EMERGING TECH

EMERGING TECH

EMERGING TECH

EMERGING TECH

EMERGING TECH

The negative sentiment in tech stocks, caused by rising interest rates, less attractive discounted cash flow models and more tepid forward guidance, is easily measured by public market valuations. And while there’s lots of talk about the impact on private companies, their cash runways and 409A valuations, measuring the performance of nonpublic companies isn’t as easy. Initial public offerings have dried up and public statements by private companies accentuate the good and hide the bad. Real data, unless you’re an insider, is hard to find.

In this Breaking Analysis, we unlock some of the secrets that nonpublic, emerging tech companies may or may not be sharing. We do this by introducing you to a capability from Enterprise Technology Research that we’ve not previously exposed in Breaking Analysis. It’s called the ETR Emerging Technology Survey and it’s packed with sentiment and performance data based on surveys of more than 1,000 chief information officers and information technology buyers covering more than 400 private companies. The survey will highlight metrics on the evaluation, adoption and churn rates for private companies and the mindshare they’re able to capture.

We’ve invited back our colleague Erik Bradley of ETR to help explain the survey and the data we’re going to cover in this post.

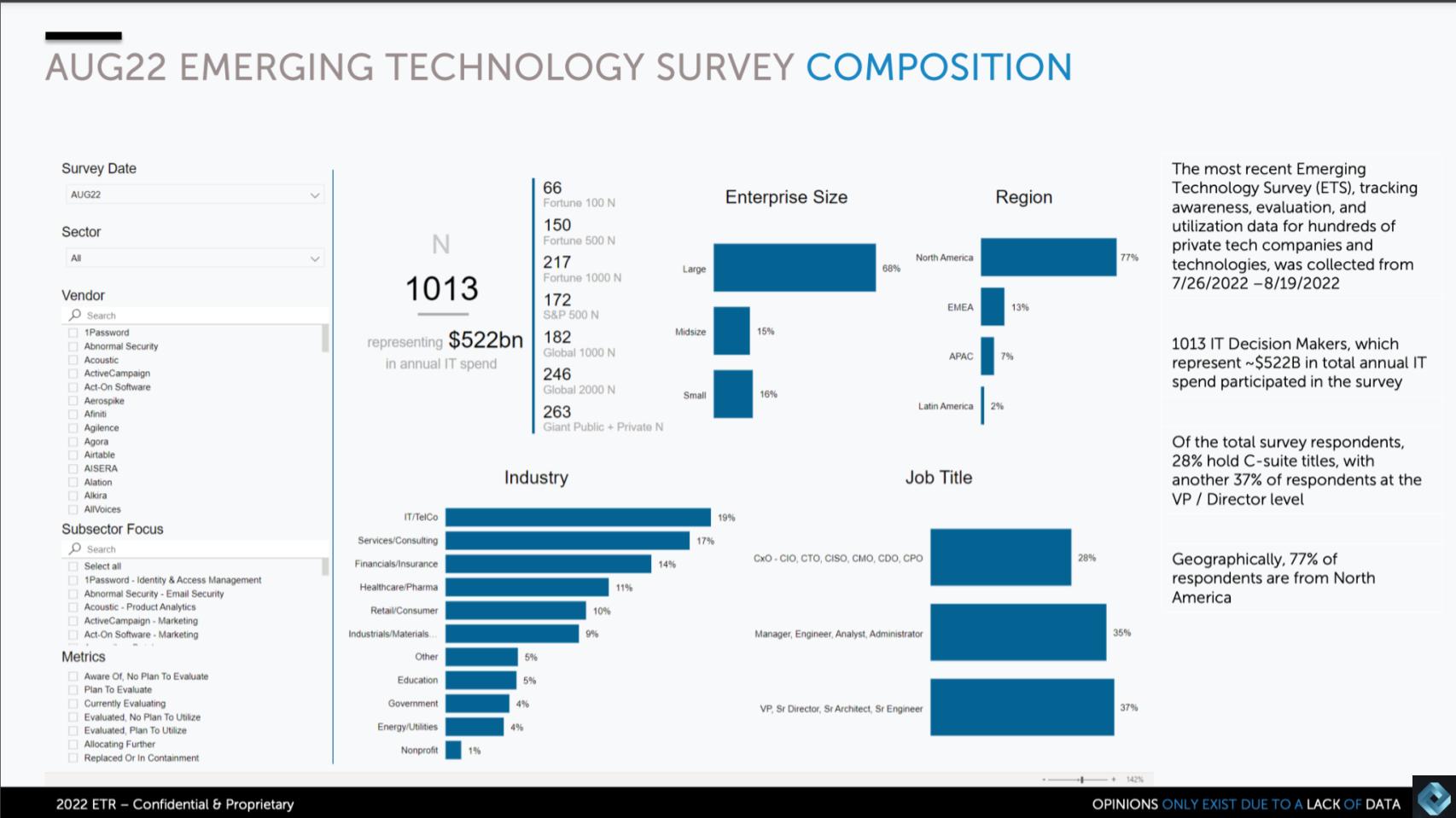

The above slide shows the the breakdown of survey respondents. Erik Bradley shared following data, which summarizes the survey breakdown:

[Listen to Erik Bradley explain the background of the ETS study & its methodology].

This Breaking Analysis is structured as follows:

One other note: The ETS data very often will include open-source offerings in the mix of companies, even though they’re not companies. An example is you’ll see adoption data for tools like TensorFlow and Kubernetes. This is done is for context, because virtually everyone is using open-source tooling and thus it provides a comparative data point. As well, many companies are building businesses around open-source platforms and this serves as a momentum indicator for the space in which they play.

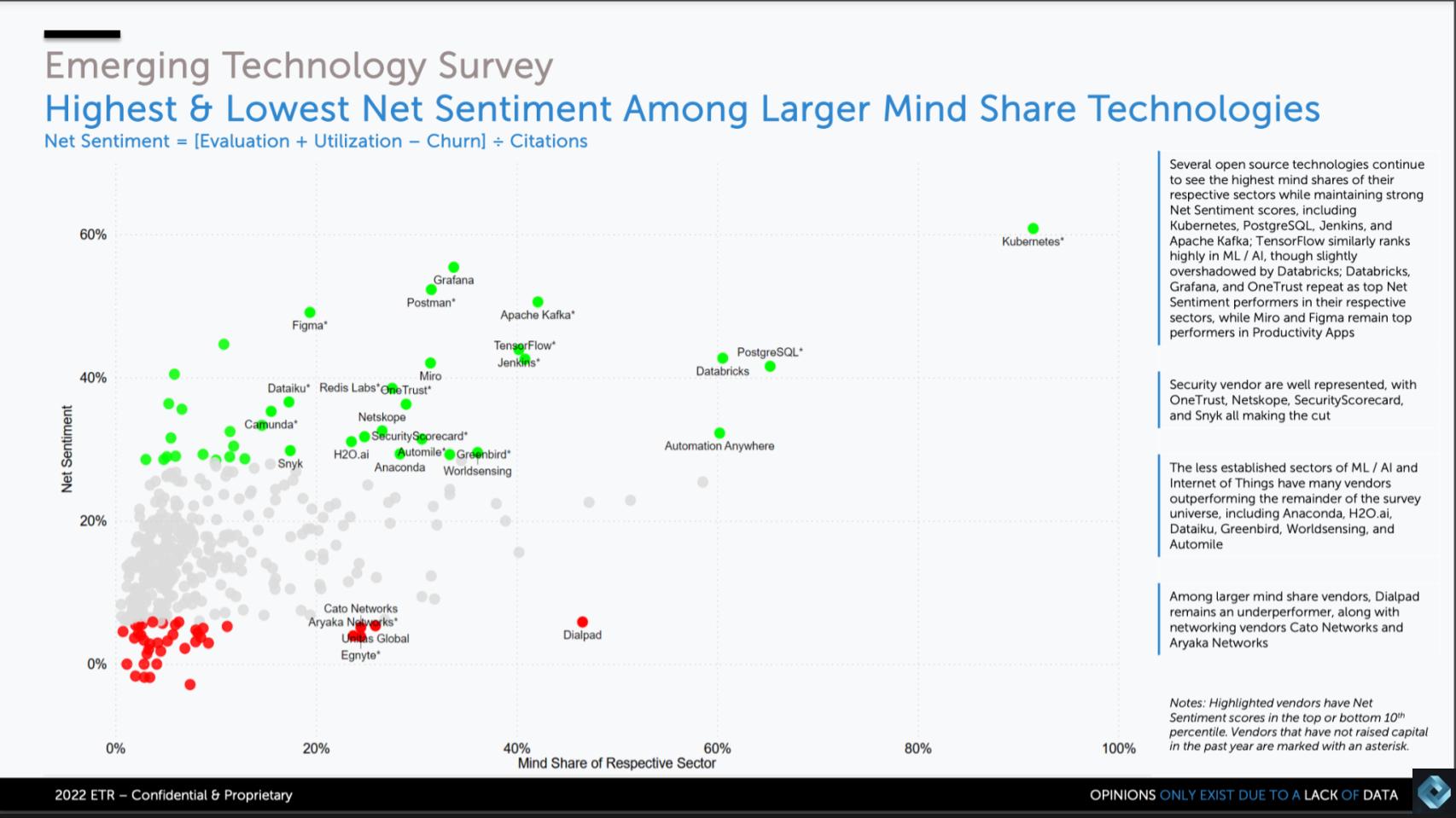

The graphic above looks at the highest (green dots) and lowest (red dots) sentiment among those private firms with the largest mindshare. The data is presented two dimensions — Net Sentiment on the vertical axis and Mindshare on the horizontal axis. Net Sentiment is a measure derived from adding the percentage of customers evaluating plus adopting, then subtracting the percentage of customers not planning to evaluate and churning the platform. It basically is an aggregation of all the positives minus the negatives. Mindshare is a measure of awareness within the data set.

The gray dots in the middle represent the mid-pack. So green is good, red is bad relative to the mean.

Note the open source tools – Kubernetes, Postgres, Kafka, TensorFlow, Jenkins and Grafana.

Erik Bradley called out a few takeaways as follows:

So what we’re looking at here, if I can just get away from the open-source names, we see other names like Databricks and OneTrust. They’re repeating as top Net Sentiment performers here. And then also the design vendors like Miro and Figma. This is their third survey in a row where they’re just dominating that sentiment overall. And Adobe should probably take note of that because these firms are really coming after Adobe. But Databricks, we all know probably would’ve been a public company by now if the market hadn’t turned, but you can see just how dominant they are in a survey of nothing but private companies. And we’ll see that again when we talk about the database later.

Some other names that stand out in the data:

These are several names that we think ultimately will hit the public markets or be acquired.

Listen to Erik Bradley’s commentary on the private companies with the largest mindshare.

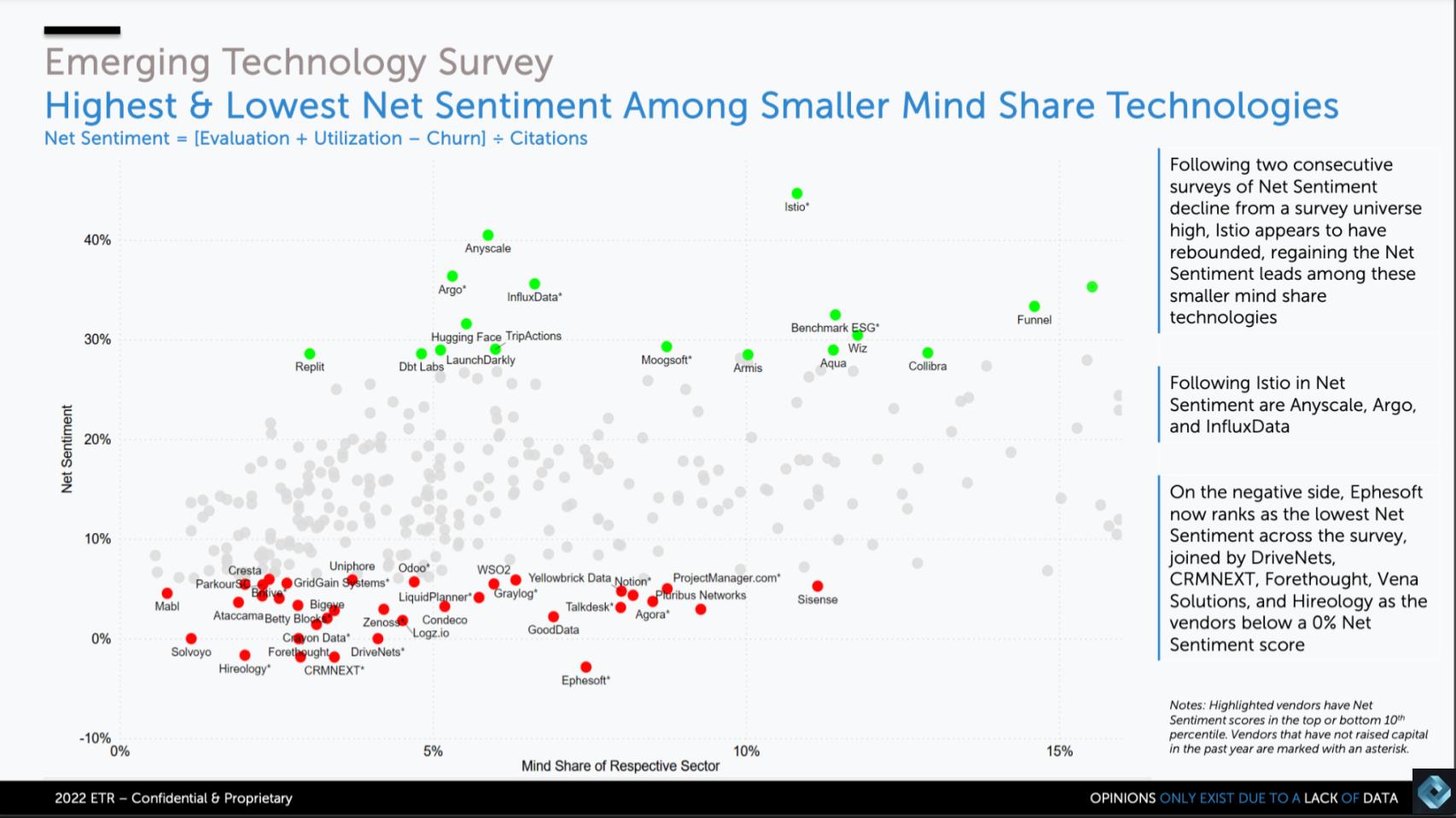

Above we show the same view for private companies with lower mindshare.

Some of the names that jump right out:

Erik Bradley added the following comments:

It’s interesting to talk about open source. Kubernetes was all the way on the top right. Everyone uses containers. Here we see Istio up there. Not everyone is using service mesh as much. And that’s why Istio is in the smaller breakout. But still when you talk about Net Sentiment, it’s about the leader, it’s the highest one there is. So really interesting to point out that Istio leads. Then we see other names like Collibra in the data side really performing well. And again, as always security, very well represented here. We have Aqua, Wiz, Armis, which is a standout in this survey this time around. They do IoT security. I hadn’t even heard of them until I started digging into the data here.

And I couldn’t believe how well they were doing. And then of course you have Anyscale, which is doing second best in this group and the best name in the survey Hugging Face, which is a machine learning AI tool. Also doing really well on a Net Sentiment basis, but they’re not as far along on that axis of mindshare just yet. So these are again, emerging companies that might not be as well-represented in the enterprise as they will be in a couple of years.

Listen to Erik Bradley’s commentary on those private companies with smaller mindshare.

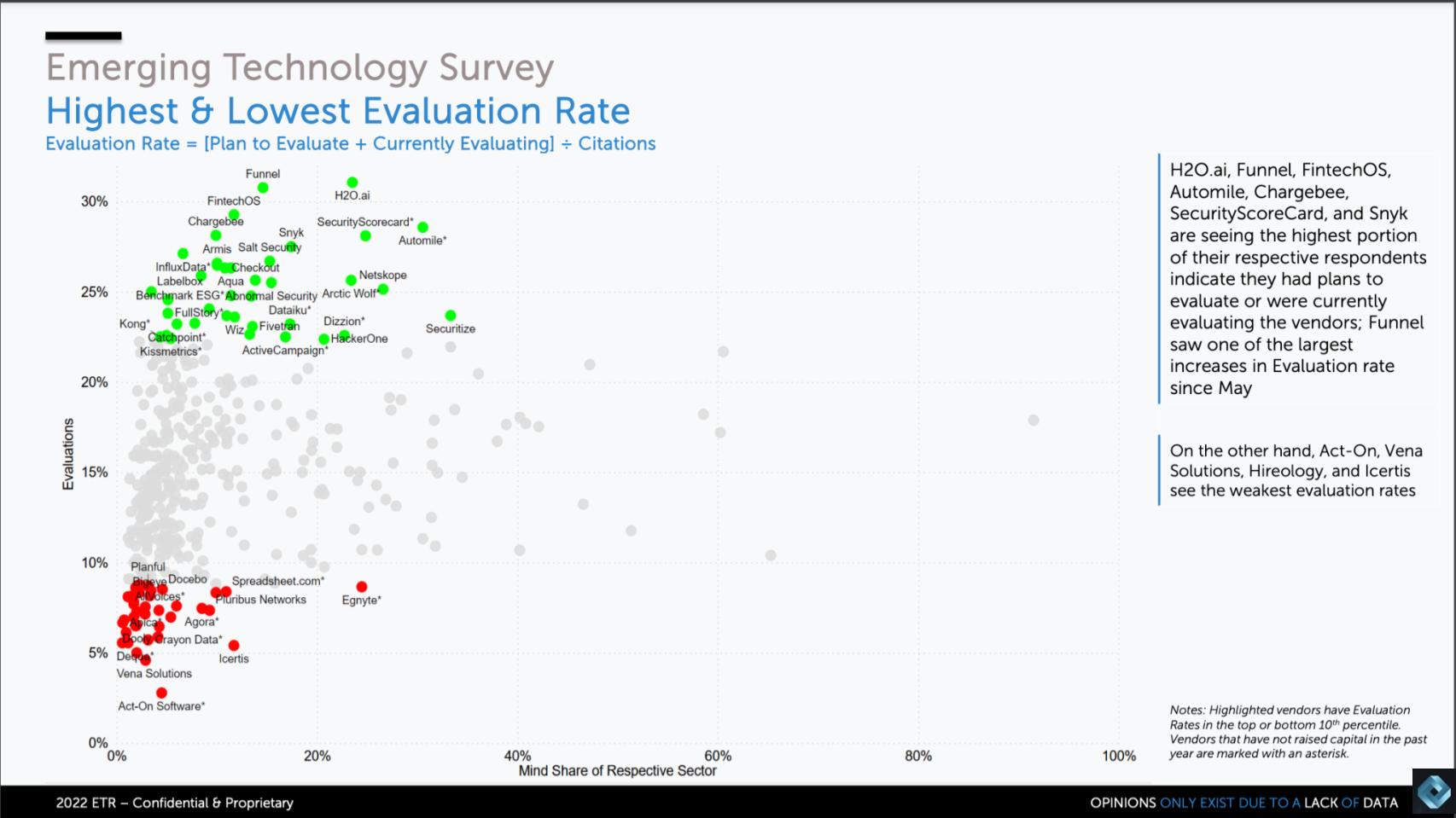

We now move into the next segment here where we look at evaluation rates, adoption and churn. First, new evaluations as shown above. Evaluation means respondents sited that they either plan to evaluate a firm or they’re currently evaluating. In later surveys we can measure conversion from evaluations and the full cycle from awareness–>evaluation–>adoption–>churn.

Erik Bradley further commented:

What we’re seeing here are some very high evaluation rates in the green. H2O, we mentioned. SecurityScorecard jumped up again. Chargebee, Snyk, Salt Security, Armis. A lot of security names are up here, Aqua, Netskope, which has been around forever. I still can’t believe it’s in an Emerging Technology Survey, but so many of these names fall in data and security again, which is why we decided to pick those out.

And on the lower side, Vena, Acton, those unfortunately took the dubious award of the lowest evaluations in our survey, but I prefer to focus on the positive. So SecurityScorecard, again, real standout in this one, they’re in a security assessment space, basically. They’ll come in and assess for you how your security hygiene is. And it’s an area of a real interest right now amongst our IT community.

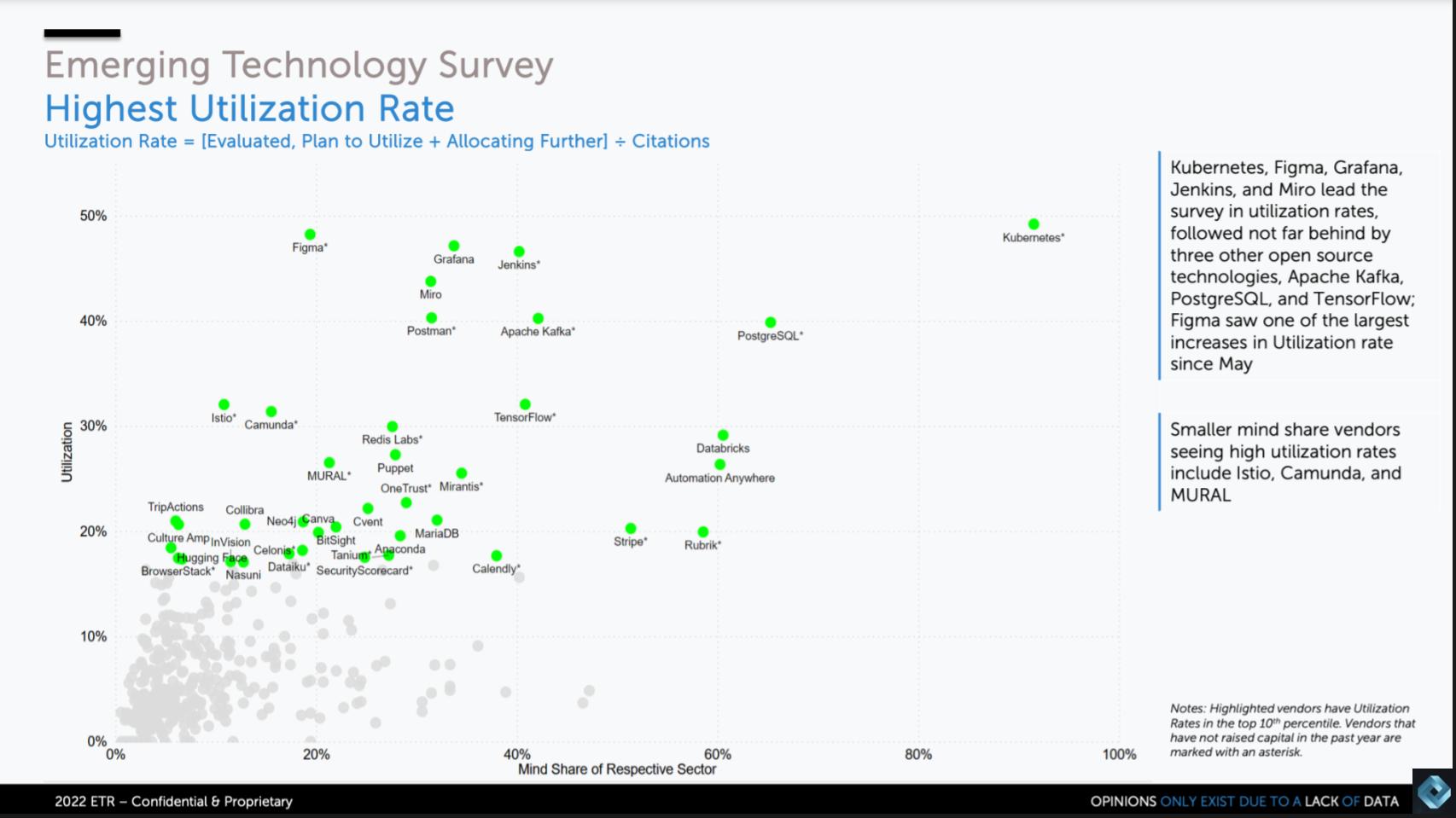

We’re going through the buying journey. We looked earlier at awareness, then went to evaluation. In this section of Breaking Analysis, it’s about utilization or adoption, shown in the graphic above. In this case we refer to a respondent affirming that they evaluated a product and they’re either using it or they plan to adopt and allocate further resources to the solution.

Erik Bradley commented as follows:

Not surprising here, a lot of open source, the reason why: It’s free. So it’s really easy to grow your utilization on something that’s free. But as you and I both know, as Red Hat proved, there’s a lot of money to be made once the open source is adopted, right? You need the governance, you need the security, you need the support wrapped around it. So here we’re seeing Kubernetes, Postgres, Apache Kafka, Jenkins, Grafana. These are all open-source-based names. But if we’re looking at names that are non-open-source, we’re going to see Databricks, Automation Anywhere, Rubrik all have the highest mindshare.

So these are the names, not surprisingly, all names that probably should have been public by now. Everyone’s expecting an IPO imminently [as soon as the markets allow]. These are the names that have the highest mindshare. If we talk about the highest utilization rates, again, Miro and Figma pop up, and I know they’re not household names, but they are just dominant in this survey. These are applications that are meant for design software and, again, they’re going after an Autodesk CAD or Adobe type of thing. It is just dominant how high the utilization rates are here, which again is something Adobe should be paying attention to. And then you’ll see a little bit lower, but also interesting, we see Collibra again, we see Hugging Face again. And these are names that are obviously in the data governance, ML, AI side. So we’re seeing a ton of data, a ton of security and Rubrik was interesting in this one, too, high utilization and high mindshare. We know how pervasive they are in the enterprise already.

Listen to Erik Bradley’s comments on the adoption rates for these private companies.

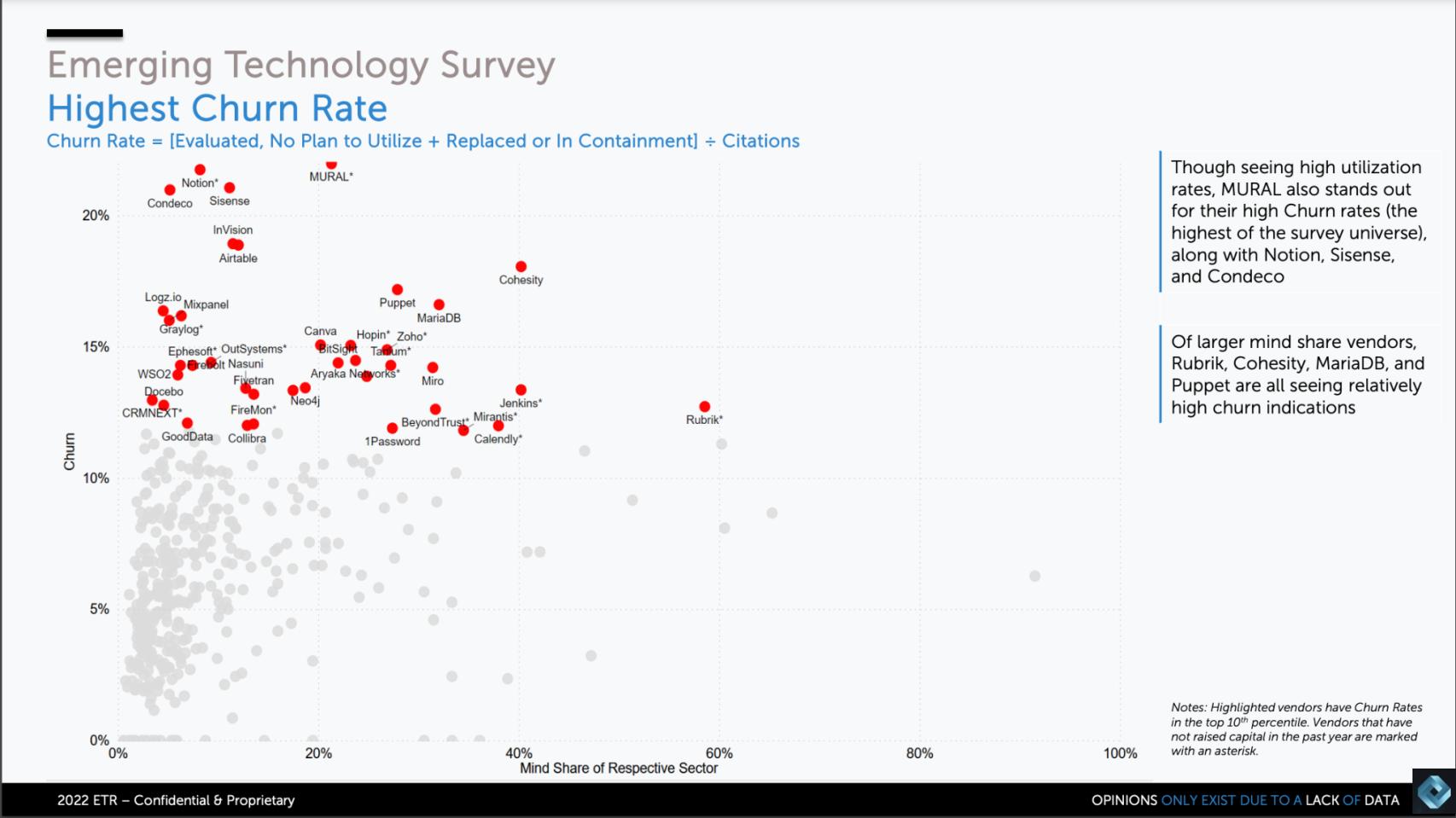

The following chart is the one in which you don’t want to have the highest score. Churn measures defections from a platform and is often caused by poor product market fit, sales to the wrong type of customer – i.e. a miss on the ideal customer profile, poor customer service, bad product quality or go-to-market challenges.

Some key points on this churn data:

Erik Bradley commented as follows:

The reason I call that out Cohesity is it has an extremely high churn rate here – about 17%. And unlike Rubrik, they were not on high on the utilization [metric]. So Rubrik is seeing both [high utilization and high churn], Cohesity is not seeing the same high utilization, but it’s seeing a high churn. So that’s when you can look at this data and say, “Hmm.”

[Puppet is similar to Rubrik]. You noticed that it was on the previous slide. It’s also on this one. So basically what it means is a lot of people are giving Puppet a shot, but it’s starting to churn, which means it’s not as sticky as we would like. One that was surprising on here for me was Tanium. It’s kind of jumbled in there. It’s hard to see in the middle, but Tanium, I was very surprised to see as high of a churn because what I do hear from our end-user community is that people that use it, like it. It really kind of spreads into not only vulnerability management, but also that endpoint detection and response side. So I was surprised by that one, mostly to see Tanium in here. Mural, again, was another one of those application design softwares that’s seeing a very high churn.

The point here is if a company scores highly in utilization that’s a positive but, like MariaDB Inc., Rubrik and Puppet Inc., for example, they’re also seeing higher churn. They’re both green in the previous one and red here, that’s not interpreted as purely negative.

Listen to Erik Bradley’s comments on the churn rates for private companies.

Let’s take a brief aside here and drill into the Cohesity and Rubrik dynamic. These are two companies that combined have raised more than $1.3 billion to disrupt the traditional backup market, initially positioning as data management players – doing more than backup and recovery – and now bleeding into cybersecurity. Rubrik in particular has heavily pivoted, positioning itself as a cybersecurity play, which we see as a somewhat of a stretch.

We pulled the data above from ETR’s quarterly TSIS data set. It is an XY graphic with Net Score or spending momentum on the vertical axis and Overlap or presence in the data set on the horizontal plane. The red dotted line at 40% indicates highly elevated spending momentum. The inserted chart contains the raw data that informs the position of the plot on each axis.

You can see where Cohesity and Rubrik were positioned on the vertical axis pre-pandemic. At that time it confirmed our strong belief that these companies each had significant momentum and were successful in bringing a modern experience to the backup and data protection market, far outpacing the other data protection players in the survey. Spending momentum on these platforms moderated during the pandemic and is well below their pre-pandemic highs. Companies that have raised as much as these two firms should have hit the public markets during the tech bubble of 2020 and 2021 but they were unable to do so, which is an indicator that they simply didn’t have the metrics and confidence in their respective businesses to make promises to Wall Street.

Rubrik is repositioning the company as a cybersecurity play, Cohesity as well as all the data protection players, market protection against cyberattacks generally and ransomware specifically. Cohesity recently named Sanjay Poonen as chief executive. He is an expert operator and go-to-market pro with deep experience at SAP SE and more recently VMware Inc. We suspect Cohesity made this move to allow its founder, Mohit Aron, who is a technical guru, to focus his time on product while Poonen addresses Cohesity’s operational and go-to-market challenges and opportunities.

Veeam Software Inc. stands out in this market as the company with steady progress — not necessarily remarkable growth in any given year but extremely consistent over time. The private equity firm Insight Partners acquired Veeam just prior to the pandemic for approximately $5 billion and is likely positioning the company for an IPO to join Commvault Systems Inc. as a public firm. Rubrik and Cohesity will likely follow suit once the IPO market returns.

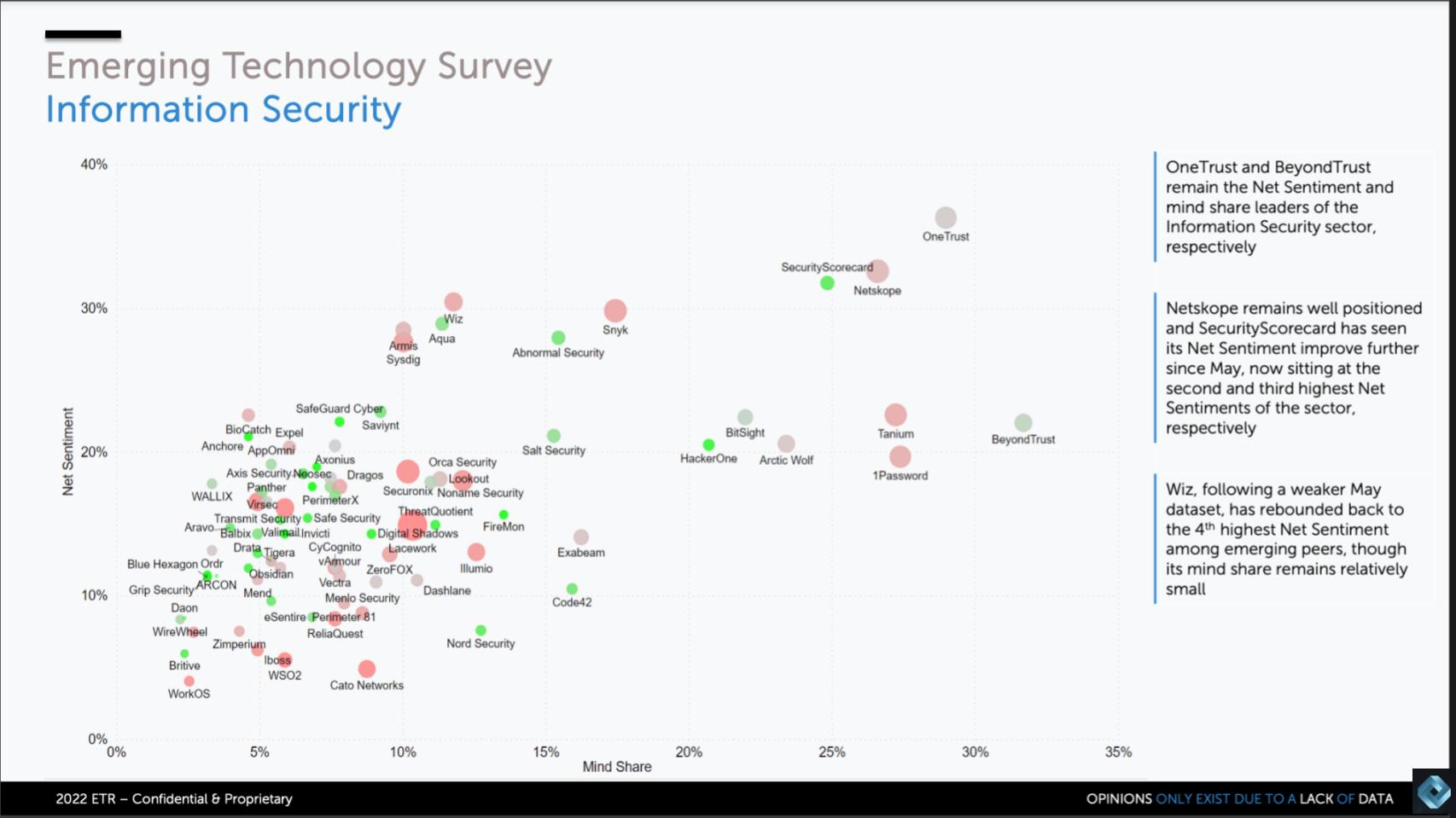

Now we’re going to drill down into two sectors, security and data. Data comprises three areas database and data warehousing, machine learning and AI and big data analytics. First let’s take a look at the security sector.

This next data dive is super-interesting because not only is it a sector drill-down, but it also gives an indicator of how much money the firm has raised. The axes are the same, Net Sentiment and Mindshare, but what ETR did is take publicly available information on how much capital a company has raised and that’s the size of the bubble.

The color of the circle – green, red or neutral – is telling us, relative to the amount of money they’ve raised, how are they doing in the data?

Erik Bradley explains further:

When you see a Netskope, which has been around forever, raised a lot of money, that’s why you’re going to see them more leaning towards red, because it’s just been around forever. Versus a name like SecurityScorecard, which has only raised a little bit of money and it’s actually performing just as well, if not better than a name like Netskope. OneTrust doing absolutely incredible right now. BeyondTrust. We’ve seen the issues with Okta, right? So those are two names that play in that space that obviously are probably getting some looks about what’s going on right now.

Wiz, we’ve all heard about right? Raised a ton of money. It’s doing well on Net Sentiment, but the mindshare isn’t as well as you’d want, which is why you’re going to see a little bit of that red versus a name like Aqua, which is doing container and application security. And hasn’t raised as much money, but is really neck-and-neck with a name like Wiz. So that is why on a relative basis, you’ll see that more green. As we all know, information security is never going away. But as we’ll get to later in the program, I’m not sure in this current market environment, if people are as willing to do POCs and switch away from their security provider. There’s a little bit of tepidness out there, a little trepidation. So right now we’re seeing overall a slight pause, a slight cooling in overall evaluations on the security side versus historical levels a year ago.

A few other key points:

Bradley’s bottom line is if you’re a private-equity firm or a venture capitalist and you see a small green circle, then you’re doing well, then it means you made a good investment. And perhaps those are the ones you want to dig into further and maybe help them catch a wave with more capital and go to market expertise.

Listen to Erik Bradley’s comments on the performance of private companies in the security space.

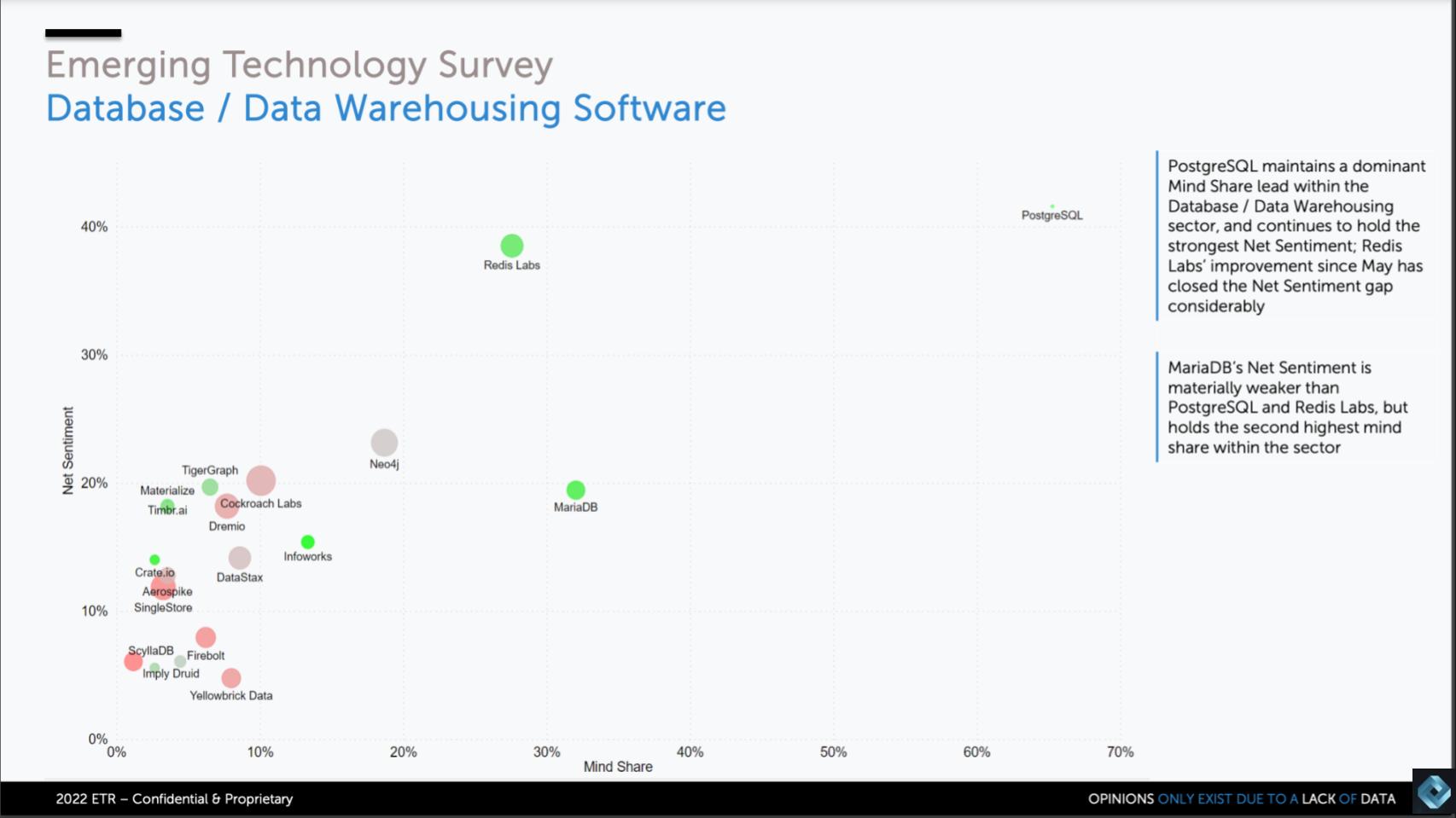

We’ll now move to the data discussion and we’ll inspect three areas within the ETS responses:

The data above shows the same dimensions and bubble indicators as the previous security view. Note that PostgresSQL shows some funding, so it’s likely that is a mix of EDB, the company, and the Postgres open-source database – a high-quality transactional system that can be thought of as an open-source version of Oracle. MariaDB is a database and a company, launched the day that Oracle acquired MySQL from the Sun Microsystems acquisition. The company has raised more than $200 million and has filed an S-4 and is doing about $50 million in revenue — basically sweeping the world of MySQL and transitioning people to MariaDB. In fact, Oracle, in response to the success of MariaDB has launched a series of enhancements to MySQL the company has named MySQL Heatwave. Heatwave has some very impressive capabilities, delivered as a fully managed proprietary database service.

Erik Bradley explains as follows:

It’s tough when you start dealing with the open-source side and I’ll be honest with you, there is a little bit of a mashup here. There are certain names that are 100% for-profit companies. And then there are others that are obviously open-source-based, like Redis is open source, but Redis Labs is the one trying to monetize the support around it. So you’re 100% accurate on this slide. I think one of the things here that’s important to note, though, is just how important open source is to data. If you’re going to be going to any of these areas, it’s going to be open-source-based to begin with. And Neo4j is one I want to call out here. It’s not one everyone’s familiar with, but it’s basically a geographical charting database. It’s a name that we’re seeing on a Net Sentiment side actually really, really high. When you think about it, it’s the third overall Net Sentiment for a niche database play. It’s not as big on the mindshare because its use cases aren’t as [prominent], but third-biggest play on Net Sentiment, which I found really interesting on this slide.

The red dots highlight companies that are performing below average relative to peers in the ETR ETS data set. Aerospike Inc. has been around for a long time. SingleStore Inc. changed its name from memSQL in 2020. Yellowbrick Data is an MPP analytic database, Firebolt Analytics Inc. is another analytic database that was making noise and throwing darts at Snowflake awhile back.

If you’re not performing well in this picture, you want to get out of that red zone and the firms highlighted there have some work to do.

Listen to Erik Bradley’s commentary on the database/data warehouse segment.

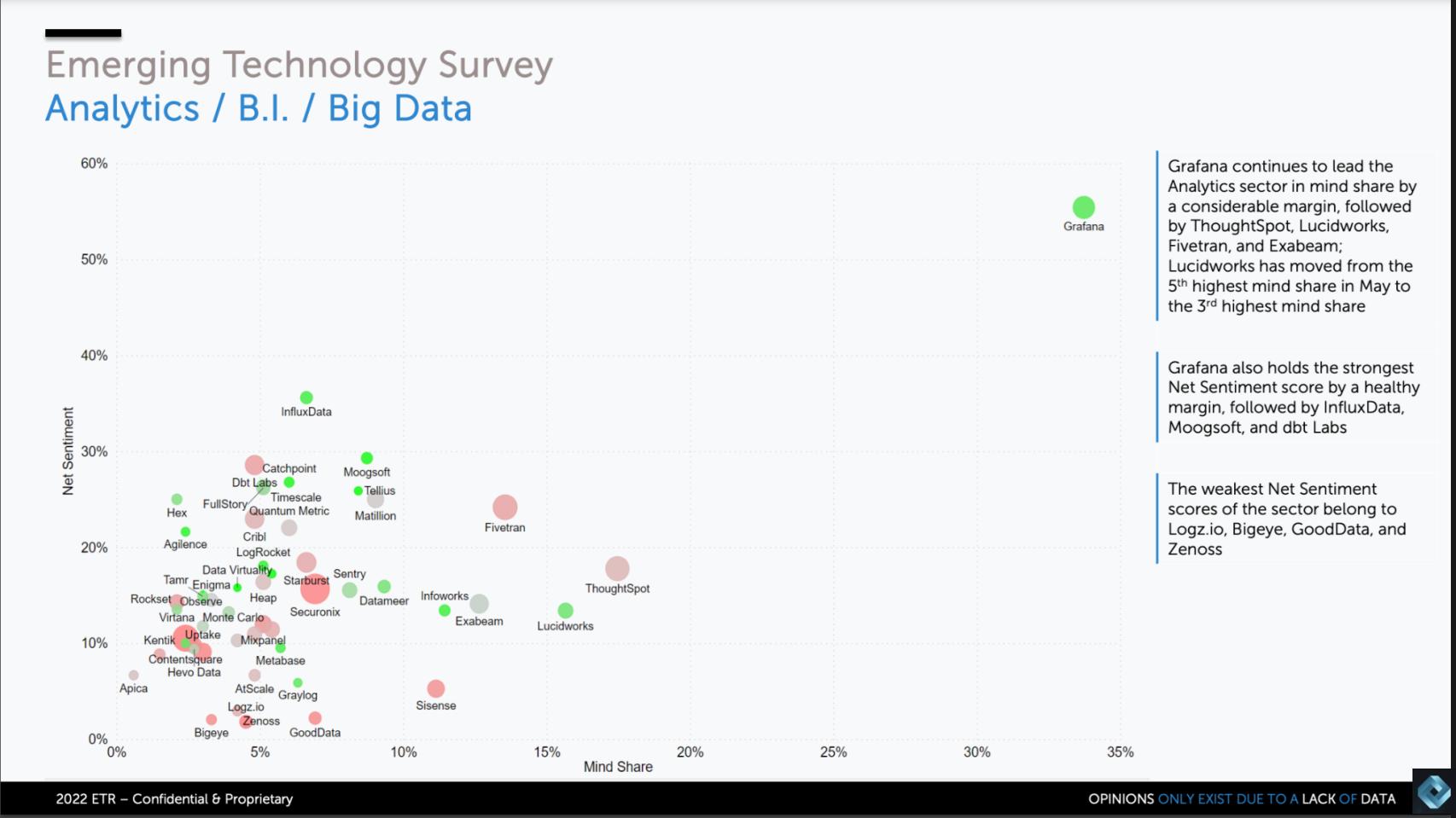

Again, same dimensions and bubble size indicators.

Some key points made by Bradley:

The small green circles are the ones that have upside potential in our view. A couple of observability companies are notable. Observe Inc. – Jeremy Burton’s company – does observability on top of Snowflake, not green, but kind of in that gray. Monte Carlo Inc. is another one, it’s slightly green. It’s doing some really interesting things in data and observability.

Listen to Erik Bradley comment on the performance of private companies in the analytics & BI space.

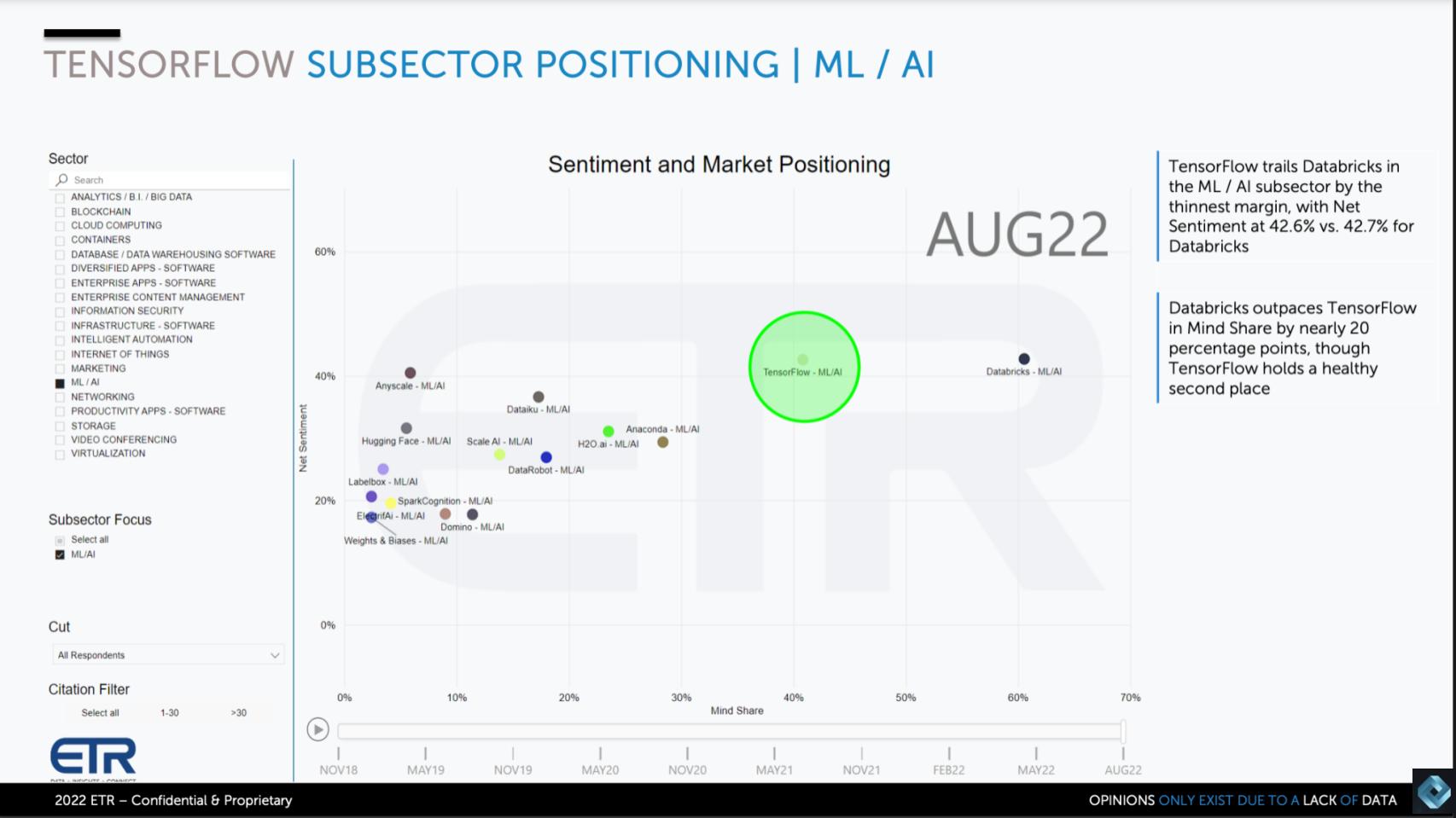

The last sector we’ll show is machine learning and AI. The chart below is similar in its dimensions except for the money raised – we’re not showing that in the size of bubble, but AI is so important we want to cover that here.

Erik Bradley explains the data and the TensorFlow callout as follows:

It’s funny again, right? Another open-source name, TensorFlow being up there. And I just want to explain, we do break out machine learning, AI is its own sector. A lot of this of course really is intertwined with the data side, but it is on its own area. And one of the things I think that’s most important here to break out is Databricks. We started to cover Databricks in machine learning, AI. That company has grown into much, much more than that. So I do want to state to you, Dave, and also the audience out there that moving forward, we’re going to be moving Databricks out of only the MA/AI into other sectors. So we can kind of value them against their peers a little bit better. But in this instance, you could just see how dominant they are in this area. And one thing that’s not here, but I do want to point out, is that we have the ability to break this down by industry vertical and organization size.

And when I break this down into Fortune 500 and Fortune 1000, both Databricks and Tensorflow are even better than you see here. So it’s quite interesting to see that the names that are succeeding are also succeeding with the largest organizations in the world. And as we know, large organizations means large budgets. So this is one area that I just thought was really interesting to point out that as we break it down, the data by vertical, these two names still are the outstanding players.

Some other callouts on this data slide:

Listen to Erik Bradley comment on the ML/AI performance of private companies.

You might expect that during a tightening cycle as we’re seeing today, that organizations would be more risk averse and reduce bets on emerging tech companies. That doesn’t seem to be the case across the board today but it is happening in pockets.

We asked Erik Bradley to give us a time series perspective on this topic:

Before we went live, you and I were having this conversation about “Is the downturn stopping people from evaluating these private companies or not,” right? In a larger sense, that’s really what we’re doing here. How are these private companies doing when it comes down to the actual practitioners? The people with the budget, the people with the decision making. And so what I did is, we have historical data as you know, I went back to the Emerging Technology Survey we did in November of 2021, right at the crest right before the market started to really fall and everything kind of started to fall apart there. And what I noticed is on the security side, very much so, we’re seeing less evaluations than we were in November ’21. So I broke it down.

- On cloud security, Net Sentiment went from 21% to 16% from November ’21. That’s a pretty big drop. That sentiment is our one aggregate metric for overall positivity, meaning utilization and actual evaluation of the name.

- In database, we saw it drop a little bit from 19% to 13%.

- In analytics we actually saw it stay steady.

So it’s pretty interesting that yes, cloud security and security in general is always going to be important. But right now we’re seeing less overall net sentiment in that space. But within analytics, we’re seeing steady with growing mindshare. And also to your point earlier in machine learning, AI, we’re seeing steady net sentiment and mindshare has grown a whopping 25% to 30%. So despite the downturn, we’re seeing more awareness of these companies in analytics and machine learning and a steady, actual utilization of them. I can’t say the same in security and database. They’re actually shrinking a little bit since the end of last year.

The ETR Emerging Technology Survey gives us insight to those companies that, like savvy politicians, accentuate the good and deflect the bad. Many companies in the ETS survey have raised historically large amounts of capital at attractive valuation terms. This is a two-edged sword in that on the one hand, many have lots of runway, but on the other hand, they have investors that expect a solid return. So while they may be able to gain share and grow, they may not be able to get back to the valuations from their late round raises. This may negatively impact their ability to wait it out for an IPO and stay independent over a long period of time.

While companies will often claim they’re not eager to go public or that they have plenty of cash and runway, a robust IPO market is almost always the best option for investors and, despite the compliance and governance edicts and the 30-day shot clock, it confers awareness and credibility advantages to those firms that can make it to IPO.

Assuming they can execute.

Thanks to Erik Bradley for bringing us the ETS data and helping us unpack the trends of private firms. Alex Myerson and Ken Shiffman are on production, podcasts and media workflows for Breaking Analysis. Special thanks to Kristen Martin and Cheryl Knight, who help us keep our community informed and get the word out, and to Rob Hof, our editor in chief at SiliconANGLE.

Remember we publish each week on Wikibon and SiliconANGLE. These episodes are all available as podcasts wherever you listen.

Email david.vellante@siliconangle.com, DM @dvellante on Twitter and comment on our LinkedIn posts.

Also, check out this ETR Tutorial we created, which explains the spending methodology in more detail. Note: ETR is a separate company from Wikibon and SiliconANGLE. If you would like to cite or republish any of the company’s data, or inquire about its services, please contact ETR at legal@etr.ai.

Watch the full video analysis:

All statements made regarding companies or securities are strictly beliefs, points of view and opinions held by SiliconANGLE Media, Enterprise Technology Research, other guests on theCUBE and guest writers. Such statements are not recommendations by these individuals to buy, sell or hold any security. The content presented does not constitute investment advice and should not be used as the basis for any investment decision. You and only you are responsible for your investment decisions.

Disclosure: Many of the companies cited in Breaking Analysis are sponsors of theCUBE and/or clients of Wikibon. None of these firms or other companies have any editorial control over or advanced viewing of what’s published in Breaking Analysis.

Support our mission to keep content open and free by engaging with theCUBE community. Join theCUBE’s Alumni Trust Network, where technology leaders connect, share intelligence and create opportunities.

Founded by tech visionaries John Furrier and Dave Vellante, SiliconANGLE Media has built a dynamic ecosystem of industry-leading digital media brands that reach 15+ million elite tech professionals. Our new proprietary theCUBE AI Video Cloud is breaking ground in audience interaction, leveraging theCUBEai.com neural network to help technology companies make data-driven decisions and stay at the forefront of industry conversations.