INFRA

INFRA

INFRA

INFRA

INFRA

Semiconductors are at the heart of technology innovation. For decades, technology improvements have marched to the cadence of silicon advancements in performance, cost, power and packaging.

In the past 10 years, the dynamics of the semiconductor industry have changed dramatically. Soaring factory costs, device volume explosions, fabless chip companies, greater programmability, compressed time to tape-out, more software content, the looming Chinese presence — these and other factors have permanently changed the power structure of the semiconductor business.

We rely on chips for every aspect of our lives, which has led to a global semiconductor shortage that has affected more industries than we’ve ever seen. Our premise is that silicon success in the next 20 years will be determined by volume manufacturing expertise, design innovation, public policy, geopolitical dynamics, visionary leadership and innovative business models that can survive the intense competition in one of the most challenging businesses in the world.

In this Breaking Analysis, it’s our pleasure to welcome Daniel Newman, one of the leading analysts in the technology business and founder of Futurum Research. As always, we’ll bring in spending data from Enterprise Technology Research, provide our opinions on what the data tells us and get Daniel’s input on the major trends.

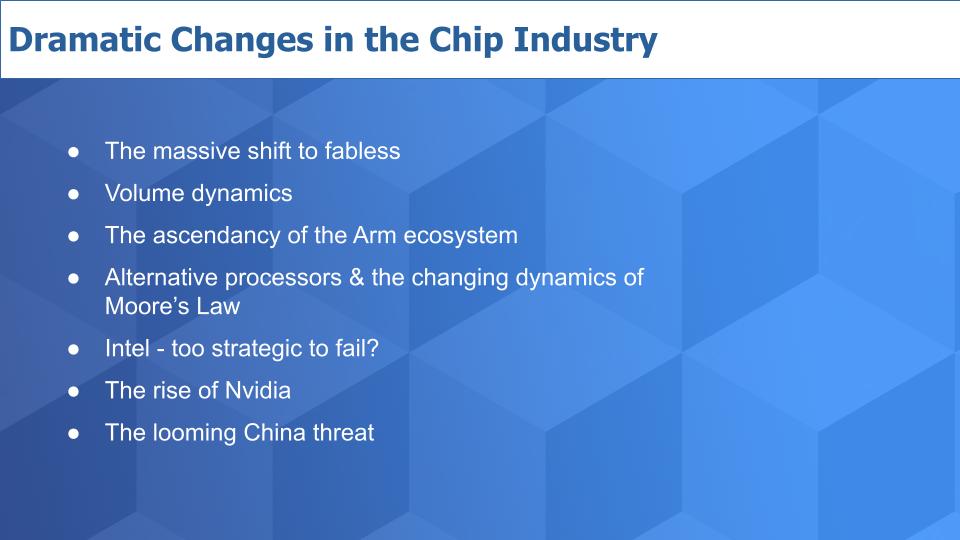

Above are some of the topics we’ll cover with Daniel.

The changes in the semiconductor industry have been epic and appear to be lasting. The shift to no-fab chip companies and the volume manufacturing impacts (thanks largely to Arm Ltd.’s model) are notable. We want to cover Intel Corp.: What does it have to do to survive and thrive the changes in its business? We’ll discuss how alternative processors are impacting the world: Is Moore’s Law dead? Is it alive and well? Daniel has strong perspectives on these topics, including Nvidia Corp., and we’ll get his thoughts on all of this, plus talk about the looming China threat in semis.

Here’s how Daniel Newman sees the industry at a macro level:

There are a lot of different narratives that are streaming alongside, and they’re not running in parallel so much as they’re running and converging towards one another. So the last two years has welcomed a semiconductor conversation that we really hadn’t had, and that was supply chain-driven. The COVID-19 pandemic brought pretty much unprecedented desire, demand, thirst for products that are powered by semiconductors. And it wasn’t until we started running out of laptops, of vehicles, of servers, that the whole world kind of put the semiconductor in focus again.

We, as a society, took for granted that if you need a laptop, you go buy a laptop. If you needed a vehicle, there’d always be one on the lot. But as we’ve seen kind of this “exponentialism” that’s taken place throughout the pandemic, what we ended up realizing is that semiconductors are eating the world. And in fact, the entire industrial complex is powered by semiconductor technology.

You went from a vehicle that might’ve had $50 or $100 worth of semiconductors on a few different parts to one that might have 700, 800 different chips in it. Thousands of dollars worth of semiconductors. So, across the board, you’re dealing with the dynamics of the shortage. You’re dealing with the dynamics of innovation. You’re dealing with Moore’s law sort of coming to the end, which is leading to new process.

We’re dealing with the foundry versus fab versus invention, and product development situations. So there are so many different concurrent semiconductor narratives that are going on and we can talk about any of them and all of them.

By way of background we re-introduce the concept of Wright’s Law. We all know about Moore’s Law but the earlier instantiation actually comes from Theodore Wright.

T.P. Wright was an aeronautical engineer. He applied the above math, which is a bit abstract, to make observations and conclusions about the cost of manufacturing airplanes. Roughly translated, it says that as the cumulative number of units produced doubles, your cost per unit declines by a fixed percentage.

In airplanes, that was around 15%. In semiconductors, we think that number is more like 20% to 25%… and when you add in the performance improvements you get from silicon advancements, it translates into something like 33% cost declines. That’s very important and confers strategic advantage to the company with the largest volumes. This is especially relevant when manufacturing a next generation of product, which is always more expensive at the start.

As the cumulative number of units produced doubles, your cost per unit declines by a fixed percentage.

Wright’s Law describes a learning-curve dynamic. Like Amazon.com Inc. Chief Executive Andy Jassy often says, there’s no compression algorithm for experience. It applies here and applies in semiconductors – big-time. If you apply Wright’s Law to what’s happening in the chip industry today, you can gain a better understanding of why Taiwan Semiconductor Manufacturing Corp. is dominating and why Intel is struggling.

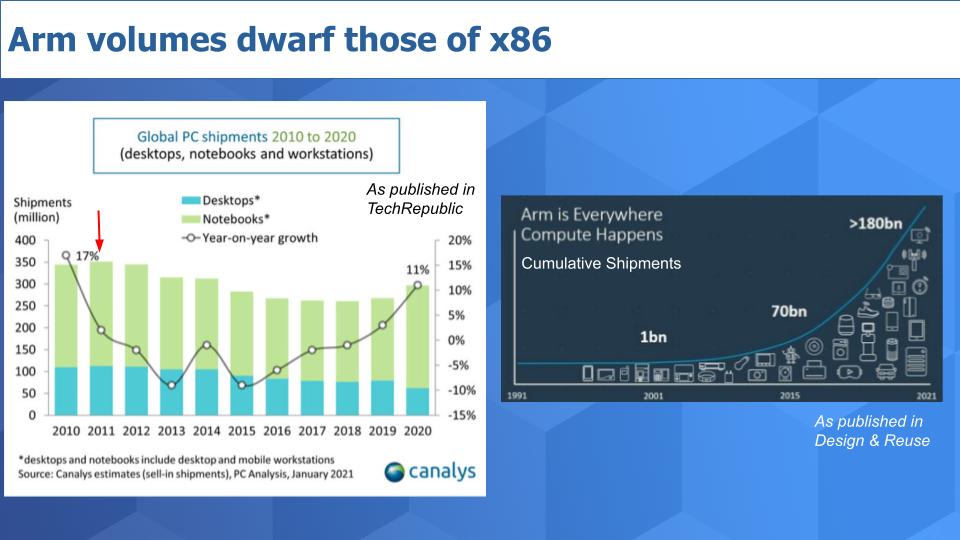

Arm wafer volumes are exploding and x86 wafer volumes are not.

Let’s introduce the supporting data and then we’ll bring Daniel in to add his views.

Very simply, the chart on the left above shows personal computer shipments, which peaked in 2011 and began a steady decline – until COVID – they’ve popped up in the past year and will be up again this year, but marginally in the grand scheme of things.

The chart on the right is cumulative Arm shipments. As we’ve reported, we think Arm wafer volumes are 10 times those of x86 volumes and, as such, the Arm ecosystem has a far better cost structure than Intel’s and that’s why Pat Gelsinger was called in to save the day.

Just as PC volumes enabled Intel to capitalize on Wright’s Law, we see Arm enjoying similar benefits.

Daniel Newman shares his thoughts on volume economics in this video clip.

What I will say about that is, we have certainly seen this, this fabless model explode over the last few years. You’re seeing companies that can focus on software, frameworks, and innovation that aren’t getting caught up in dealing with the large capital expenditures, and overhead. The ability to, as you suggested in the topics here, partner with a company like Arm, that’s developing innovation and then offering it to everybody.

And for a licensee, they can quickly build. We’re seeing what that’s doing with companies like AWS, that are saying, we’re going to just build it. Alibaba too. And others. We’re just going to build it. These are companies that were never considered chip makers, they are now today competing as chipmakers. So there’s a lot of different dynamics, going back to your comment about Wright’s law. Like I said, as we normalize, and we figure out the supply and demand situation on a global scale, I do believe that, those who can manufacture the most will certainly continue to have significant competitive advantages.

Daniel Newman further comments in this clip on the impact of the chip shortage and Intel’s opportunity to “repatriate” production to the United States. Importantly, he provides insights into the complexities of solving the supply demand imbalance and Intel’s motivations.

The bottom line is the chip shortage and the strategic importance of onshore manufacturing could buy Intel some time to right the ship.

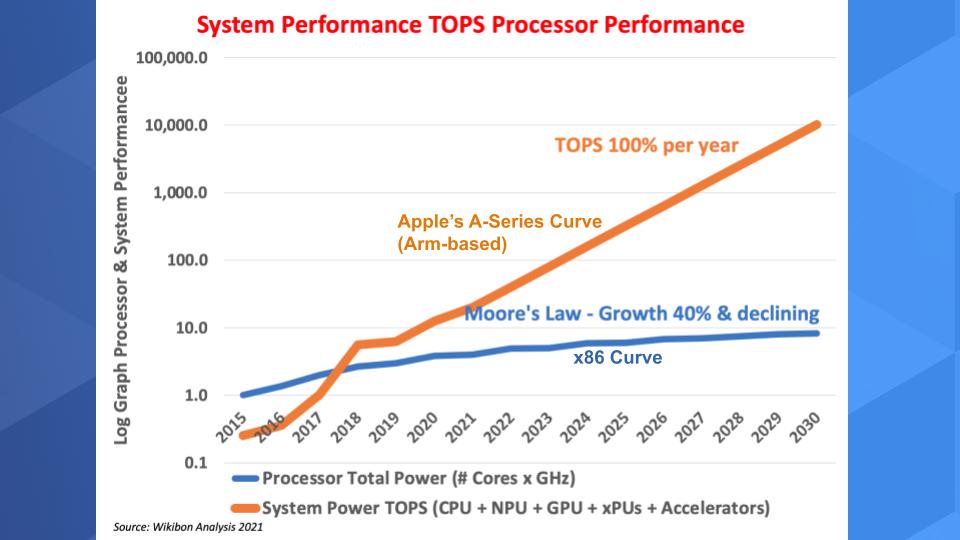

One of the things we often talk about is the way in which alternative processors have exploded onto the market. And this chart below speaks to the advantages that Arm enjoys. Intel is responding by both outsourcing some of its manufacturing but also once again entering the independent foundry business. That is, getting serious about manufacturing non-Intel chips in its facilities.

What this chart above shows is performance curves on a log scale. The blue line shows the historical x86/Moore’s Law progression. The orange line is derived from Apple’s A-series chip performance progression over time, culminating in the most recent A-15 chip. The data measures performance in trillions of operations per second.

The traditional x86 curve of doubling every 18-24 months – or about 40% improvement per year – is moderating to around 30% per year. The orange line, powered by Arm, is growing at 100%-plus per year when you combine the central processing units, network processing units, graphics processing units and alternative processing units.

We’re seeing Apple Inc. use Arm, Amazon Web Services Inc. is building Graviton on Arm, Tesla Inc. is using Arm…the list is long and this is one reason why.

Daniel Newman comments on the changing dynamics of Moore’s Law in this clip.

We are certainly in an era where companies are able to take control of the innovation curve, using the development and the open ecosystem of Arm, having more direct control and price control. And of course, part of that massive Arm number has to do with mobile devices and IoT, and devices that have huge scale. But at the same time, a lot of companies have made the decision either to move some portion of their product development on Arm, or to move entirely on Arm. [It’s] part of why it was so attractive to Nvidia, part of the reason that it’s under so much scrutiny, (i.e. that acquisition) – whether that deal will end up getting completed remains to be seen. But we are seeing an era where we have a lust for power. I talked about lust for semiconductors, our lust for our technology to do more, whether that’s software-defined vehicles, whether that’s the smartphones we keep in our pocket or the desktop computer we use, we want these machines to be as powerful and fast and responsive and scalable as possible.

If you can get 100% versus 30% improvement with each year in a next generation, what is the consumer going to want? So I think companies are following the normal demand of consumers based on what’s available. And at the same time, there’s some economic benefits they’re, they’re able to realize as well.

In March of this year we published this article where we addressed that precise question.

In the piece, we talked about the multi-front war Intel is waging with Advanced Micro Devices Inc., the Arm ecosystem, TSMC, other design firms and China. We attempted to analyze the company’s moves, which seem to be right from a strategy perspective. But Intel can only move so fast. We discussed the potential impact of the U.S. government’s assistance, Intel’s partnerships with IBM Corp. and what that might portend, how the U.S. government has a huge incentive to make sure Intel wins with onshore manufacturing… and the looming threat from China.

We asked Daniel Newman: Is Intel too strategic to fail and is Pat Gelsinger making the right moves?

First of all, I do believe that this current juncture, where the semiconductor and supply chain shortage and crisis still looms, that Intel is too strategic to fail. I also believe that Intel’s demise is somewhat overstated. Not to say Intel doesn’t have a slate of challenges that it’s going to need to address long-term, just with the technology adoption curve that you showed being one of them, Dave, but you have to remember, the company still has nearly 90% of the server CPU market. It still has a significant market share in a client and PC. It is seeing market share erosion, but it’s not happening nearly as fast as some people had suggested it would happen, with right now with the demand in place, and as high as it is, Intel is selling chips just about as quickly as they can make them.

And so we are sort of seeing the TAM as a whole, demand as a whole, continue to expand. And so Intel is fulfilling that need, but where are they really too strategic to fail? I mean, we’ve seen in certain markets, in client for instance, where AMD is gaining. Of course, that’s still x86. We’ve seen where the M1 was kind of initially thought to be potentially a product that would take some time. It didn’t take nearly as long for them to get that product in good shape, but the foundry and fab side is where I think Intel really has a chance to flourish right now.

First, it can play in the Arm space. It can build these facilities to be able to produce, and help support the production of volumes of chips, using Arm designs. So that actually gives Intel inroads.

Two is [that] the company that has made the most outspoken commitment to invest in the manufacturing needs of the industry, both here in the United States, and in other places across the world where we have friendly ally relationships, and need more production capabilities, And there is no other logical company that’s U.S.-based, which is going to meet the policymakers requirements right now; and is also raising their hand, and saying, we have the know-how we’ve been doing this. We can do more of this.

And so I think Pat is leaning into the right area. And I think what will happen is, very likely Intel will support manufacturing of chips by companies like Qualcomm, companies like Nvidia. And if they’re able to do that, some of the market share loss is that they’re potentially facing with innovation challenges and engineering challenges could be offset with growth in their fab, and foundry businesses. And I think Pat sees this clearly. I think he’s going to market with it and, you know, convincing the street, that’s going to be a whole different thing. But I think as the Street sees the opportunity here, this is an area that Intel can really lean into.

The other big question we want to test with Daniel is will Arm (and Nvidia) be able to seriously penetrate the enterprise– that is, the server business. Clearly Nvidia wants to own the datacenter.

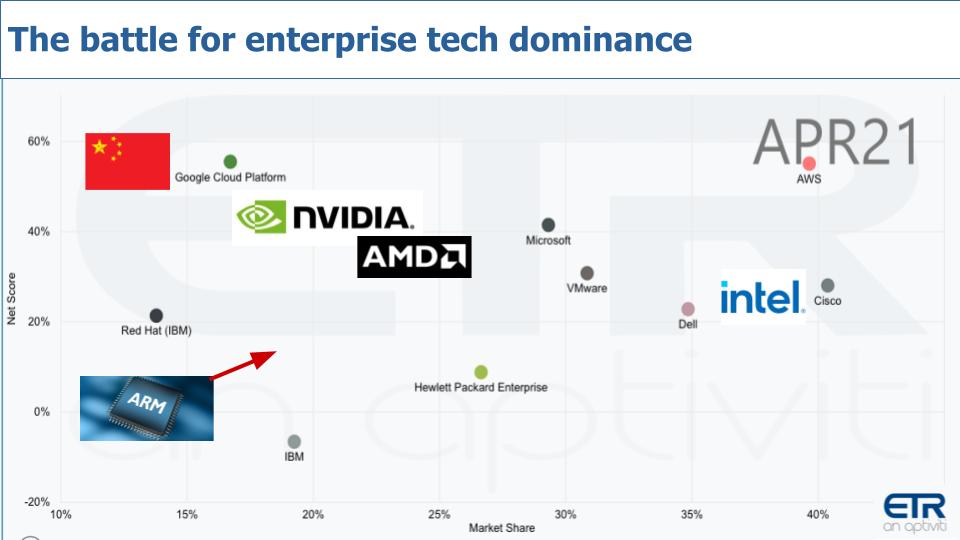

This data above from ETR lays out many of the enterprise players. And we’ve superimposed the semiconductor giants on the chart.

The data shows an X/Y chart with Net Score or spending momentum on the Y axis and Market Share or presence in the survey on the X axis. As we’ve reported before, AWS is leading the charge in enterprise architecture with Nitro and Graviton. Microsoft Corp. is following suit, as is Google. VMware Inc., Cisco Systems Inc., Dell Technologies Inc., Hewlett Packard Enterprise Co. and IBM with Red Hat are shown on the chart. And we’ve superimposed Intel, Nvidia, China and Arm.

Now we can debate the position of the logos but we know that: 1) Intel has a dominant position in the datacenter and must protect that business. It cannot lose ground as it has in PCs because of the margin pressure it would face; 2) We know AWS, with its Annapurna acquisition is trying to control its own destiny; 3) We know VMware has Project Monterey and is following AWS’ lead to support new workloads beyond traditional x86 general purpose apps, in partnerships with Pensando Systems Inc., Arm and others; and 4) We know Cisco has chip design chops – as does HPE to a lesser extent and of course we know IBM has excellent semiconductor design expertise, especially related to memory disaggregation and its years of experience in the business.

We also know Nvidia has plans to go hard after the data center. We know China wants to control its own destiny and then there’s Arm. It dominates mobile and the “internet of things.” We believe it make a play for the data center, especially with offloading storage, networking and security work at a lower cost.

Here’s how Daniel Newman sees the picture.

It’s going to take some time, I believe, but some of the investments, and products that have been brought to market in, in you mentioned that shorter tape out period, that shorter period for innovation, whether it’s Graviton on AWS or the AI/ML chips that, with Trainium, and Inferentia, how quickly AWS was able to develop, build and deploy to market an Arm-based solution that is being well-received and becoming an increasingly important component of the services and products that are being offered from AWS.

At this point, Arm is still pretty small. And I would suggest that Nvidia and Arm, in the spirit of trying to get this deal done, probably don’t want the enterprise opportunity to be overly inflated, as to how quickly the company is going to be able to play in that space, because that could somewhat slow or bring up some caution flags for regulators.

At the same time, you could argue that Arm offering additional options, and competition much like it’s doing in client, will offer new form factors, new designs, new SKUs. The OEMs will be able to create more customized hardware offerings, that might be unique for certain enterprises. We’re seeing the disaggregation with DPUs and how that technology using Arm, with what AWS is doing with Nitro, but also what these different companies are doing with semiconductor technology to split out security, networking and storage. And so you start to see design innovation could become very interesting on the foundation of Arm. So in time I certainly see momentum.

But as we continue to grow up, and you see these different processes, these different companies, Nvidia, AMD, Intel, all seen as very worthy companies with very capable technologies in the data center. If they can offer economics, if they can offer performance, if they can offer faster time to value, people will look at them. So I’d say in time, Dave, the answer is Arm will certainly become more and more competitive in the data center, like it was able to do at the edge and in mobile.

We know that China wants to be self sufficient in semiconductors and is investing in fab capacity. It’s building out NAND capabilities and we believe will continue to move up the value chain.

Here’s how Daniel Newman sees China in semiconductors:

Taiwan and China are very physically close together. And the way that China sees Taiwan and the way America sees Taiwan is completely different. We have very little control over what can happen. We’ve all seen what’s happened with Hong Kong. So there’s just so many trains on the track. They’re all moving, but they’re not in parallel. These tracks are all converging, but the convergence isn’t perpendicular. So sometimes we don’t see how all these things interrelate.

I would never count China out of anything. If they put their mind to it, if it’s something that they want to put absolute focus on. I think right now, China vacillates between wanting to be a good player and a good steward to the world, and wanting to completely run its own show. The politicization of what’s going on over there, we all saw what happened in the real estate market recently, we saw what happened with tech ed over the last few months, we’ve seen what’s happened with innovation, and entrepreneurship. It is not entirely clear if China wants to give the more capitalistic and innovation ecosystem a full try, but it has certainly shown that it wants to be seen as a world leader over the last few decades. It’s accomplished that, in almost any area that it wants to compete. Dave, I would say, if this is one of Xi Jinping primary areas of focus, wanting to be self-sufficient in semiconductors, it would be a very irresponsible to rule it out as a possibility.

Many thanks to Daniel Newman for his collaboration and insights today. Follow Daniel @danielnewmanUV on Twitter and check out the Futurum Web site.

Remember we publish each week on Wikibon and SiliconANGLE. These episodes are all available as podcasts wherever you listen.

Email david.vellante@siliconangle.com, DM @dvellante on Twitter and comment on our LinkedIn posts.

Also, check out this ETR Tutorial we created, which explains the spending methodology in more detail. Note: ETR is a separate company from Wikibon and SiliconANGLE. If you would like to cite or republish any of the company’s data, or inquire about its services, please contact ETR at legal@etr.ai.

Here’s the full video analysis:

All statements made regarding companies or securities are strictly beliefs, points of view and opinions held by SiliconANGLE media, Enterprise Technology Research, other guests on theCUBE and guest writers. Such statements are not recommendations by these individuals to buy, sell or hold any security. The content presented does not constitute investment advice and should not be used as the basis for any investment decision. You and only you are responsible for your investment decisions.

Support our mission to keep content open and free by engaging with theCUBE community. Join theCUBE’s Alumni Trust Network, where technology leaders connect, share intelligence and create opportunities.

Founded by tech visionaries John Furrier and Dave Vellante, SiliconANGLE Media has built a dynamic ecosystem of industry-leading digital media brands that reach 15+ million elite tech professionals. Our new proprietary theCUBE AI Video Cloud is breaking ground in audience interaction, leveraging theCUBEai.com neural network to help technology companies make data-driven decisions and stay at the forefront of industry conversations.