SECURITY

SECURITY

SECURITY

SECURITY

SECURITY

Organizations continue to spend more on security, with 87% of firms expecting to increase spend on cybersecurity in the next 12 months. But are we safer?

It’s estimated that firms on average have between 60 and 75 security tools installed. Although leading vendors logically market the benefits of addressing tools sprawl and complexity through consolidation, the data suggests that more than half the firms are increasing the number of security vendors installed, with a very small percentage able to effect vendor consolidation.

Adding to the challenge is an environment where security operations pros have too many priorities to manage, including identity, vulnerability management, patching, endpoint, security and information event management, antivirus, zero trust, cloud security and more. Finally, firms are investing in artificial intelligence to relieve the crushing labor burden security analysts are facing but are being forced to balance innovation with the daily battle.

In this Breaking Analysis, we preview RSA Conference 2024 with our colleague Erik Bradley of Enterprise Technology Research. We’ll provide a detailed analysis of a recent survey conducted by ETR, perfectly timed ahead of RSA.

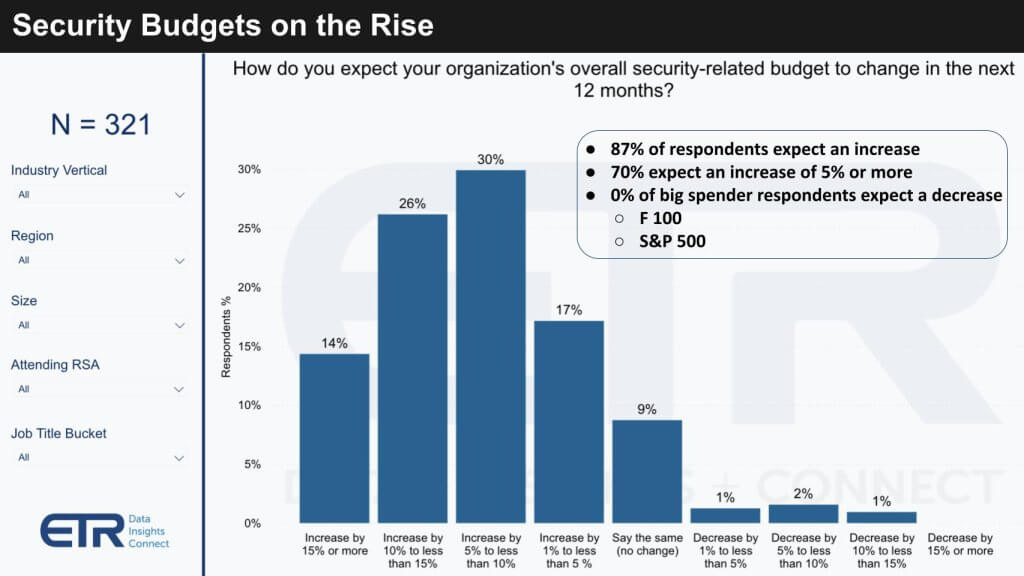

The chart below shows data from the most recent ETR survey we referenced at the top. As you can see, the N is 321 respondents and the vast majority, 87%, are increasing spend on security, with 70% expecting an increase of 5% or more, which is higher than the overall information technology spending average of 3.4%. The other notable callout is that 0% of the Fortune 100 and S&P 500 respondents in the survey expect a decrease in budget.

This data represents a standout revelation from the survey in that 70% of customers see their security budgets growing by 5% or more, a strikingly high rate of security spending compared with IT spending at large. The data further shows that more than half of the surveyed firms are increasing their security investment by 5% to 14%. Notably, an astonishing 14% of respondents are engaging in what we classify as “hypergrowth” in spending, exceeding a 15% increase. This hypergrowth threshold is not strictly defined and could include some very large outliers, which leads us to believe that the actual figures may be significantly higher than reported.

Our analysis further identifies a notable trend within organizational size dynamics. Midsized companies, which ETR categorizes as those with 200 to 1,200 employees, have 92% of respondents reporting spending increases, and an exceptional 23% of them are anticipating hypergrowth. Conversely, the Global 2000 companies exhibit the least propensity toward hypergrowth, which is a rational trend given their already substantial budget baselines. This disparity underscores that the rate of security spend escalation is not only surpassing general IT expenditure but also varies by company size.

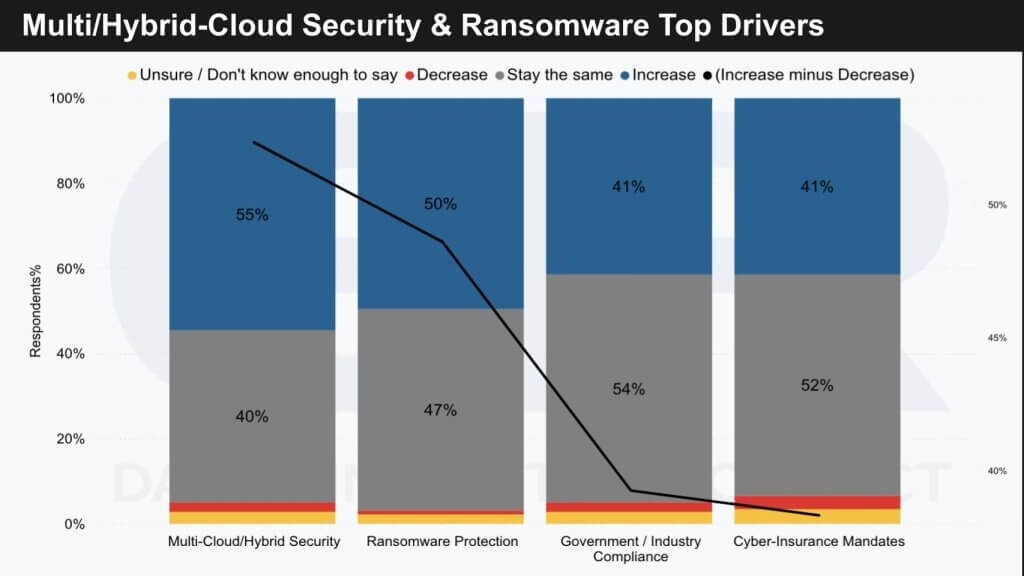

The data above shows the areas driving the highest increase in spend. Note the data is presented on a double Y axis, so that black line, which is the percentage of respondents increasing spend minus the percentage decreasing spend, is actually quite high on the righthand vertical axis.

Respondents in the ETR survey indicate that multicloud and ransomware are pivotal factors influencing the increase in security spending. We’ve noted in previous Breaking Analysis and supercloud research the complexity brought on by the need to secure multicloud and hybrid cloud environments, which inherently expand the threat surface. This complexity appears to be a substantial driver thanks to the increase in attack vectors it presents.

We note the following key catalysts for heightened security expenditure are:

We further emphasize:

Interestingly, cyber insurance is seen as less of a driver for increased security spending, particularly within the Global 2000:

This perceived maturation perhaps is the result of a rationalization within the industry after years of tumult, reflecting a better alignment between cyber insurance demands and the realities of security tool efficacy.

This next set of data is eye-opening. The survey asked respondents whether over the next 12 months they expect the number of security vendors to increase, decrease or stay flat. The prevailing narrative in the industry would suggest that most customers are consolidating the number of vendors in their security stack. They’re not.

Our research reveals a significant deviation from the vendor narrative regarding security tool consolidation within organizations. Contrary to the successful examples by leading security firms such as CrowdStrike Holdings Inc., Palo Alto Networks Inc. and Zscaler Inc., the data does not primarily reflect a trend toward vendor consolidation. Key findings include:

These insights lead us to anticipate:

This data represents a contrarian view to the industry’s consolidation rhetoric. Despite public earnings calls touting strategic shifts toward platform integration, the ground reality reflects a persistent inclination toward “best of breed” solutions and a readiness to onboard additional vendors if deemed necessary.

The gap between strategic aspirations of security companies and the operational practices of end-users suggests that, although consolidation is a stated goal, the industry may not yet be ripe for such a transition. The data firmly points to a continued increase in the number of security vendors, emphasizing the need for vigilance as security architectures evolve.

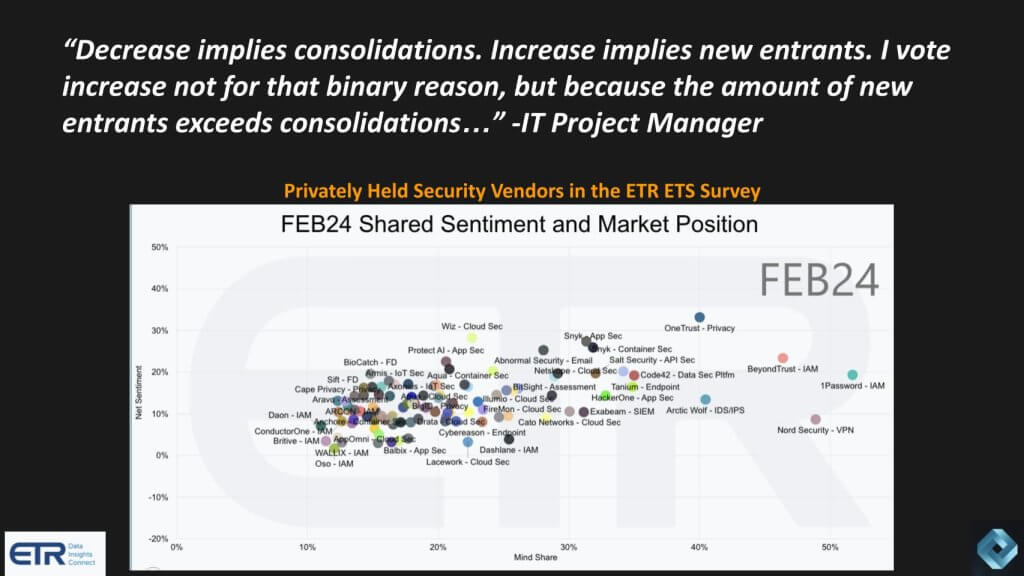

We posted an informal X poll to assess sentiment in the community. While half the respondents expected the number of vendors to decrease, a healthy 30% indicated they thought the number would grow. We suspect those were likely practitioners on the ground. Below we show the comment made by one IT person who said: “Decrease implies consolidations. Increase implies new entrants. I vote increase not for that binary reason, but because the amount of new entrants exceeds consolidations.”

And for effect, we’ve superimposed an impossible-to-read chart – that’s the point – from ETR’s Emerging Technology Survey of privately held companies. This is the security sector and you can see how crowded it is with names that are well-known, such as OneTrust, BeyondTrust, 1Password, Nord, Wiz, Snyk, Cato and multiple dozens of others.

The prevailing sentiment that vendor consolidation is the dominant trend in security is not substantiated by this data. Rather, the opposite appears to be true and the data indicates a tendency toward the adoption of new entrants in the market rather than consolidation. This is attributed to the sheer volume of novel solutions surpassing the rate of vendor consolidation.

We note the following additional points:

The sector’s dynamism and firms’ vulnerabilities support the addition of new companies. This underscores the industry’s rapid evolution and the critical need for businesses to remain vigilant and adaptable in their security postures.

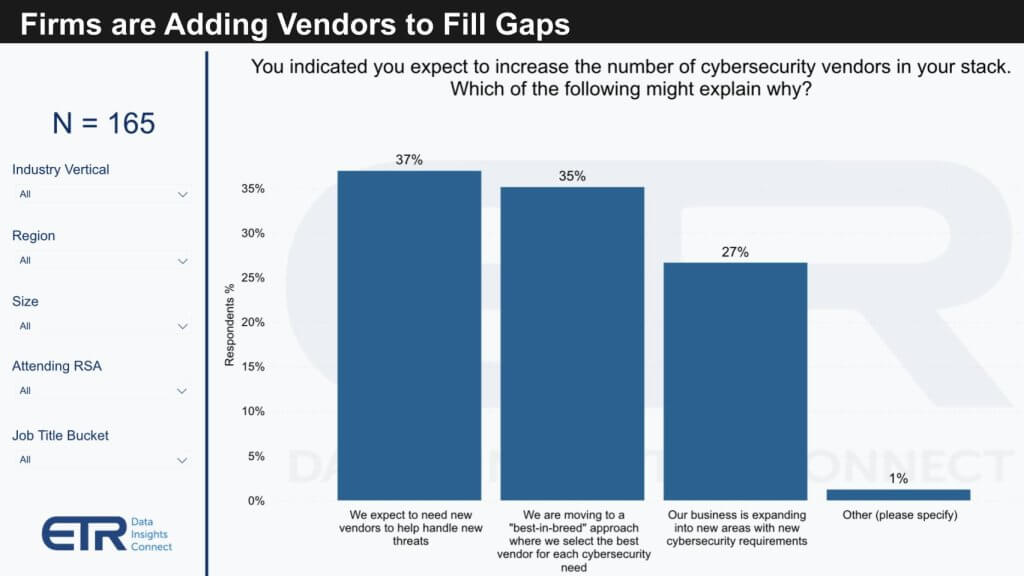

The data below drills into those respondents saying they were increasing the number of vendors in their cyber stack. The survey asks them why they’re adding vendors.

The implications are:

There is a notable consensus that though there’s a universal preference for reducing the number of vendors, this doesn’t overshadow the demand for robust security measures. About 36% of the respondents highlighted the emergence of new threats and the pursuit of best-of-breed solutions as primary reasons for increased vendor counts. Additionally, 27% cited expanding business initiatives as a contributing factor.

In stark contrast to this trend, a small fraction of respondents — only 29 out of over 300 — indicated a decrease in their security vendor stack, mainly motivated by budget constraints and a strategic push toward simplification.

We believe the discourse around vendor value and consolidation takes on greater significance in light of the term “spending fatigue” used in recent earnings calls. This has sparked debate among industry leaders, with companies such as CrowdStrike and Zscaler reporting contrasting trends.

The question remains whether a single vendor can truly offer a best-of-breed experience across a broad portfolio, a question highlighted in discussions with other analysts on theCUBE. The emerging view seems to suggest that though “good enough” might work in certain areas, in the domain of security, the stakes are too high to settle for anything less than best-of-breed, underscoring the enduring importance of a layered defense strategy.

That said, the growth and increasing ubiquity of Microsoft’s security tooling, despite the scathing report by the government’s Cyber Safety Review Board about Microsoft’s poor security practices, indicates that good enough may be good enough for many customers. Nonetheless, we believe best practice calls for layering further protections on top of Microsoft tooling.

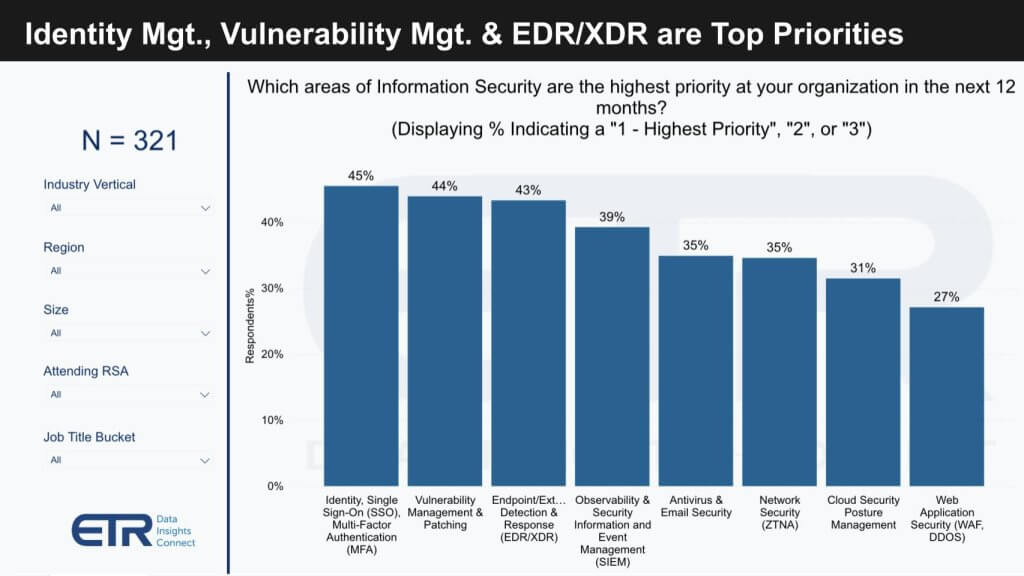

In the words of former Snowflake Chief Executive Frank Slootman, “If you have 10 priorities, you have none.” This chart below underscores the problem in cyber. You can’t narrow things down to one priority. Identity, single sign-on, multifactor authentication, patching, EDR, XDR, SIEM, observability, antivirus, zero trust, cloud, web application firewall – customers face a never ending set of priorities. And if you ignore any of them, you do so at your own peril.

Our research shows that in the domain of cybersecurity, the disparity in priorities between C-suite executives and operational practitioners is becoming increasingly evident.

ETR has launched a new product, Market Arrays, which provides a deep dive into the various aspects of identity and endpoint platforms (with more sectors coming) revealing that:

This data underscores the varying focus areas within an organization, reflecting differing priorities based on role and responsibility. It’s clear that though all facets of security are deemed critical, there’s a pronounced contrast between the strategic oversight of executives and the immediate, hands-on challenges faced by analysts. Such disparities suggest a need for greater alignment and understanding across the different organizational tiers to effectively address the comprehensive security landscape.

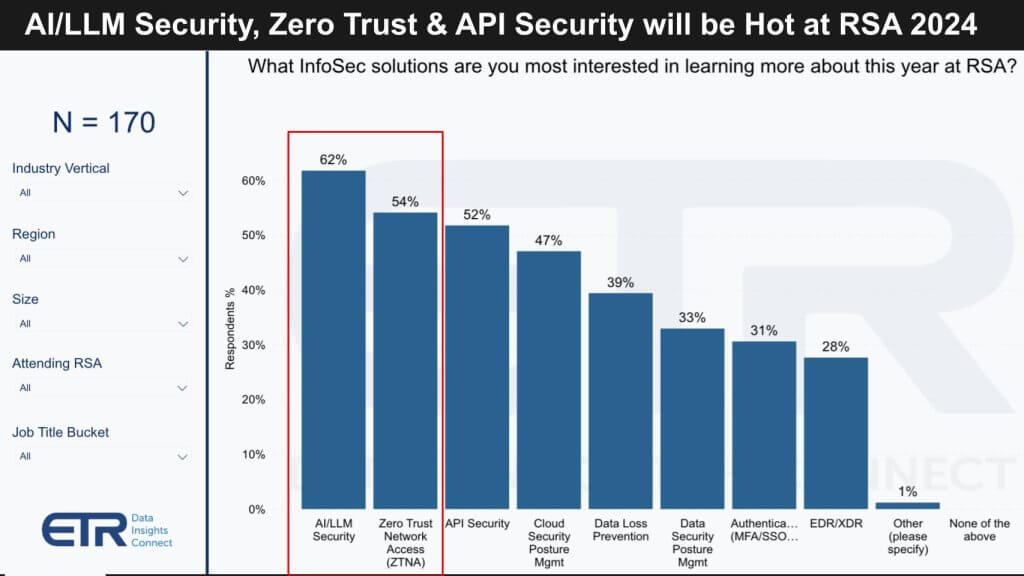

In the latest survey of 321 security professionals, 170 (53%) have indicated their intention to attend RSA. Their interests span a range of topics, reflecting the current security landscape’s complexity and the ever-growing demands on security operations professionals. The key areas of interest for RSA attendees are:

It is noteworthy that despite the extensive list of topics security professionals need to keep abreast of, DLP and data security management are surprisingly ranked lower in priority. Moreover, approximately 30% of respondents have no immediate plans to assess their data security management strategies. This could suggest a concerning complacency or a gap in recognizing the critical importance of robust data security practices amidst the fast-evolving digital threat landscape. Such findings tell us there’s a necessity for continual education and strategy reassessment to ensure comprehensive security across all organizational data touch points.

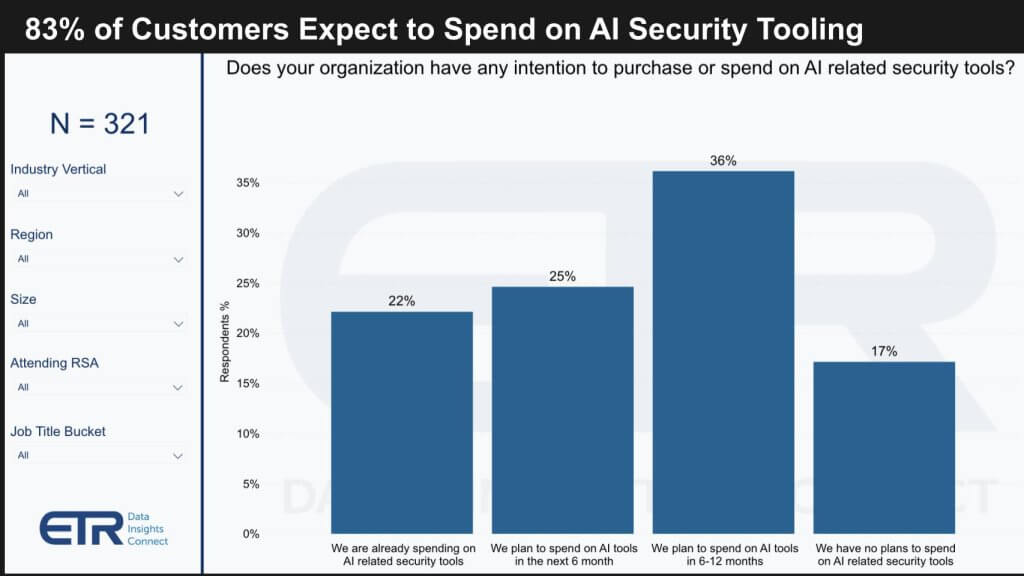

Our analysis of the latest survey data provides insights into the current and future spending trends on AI security tools. The findings suggest that AI’s role in security is expanding rapidly, with:

Although a small segment indicates no planned expenditure on AI-specific tools, the broader trend highlights a substantial commitment to AI in the security domain. The intent behind the question in the ETR survey was specifically geared toward net new investments in AI tools rather than incidental spending on embedded AI features within existing products.

Additional ETR data not displayed above reveals that:

These figures underscore a relatively low baseline of existing AI integration, suggesting considerable growth potential for AI application in security tools. With the majority of respondents planning to invest, the landscape of AI-enabled security tools is poised for significant growth in our view, reflecting both a demand for advanced security measures and the growing importance of AI in addressing complex security challenges, particularly the lack of qualified human labor. Moreover, as attackers increasingly use AI to penetrate organizations, AI will be of increasing importance to stop and detect breaches and take remedial action.

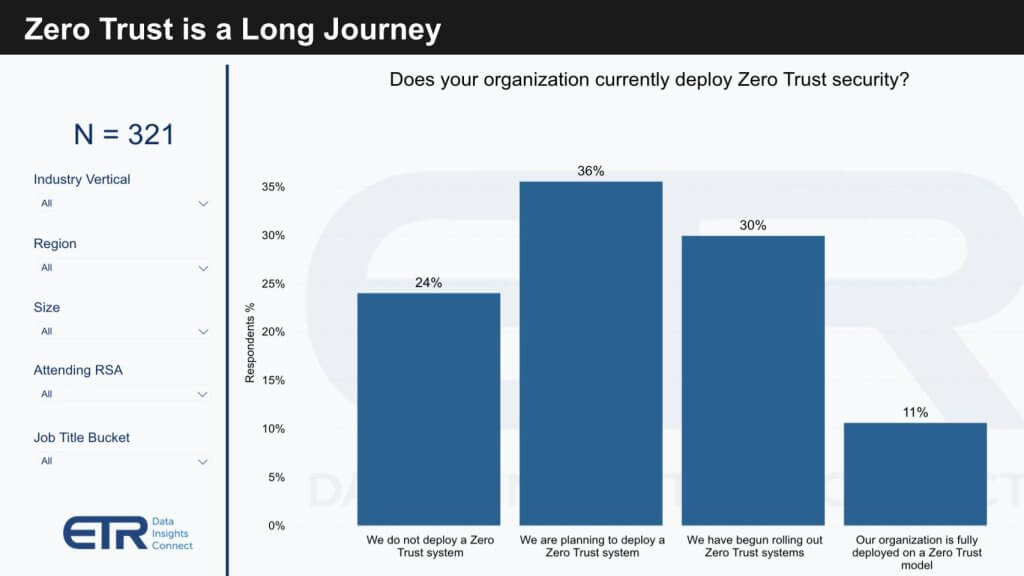

The industry narrative around zero-trust architectures reveals a gap between market hype and the on-the-ground reality seen by security practitioners. Although zero trust is receiving justified attention, its implementation is complex and multifaceted. Among the surveyed CISOs, there is a clear drive to adopt zero-trust methodologies, but several hurdles remain:

Despite these challenges, our findings suggest an encouraging trend toward adoption:

Interestingly, there is a notable discrepancy in perceptions between job roles regarding the deployment of zero trust:

This difference in perception highlights a communication gap within organizations regarding the status of zero-trust implementation. Overall, the landscape for zero trust is still evolving, with the majority of entities recognizing its value and actively moving toward it, signifying a significant future growth area in security architecture.

TheCUBE once again will be broadcasting live from Moscone West at RSA. Our program spans four days of coverage with leading practitioners, analysts, industry CEOs and thought leaders. All the action can be found here on theCUBE’s live broadcast site and on SiliconANGLE.

At RSA, we will also engage directly with the cybersecurity community, attending various events, such as a cocktail party SiliconANGLE is hosting alongside the New York Stock Exchange, OpenPolicy and Intel Capital, and collaborating with companies such as Elastic. We eagerly anticipate these interactions as an opportunity to further our understanding and assess the pulse of the industry.

As we look ahead to RSA 2024, our focus will be on a number of critical developments and dynamics within the cybersecurity domain. Key points of interest include:

Our presence at Moscone West in Media Row offers a prime location for networking and sharing insights. We invite attendees to join us for these discussions, and we look forward to the productive exchanges that RSA always facilitates, connecting technology providers, end-users and investors alike. As always, the convergence of perspectives at RSA provides a comprehensive snapshot of the current state and future direction of cybersecurity.

See you there!

Support our mission to keep content open and free by engaging with theCUBE community. Join theCUBE’s Alumni Trust Network, where technology leaders connect, share intelligence and create opportunities.

Founded by tech visionaries John Furrier and Dave Vellante, SiliconANGLE Media has built a dynamic ecosystem of industry-leading digital media brands that reach 15+ million elite tech professionals. Our new proprietary theCUBE AI Video Cloud is breaking ground in audience interaction, leveraging theCUBEai.com neural network to help technology companies make data-driven decisions and stay at the forefront of industry conversations.