BIG DATA

BIG DATA

BIG DATA

BIG DATA

BIG DATA

Splunk Inc. beat analyst revenue and earnings-per-share estimates in its first fiscal quarter and raised its outlook for the full year, but it wasn’t good enough for investors.

A slowdown in the company’s overall growth rate and a small decline in new-customer growth sent its shares down nearly 4 percent in immediate after-hours trading. Update: On Friday, shares fell nearly 7 percent.

First-quarter total revenues of $242.4 million actually matched Splunk’s previous estimate before the company lowered expectations when it last reported quarterly earnings. Analyst consensus estimates were $233.9 million. The quarterly loss of one cent per share was at the high end of analyst estimates and ahead of consensus estimates of a loss of four cents.

The company, which sells cloud-based software for analyzing real-time, machine-generated data such as clickstreams and computer network activity, modestly raised full-year billing estimates to $1.425 billion from $1.4 billion and upped revenue expectations to $1.195 billion from its earlier guidance of $1.185 billion. Operating margin estimates of 8 percent were unchanged.

Splunk said it signed “nearly 500 new enterprise customers,” in the quarter, which would indicate a decline from new-customer acquisition of 500 customers in the first quarter of each of the last two years. The slowdown may explain the after-hours share decline. “Anything less than 500 new customers may be viewed as a disappointment and indicate turbulence in the transition of smaller accounts to the third-party sales channel,” wrote Frank DiPietro in an pre-earnings analysts on The Motley Fool. “It could also signal that Splunk’s own sales team is slowing down in adding larger accounts.”

Executives said more than 80 percent of quarterly bookings came from existing customers, but it’s still on track to reach 20,000 customers in fiscal 2020, up from 13,000 currently. Splunk recorded 358 orders of greater than $100,000 in the quarter, reflecting its continued reliance on license sales.

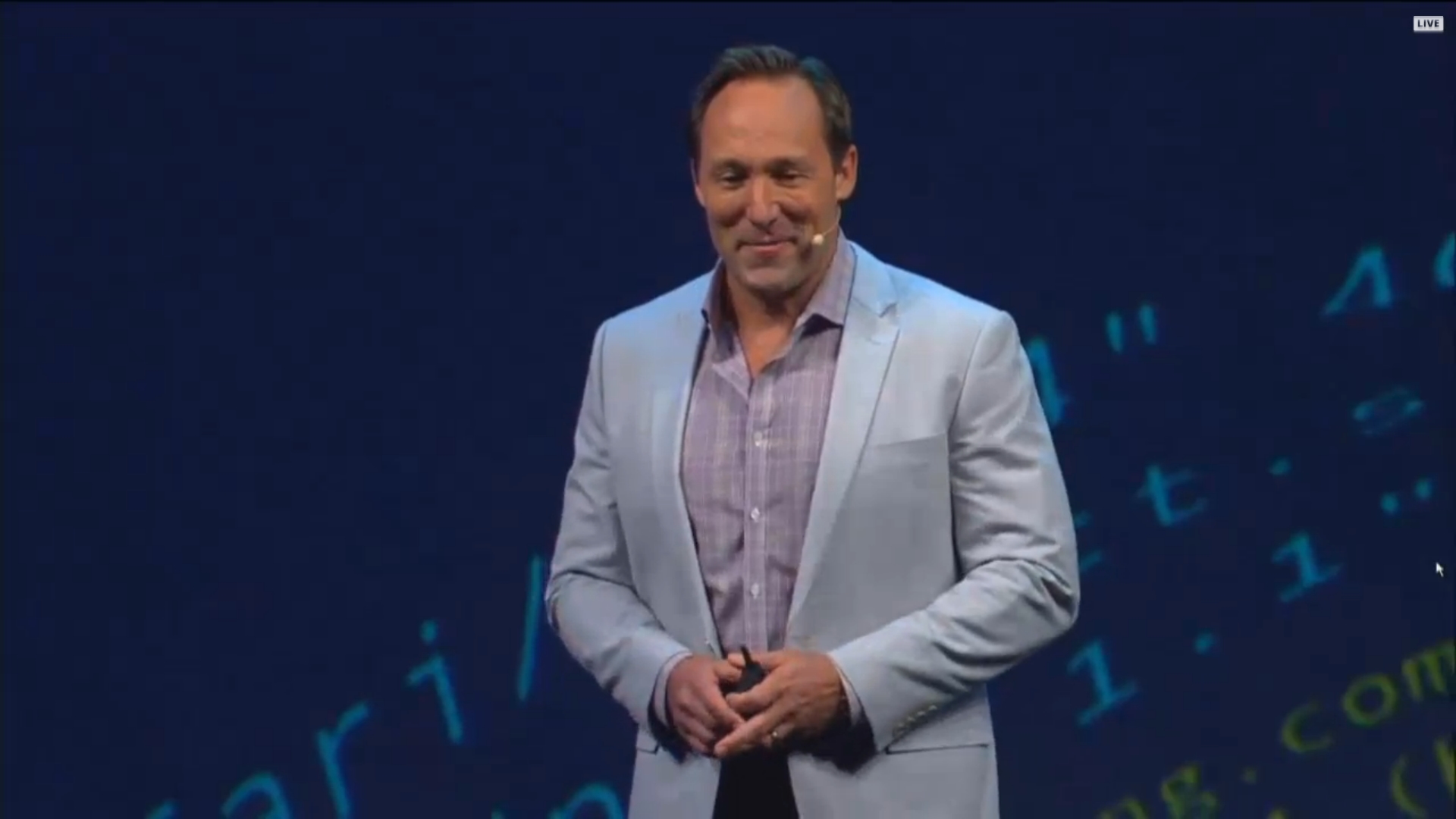

That’s a problem as well as a virtue, however. Splunk is facing aggressive expectations on both customer growth and cloud strategies. The company was late in moving to a cloud subscription model and has been struggling to make up for lost time. It’s cloud business doubled year-over-year to $17.7 million in the quarter. “Our cloud business continues its momentum,” said Chief Executive Doug Merritt (pictured).

However, Merritt and Chief Financial Officer David F. Conte faced pressure on the company’s earnings call to explain the impact of cloud subscriptions gross margins, deferred billings and the company’s overall growth rate. Splunk has said it expects to be a $2 billion company by 2020. “As cloud continues to grow it’s going to be a drag on the license line,” Merritt said. “When you look at the growth of deferred revenue, the biggest impact is the growth in cloud.” The good news is that cloud customers are more loyal and spend more over time, he said.

Executives did indicate some turmoil on the sales side, particularly as the transition to cloud subscriptions makes an impact on sales commissions. Weaker-than-expected results in the Europe, Middle East and Africa were the consequence of management problems, for which the company has initiated a “leadership change,” Merritt said.

Support our mission to keep content open and free by engaging with theCUBE community. Join theCUBE’s Alumni Trust Network, where technology leaders connect, share intelligence and create opportunities.

Founded by tech visionaries John Furrier and Dave Vellante, SiliconANGLE Media has built a dynamic ecosystem of industry-leading digital media brands that reach 15+ million elite tech professionals. Our new proprietary theCUBE AI Video Cloud is breaking ground in audience interaction, leveraging theCUBEai.com neural network to help technology companies make data-driven decisions and stay at the forefront of industry conversations.