. and Google Cloud. Huang said he has high hopes for the Groq chips, but told analysts it will likely remain a “niche product” for some time to come.

“LPX is designed for low latency and high token rate, but its throughput is low,” Huang said. “The use case for LPX is not broad.”

Another ASIC maker is Cerebras Systems Inc., which made a blockbuster debut on the public markets last week in what was interpreted as a clear signal that the AI market is hungry for alternatives to Nvidia’s chips.

Holger Mueller of Constellation Research said two of the standout aspects of its quarter had nothing to do with its technology, but rather the discipline of its management. He was especially impressed by Nvidia’s cost control measures, which helped it to squeeze out billions in additional profit. “One year ago, Nvidia was able to extract $1 of net income for every $2.5 in revenue it earned, but today it’s earning $1.40,” the analyst pointed out. “That’s a remarkable advance in profitability for such an established company. But this is a very different Nvidia.”

The analyst also pointed out the profits derived from Nvidia’s investments in startups and other financial activities, which contributed to an $11.5 billion jump in its bottom line. “These activities don’t come for free, as the company used five-times as much cash as it did one year ago on investments, and approximately 40% more financing,” Mueller said. “That means that it has lower free cash than one year ago. It’s not a big concern, but it does underscore how this company has changed. The question now is how long can Nvidia keep growing at this level? All eyes are on the Vera Rubin delivery in the second half of the year.”

Despite Nvidia’s impressive results, the company’s stock was more or less flat in extended trading, with many investors hoping for an even more stellar performance. Privately, a lot of market watchers are nervous about a comedown for the chipmaker following a multiyear boom that has seen its market capitalization surge from $400 billion at the end of 2022 to over $5.4 trillion today.

EMarketer analyst Jacob Bourne said the inevitable earnings beat has already been priced in before the results were announced, hence the muted reaction to the report.

“The lingering question is whether it can convince investors the AI buildout has durability into 2027 and 2028, especially as the narrative shifts toward inference workloads and competing silicon from Google, Amazon, AMD and Intel,” he said. Nvidia’s strategy of investing across the AI supply chain is helping to entrench its position, but skeptics worry about how much of that demand is organic versus propped up by Nvidia’s own balance sheet.

“Time and time again, Nvidia obliterates expectations and consensus; it delivered exactly on what people wanted, especially regarding data centers,” said David Wagner of Aptus Capital Advisors. “But the market doesn’t always act as you would expect after a strong report like this one.”

The company also announced plans to return some money to shareholders. It authorized a plan to buy back $80 billion worth of stock and increased its quarterly cash dividend to 25 cents per share from one cent.

Support our mission to keep content open and free by engaging with theCUBE community. Join theCUBE’s Alumni Trust Network, where technology leaders connect, share intelligence and create opportunities.

Founded by tech visionaries John Furrier and Dave Vellante, SiliconANGLE Media has built a dynamic ecosystem of industry-leading digital media brands that reach 15+ million elite tech professionals. Our new proprietary theCUBE AI Video Cloud is breaking ground in audience interaction, leveraging theCUBEai.com neural network to help technology companies make data-driven decisions and stay at the forefront of industry conversations.